{"title":"Stock exchange trading optimization algorithm: a human-inspired method for global optimization.","authors":"Hojjat Emami","doi":"10.1007/s11227-021-03943-w","DOIUrl":null,"url":null,"abstract":"<p><p>In this paper, a human-inspired optimization algorithm called stock exchange trading optimization (SETO) for solving numerical and engineering problems is introduced. The inspiration source of this optimizer is the behavior of traders and stock price changes in the stock market. Traders use various fundamental and technical analysis methods to gain maximum profit. SETO mathematically models the technical trading strategy of traders to perform optimization. It contains three main actuators including rising, falling, and exchange. These operators navigate the search agents toward the global optimum. The proposed algorithm is compared with seven popular meta-heuristic optimizers on forty single-objective unconstraint numerical functions and four engineering design problems. The statistical results obtained on test problems show that SETO is capable of providing competitive and promising performances compared with counterpart algorithms in solving optimization problems of different dimensions, especially 1000-dimension problems. Out of 40 numerical functions, the SETO algorithm has achieved the global optimum on 36 functions, and out of 4 engineering problems, it has obtained the best results on 3 problems.</p>","PeriodicalId":50034,"journal":{"name":"Journal of Supercomputing","volume":"78 2","pages":"2125-2174"},"PeriodicalIF":2.7000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1007/s11227-021-03943-w","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Supercomputing","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1007/s11227-021-03943-w","RegionNum":3,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"COMPUTER SCIENCE, HARDWARE & ARCHITECTURE","Score":null,"Total":0}

引用次数: 1

Abstract

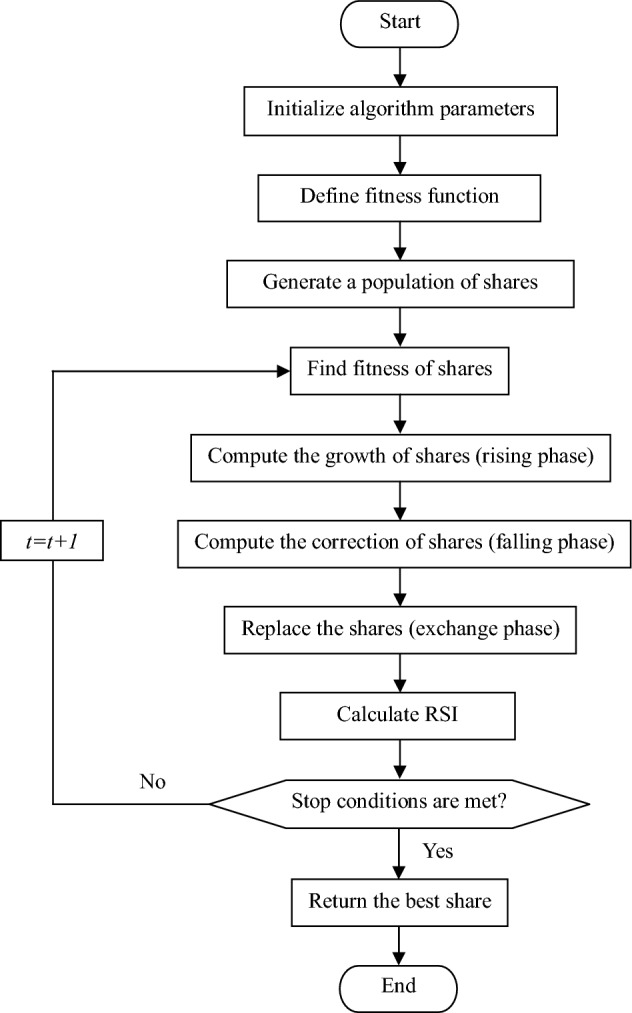

In this paper, a human-inspired optimization algorithm called stock exchange trading optimization (SETO) for solving numerical and engineering problems is introduced. The inspiration source of this optimizer is the behavior of traders and stock price changes in the stock market. Traders use various fundamental and technical analysis methods to gain maximum profit. SETO mathematically models the technical trading strategy of traders to perform optimization. It contains three main actuators including rising, falling, and exchange. These operators navigate the search agents toward the global optimum. The proposed algorithm is compared with seven popular meta-heuristic optimizers on forty single-objective unconstraint numerical functions and four engineering design problems. The statistical results obtained on test problems show that SETO is capable of providing competitive and promising performances compared with counterpart algorithms in solving optimization problems of different dimensions, especially 1000-dimension problems. Out of 40 numerical functions, the SETO algorithm has achieved the global optimum on 36 functions, and out of 4 engineering problems, it has obtained the best results on 3 problems.

期刊介绍:

The Journal of Supercomputing publishes papers on the technology, architecture and systems, algorithms, languages and programs, performance measures and methods, and applications of all aspects of Supercomputing. Tutorial and survey papers are intended for workers and students in the fields associated with and employing advanced computer systems. The journal also publishes letters to the editor, especially in areas relating to policy, succinct statements of paradoxes, intuitively puzzling results, partial results and real needs.

Published theoretical and practical papers are advanced, in-depth treatments describing new developments and new ideas. Each includes an introduction summarizing prior, directly pertinent work that is useful for the reader to understand, in order to appreciate the advances being described.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们