Rei Taguchi, Hiroki Sakaji, Kiyoshi Izumi, Yuri Murayama

{"title":"Constructing Sentiment Signal-Based Asset Allocation Method with Causality Information","authors":"Rei Taguchi, Hiroki Sakaji, Kiyoshi Izumi, Yuri Murayama","doi":"10.1007/s00354-023-00231-4","DOIUrl":null,"url":null,"abstract":"Abstract This study demonstrates whether financial text is useful for the tactical asset allocation method using stocks. This can be achieved using natural language processing to create polarity indexes in financial news. We perform clustering of the created polarity indexes using the change point detection algorithm. In addition, we construct a stock portfolio and rebalanced it at each change point using an optimization algorithm. Consequently, the proposed asset allocation method outperforms the comparative approach. This result suggests that the polarity index is useful for constructing the equity asset allocation method.","PeriodicalId":54726,"journal":{"name":"New Generation Computing","volume":"31 1","pages":"0"},"PeriodicalIF":2.0000,"publicationDate":"2023-09-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"New Generation Computing","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s00354-023-00231-4","RegionNum":4,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"COMPUTER SCIENCE, HARDWARE & ARCHITECTURE","Score":null,"Total":0}

引用次数: 0

Abstract

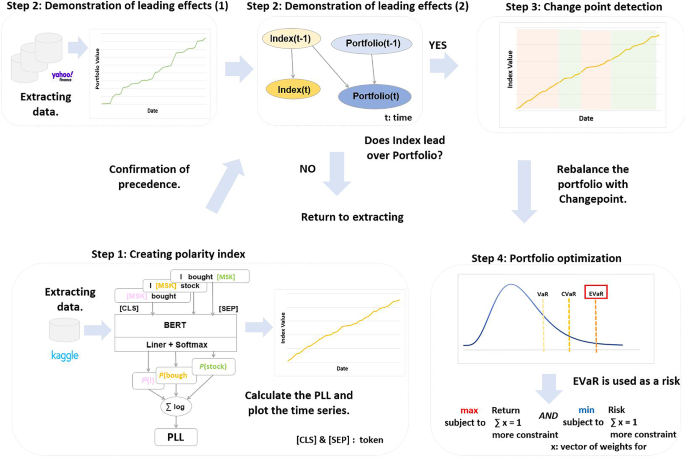

Abstract This study demonstrates whether financial text is useful for the tactical asset allocation method using stocks. This can be achieved using natural language processing to create polarity indexes in financial news. We perform clustering of the created polarity indexes using the change point detection algorithm. In addition, we construct a stock portfolio and rebalanced it at each change point using an optimization algorithm. Consequently, the proposed asset allocation method outperforms the comparative approach. This result suggests that the polarity index is useful for constructing the equity asset allocation method.

期刊介绍:

The journal is specially intended to support the development of new computational and cognitive paradigms stemming from the cross-fertilization of various research fields. These fields include, but are not limited to, programming (logic, constraint, functional, object-oriented), distributed/parallel computing, knowledge-based systems, agent-oriented systems, and cognitive aspects of human embodied knowledge. It also encourages theoretical and/or practical papers concerning all types of learning, knowledge discovery, evolutionary mechanisms, human cognition and learning, and emergent systems that can lead to key technologies enabling us to build more complex and intelligent systems. The editorial board hopes that New Generation Computing will work as a catalyst among active researchers with broad interests by ensuring a smooth publication process.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们