{"title":"Using interest rates to predict economic growth: Are corporate bonds better?","authors":"David G. McMillan","doi":"10.1002/ijfe.2867","DOIUrl":null,"url":null,"abstract":"<p>We consider whether government bonds, through the term structure, or corporate bonds, through the default yield, provide predictive power for output, consumption and investment growth in the United States. Such predictive power will allow policy-makers to use the information as a leading indicator for macroeconomic performance and will improve our understanding of the links between real and financial markets. Full sample results suggest that both interest rate series exhibit predictive power for each of the macroeconomic growth series. Time-variation in the predictive coefficient reveals the waning influence of the term structure and the rising influence of the default yield. Forecast results, which are obtained from a rolling window approach, likewise suggest both series have information content for macroeconomic conditions, but there is a change in their relative strengths. These results may arise as interest rates have declined since the highs of the early to mid-1980s thus reducing the information content of government yields, whereas corporate bonds respond more to investor views of macroeconomic risk, which affects a firm's ability to repay its debt. Furthermore, short-term rates are largely held unprecedently low since the dotcom crash.</p>","PeriodicalId":47461,"journal":{"name":"International Journal of Finance & Economics","volume":"29 4","pages":"3995-4009"},"PeriodicalIF":2.8000,"publicationDate":"2023-07-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ijfe.2867","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Finance & Economics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/ijfe.2867","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

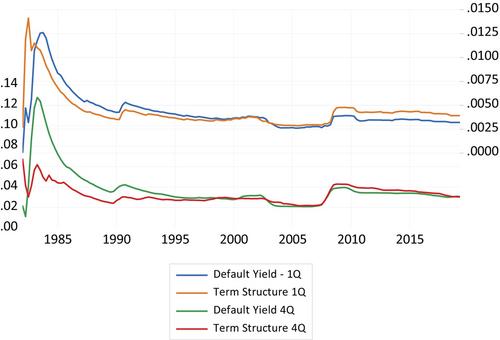

Abstract

We consider whether government bonds, through the term structure, or corporate bonds, through the default yield, provide predictive power for output, consumption and investment growth in the United States. Such predictive power will allow policy-makers to use the information as a leading indicator for macroeconomic performance and will improve our understanding of the links between real and financial markets. Full sample results suggest that both interest rate series exhibit predictive power for each of the macroeconomic growth series. Time-variation in the predictive coefficient reveals the waning influence of the term structure and the rising influence of the default yield. Forecast results, which are obtained from a rolling window approach, likewise suggest both series have information content for macroeconomic conditions, but there is a change in their relative strengths. These results may arise as interest rates have declined since the highs of the early to mid-1980s thus reducing the information content of government yields, whereas corporate bonds respond more to investor views of macroeconomic risk, which affects a firm's ability to repay its debt. Furthermore, short-term rates are largely held unprecedently low since the dotcom crash.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们