{"title":"Extracting information from the limit order book: New measures to evaluate equity data flow","authors":"Ziwen Ye, Ionuţ Florescu","doi":"10.1002/hf2.10029","DOIUrl":null,"url":null,"abstract":"<p>In this research, we develop a set of new measures to evaluate the data flow in the U.S. equity exchanges using Level I order book data. The quantities we develop and use to summarize trading activity are as follows: the activity-weighted spread and the activity-weighted return. We study the distribution of these two quantities and observe that there are significant changes in their behavior when equity markets are impacted by an external event. We focus the study on three exchanges: New York Stock Exchange (NYS), NASDAQ InterMarket (THM), and NYSE Arca (PSE) since they exhibit the largest impact to the proposed measures. We also study two different financial events which happened suddenly without any prior warning. These events are as follows: May 6, 2010, the “Flash Crash,” and April 23, 2013, the “Hoax tweet” event. Based on the results we obtain, the order flow dynamic is disturbed during these rare events. We quantify this change by measuring the number of detected “anomalies” for each exchange and equity studied. We believe the methodology we propose may be capable of detecting a potential unforecasted event as it is impacting the equity markets.</p>","PeriodicalId":100604,"journal":{"name":"High Frequency","volume":"2 1","pages":"37-47"},"PeriodicalIF":0.0000,"publicationDate":"2019-03-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/hf2.10029","citationCount":"5","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"High Frequency","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10029","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 5

Abstract

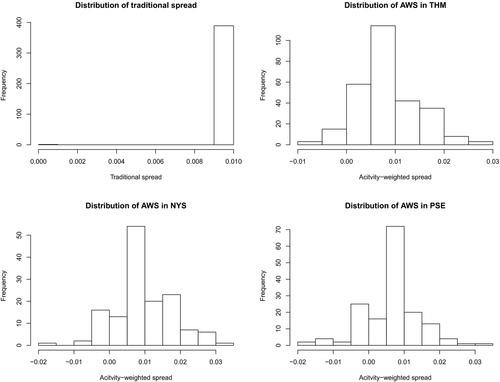

In this research, we develop a set of new measures to evaluate the data flow in the U.S. equity exchanges using Level I order book data. The quantities we develop and use to summarize trading activity are as follows: the activity-weighted spread and the activity-weighted return. We study the distribution of these two quantities and observe that there are significant changes in their behavior when equity markets are impacted by an external event. We focus the study on three exchanges: New York Stock Exchange (NYS), NASDAQ InterMarket (THM), and NYSE Arca (PSE) since they exhibit the largest impact to the proposed measures. We also study two different financial events which happened suddenly without any prior warning. These events are as follows: May 6, 2010, the “Flash Crash,” and April 23, 2013, the “Hoax tweet” event. Based on the results we obtain, the order flow dynamic is disturbed during these rare events. We quantify this change by measuring the number of detected “anomalies” for each exchange and equity studied. We believe the methodology we propose may be capable of detecting a potential unforecasted event as it is impacting the equity markets.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们