{"title":"Systemic cascades on inhomogeneous random financial networks.","authors":"T R Hurd","doi":"10.1007/s11579-022-00315-7","DOIUrl":null,"url":null,"abstract":"<p><p>This article presents a model of the financial system as an inhomogeneous random financial network (IRFN) with <i>N</i> nodes that represent different types of institutions such as banks or funds and directed weighted edges that signify counterparty relationships between nodes. The onset of a systemic crisis is triggered by a large exogenous shock to banks' balance sheets. Their behavioural response is modelled by a cascade mechanism that tracks the propagation of damaging shocks and possible amplification of the crisis, and leads the system to a cascade equilibrium. The mathematical properties of the stochastic framework are investigated for the first time in a generalization of the Eisenberg-Noe solvency cascade mechanism that accounts for fractional bankruptcy charges. New results include verification of a \"tree independent cascade property\" of the solvency cascade mechanism, and culminate in an explicit recursive stochastic solvency cascade mapping conjectured to hold in the limit as the number of banks <i>N</i> goes to infinity. It is shown how this cascade mapping can be computed numerically, leading to a rich picture of the systemic crisis as it evolves toward the cascade equilibrium.</p>","PeriodicalId":48722,"journal":{"name":"Mathematics and Financial Economics","volume":"17 1","pages":"1-21"},"PeriodicalIF":1.0000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9944675/pdf/","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematics and Financial Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11579-022-00315-7","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 1

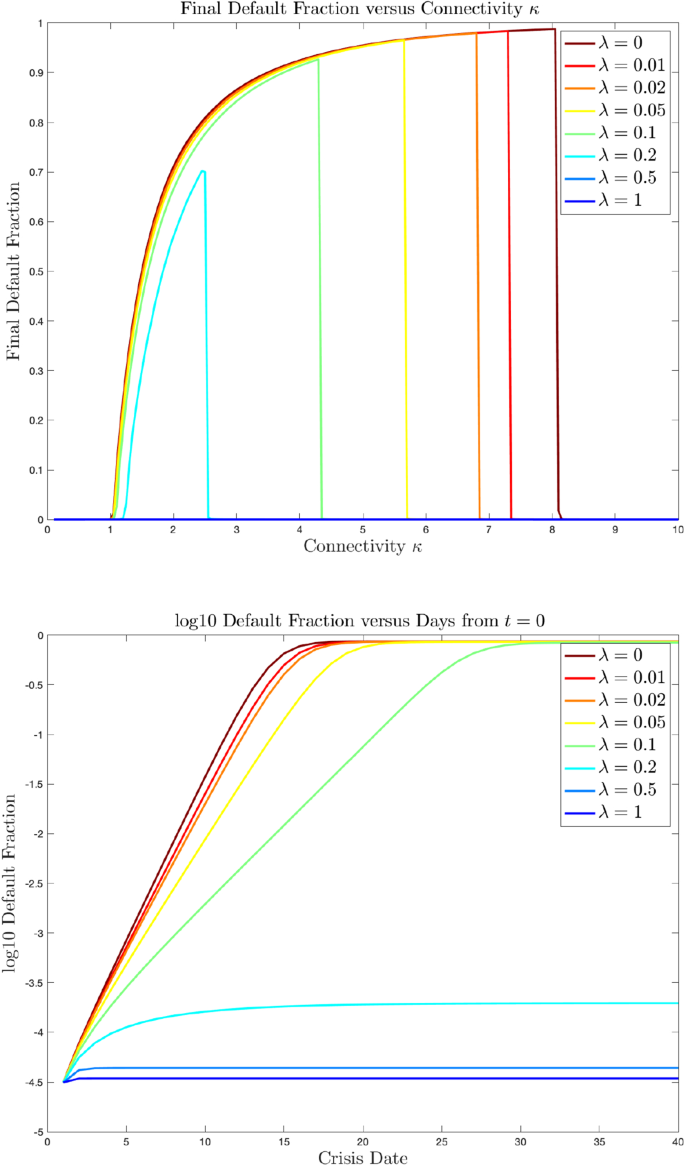

Abstract

This article presents a model of the financial system as an inhomogeneous random financial network (IRFN) with N nodes that represent different types of institutions such as banks or funds and directed weighted edges that signify counterparty relationships between nodes. The onset of a systemic crisis is triggered by a large exogenous shock to banks' balance sheets. Their behavioural response is modelled by a cascade mechanism that tracks the propagation of damaging shocks and possible amplification of the crisis, and leads the system to a cascade equilibrium. The mathematical properties of the stochastic framework are investigated for the first time in a generalization of the Eisenberg-Noe solvency cascade mechanism that accounts for fractional bankruptcy charges. New results include verification of a "tree independent cascade property" of the solvency cascade mechanism, and culminate in an explicit recursive stochastic solvency cascade mapping conjectured to hold in the limit as the number of banks N goes to infinity. It is shown how this cascade mapping can be computed numerically, leading to a rich picture of the systemic crisis as it evolves toward the cascade equilibrium.

期刊介绍:

The primary objective of the journal is to provide a forum for work in finance which expresses economic ideas using formal mathematical reasoning. The work should have real economic content and the mathematical reasoning should be new and correct.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们