{"title":"Optimal execution with stochastic delay","authors":"Álvaro Cartea, Leandro Sánchez-Betancourt","doi":"10.1007/s00780-022-00491-w","DOIUrl":null,"url":null,"abstract":"<p>We show how traders use marketable limit orders (MLOs) to liquidate a position over a trading window when there is latency in the marketplace. MLOs are liquidity-taking orders that specify a price limit and are for immediate execution only; however, if the price limit of the MLO precludes it from being filled, the exchange cancels the order. We frame our model as an impulse control problem with stochastic latency where the trader controls the times and the price limits of the MLOs sent to the exchange. We show that impatient liquidity takers submit MLOs that may walk the book (capped by the limit price) to increase the probability of filling the trades. On the other hand, patient liquidity takers use speculative MLOs that are only filled if there has been an advantageous move in prices over the latency period. Patient traders who are fast do not use their speed to hit the quotes they observe, or to finish the execution programme early; they use speed to complete the execution programme with as many speculative MLOs as possible. We use foreign exchange data to implement the random-latency-optimal strategy and to compare it with four benchmarks. For patient traders, the random-latency-optimal strategy outperforms the benchmarks by an amount that is greater than the transaction costs paid by liquidity takers in foreign exchange markets. Around news announcements, the value of the outperformance is between two and ten times the value of the transaction costs. The superiority of the strategy is due to both the speculative MLOs that are filled and the price protection of the MLOs.</p>","PeriodicalId":50447,"journal":{"name":"Finance and Stochastics","volume":"90 3","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2022-12-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Finance and Stochastics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00780-022-00491-w","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

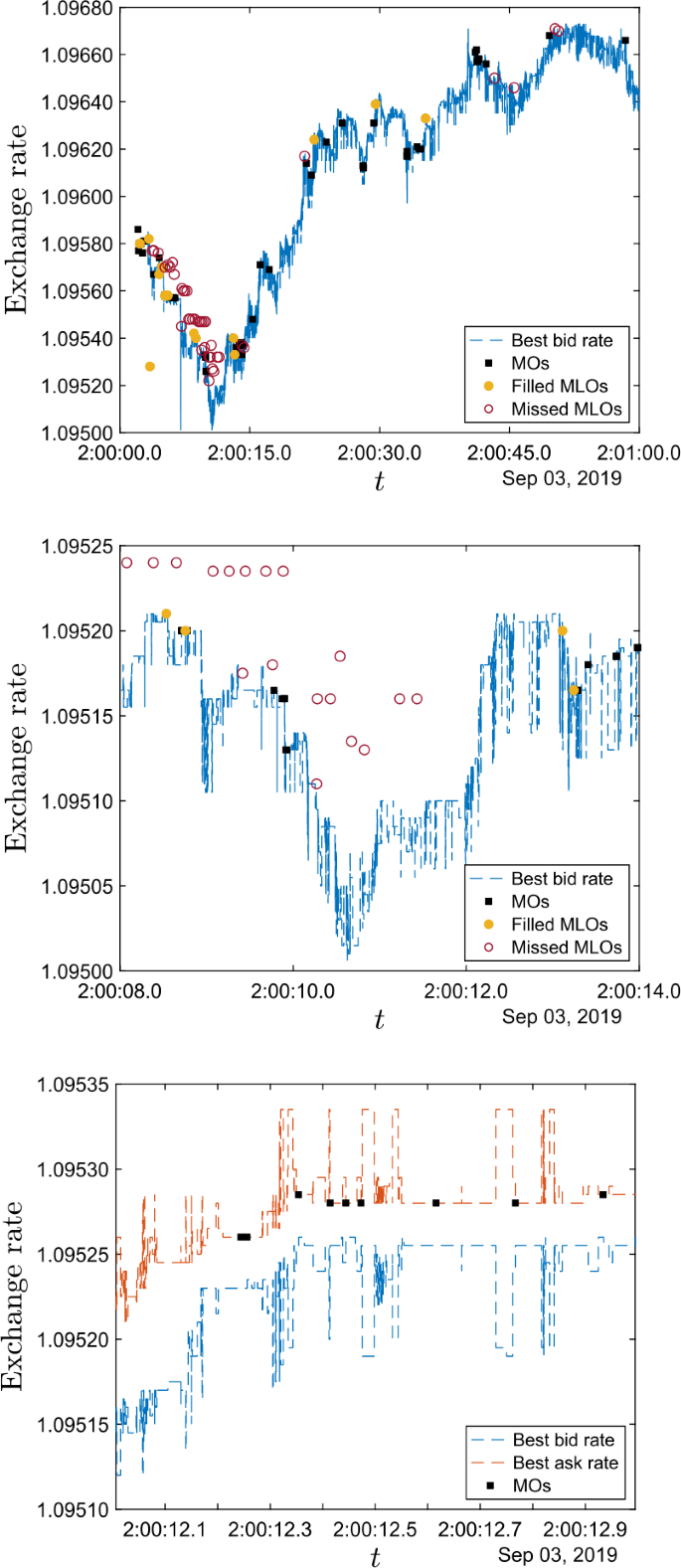

We show how traders use marketable limit orders (MLOs) to liquidate a position over a trading window when there is latency in the marketplace. MLOs are liquidity-taking orders that specify a price limit and are for immediate execution only; however, if the price limit of the MLO precludes it from being filled, the exchange cancels the order. We frame our model as an impulse control problem with stochastic latency where the trader controls the times and the price limits of the MLOs sent to the exchange. We show that impatient liquidity takers submit MLOs that may walk the book (capped by the limit price) to increase the probability of filling the trades. On the other hand, patient liquidity takers use speculative MLOs that are only filled if there has been an advantageous move in prices over the latency period. Patient traders who are fast do not use their speed to hit the quotes they observe, or to finish the execution programme early; they use speed to complete the execution programme with as many speculative MLOs as possible. We use foreign exchange data to implement the random-latency-optimal strategy and to compare it with four benchmarks. For patient traders, the random-latency-optimal strategy outperforms the benchmarks by an amount that is greater than the transaction costs paid by liquidity takers in foreign exchange markets. Around news announcements, the value of the outperformance is between two and ten times the value of the transaction costs. The superiority of the strategy is due to both the speculative MLOs that are filled and the price protection of the MLOs.

期刊介绍:

The purpose of Finance and Stochastics is to provide a high standard publication forum for research

- in all areas of finance based on stochastic methods

- on specific topics in mathematics (in particular probability theory, statistics and stochastic analysis) motivated by the analysis of problems in finance.

Finance and Stochastics encompasses - but is not limited to - the following fields:

- theory and analysis of financial markets

- continuous time finance

- derivatives research

- insurance in relation to finance

- portfolio selection

- credit and market risks

- term structure models

- statistical and empirical financial studies based on advanced stochastic methods

- numerical and stochastic solution techniques for problems in finance

- intertemporal economics, uncertainty and information in relation to finance.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们