{"title":"Does corporate governance spur bank intellectual capital in an emerging economy? A system GMM analysis from Ethiopia","authors":"Abdu Mohammed Assfaw, Dhiraj Sharma","doi":"10.1186/s43093-023-00298-x","DOIUrl":null,"url":null,"abstract":"<h3 data-test=\"abstract-sub-heading\">Purpose</h3><p>The current study aims to explore the impact of corporate governance (CG) mechanisms, as measured by board size, board meeting frequency, board gender diversity, number of board subcommittees, board remuneration, size of audit committee, and audit committee meeting frequency, on bank intellectual capital (as calculated by the modified value-added intellectual coefficient (M-VAIC) and its components (human capital efficiency (HCE), structural capital efficiency (SCE), and relational capital efficiency (SCE)).</p><h3 data-test=\"abstract-sub-heading\">Design/methodology/approach</h3><p>Panel data is extracted from the financial and other internal reports of 14 commercial banks and the National Bank of Ethiopia for the period 2011–2022. A two-step system generalized method of moments (2SYS-GMM) was used to account for the unobserved endogeneity and heteroscedasticity problems.</p><h3 data-test=\"abstract-sub-heading\">Findings</h3><p>The empirical findings suggest that board size and board meeting frequency have a negative and significant impact on all IC performance measures. Besides, audit committee size has a negative and significant effect on HCE, SCE, and M-VAIC of the banking industry in Ethiopia. Moreover, board remuneration has a significant positive relationship with IC efficiency (HCE, SCE, and M-VAIC). Also, audit committee meeting frequency has a positive and significant effect on the HCE of banks. However, board gender diversity and the number of board subcommittees have not made statistically significant contributions to IC performance.</p><h3 data-test=\"abstract-sub-heading\">Research limitation/implication</h3><p>The study is limited in its use of seven dimensions of CG and future studies can use other alternative accounts for CG variables. Next, this study applies only to commercial banks; hence, future studies can include other financial as well as non-financial organizations such as insurance companies, microfinance institutions, manufacturing, and other sectors.</p><h3 data-test=\"abstract-sub-heading\">Practical implications</h3><p>This study contributes to helping the regulators and practitioners of the banking industry improve the existing standards and guidelines for CG practices to strengthen their IC performance. The findings may also give input for policymakers to integrate the intellectual capital in the decision-making process for policy formulation and implementation for the establishment of a robust banking sector.</p><h3 data-test=\"abstract-sub-heading\">Originality/value</h3><p>Considering the modified value-added IC coefficient (M-VAIC) and 2SYS-GMM models, this research is the first study to analyze the relationships between CG and banks’ IC in Ethiopia.</p>","PeriodicalId":44859,"journal":{"name":"Future Business Journal","volume":"1 1","pages":""},"PeriodicalIF":2.7000,"publicationDate":"2024-01-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Future Business Journal","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1186/s43093-023-00298-x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

Abstract

Purpose

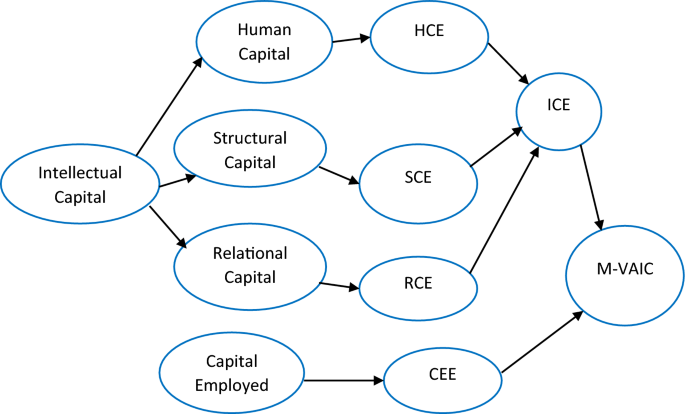

The current study aims to explore the impact of corporate governance (CG) mechanisms, as measured by board size, board meeting frequency, board gender diversity, number of board subcommittees, board remuneration, size of audit committee, and audit committee meeting frequency, on bank intellectual capital (as calculated by the modified value-added intellectual coefficient (M-VAIC) and its components (human capital efficiency (HCE), structural capital efficiency (SCE), and relational capital efficiency (SCE)).

Design/methodology/approach

Panel data is extracted from the financial and other internal reports of 14 commercial banks and the National Bank of Ethiopia for the period 2011–2022. A two-step system generalized method of moments (2SYS-GMM) was used to account for the unobserved endogeneity and heteroscedasticity problems.

Findings

The empirical findings suggest that board size and board meeting frequency have a negative and significant impact on all IC performance measures. Besides, audit committee size has a negative and significant effect on HCE, SCE, and M-VAIC of the banking industry in Ethiopia. Moreover, board remuneration has a significant positive relationship with IC efficiency (HCE, SCE, and M-VAIC). Also, audit committee meeting frequency has a positive and significant effect on the HCE of banks. However, board gender diversity and the number of board subcommittees have not made statistically significant contributions to IC performance.

Research limitation/implication

The study is limited in its use of seven dimensions of CG and future studies can use other alternative accounts for CG variables. Next, this study applies only to commercial banks; hence, future studies can include other financial as well as non-financial organizations such as insurance companies, microfinance institutions, manufacturing, and other sectors.

Practical implications

This study contributes to helping the regulators and practitioners of the banking industry improve the existing standards and guidelines for CG practices to strengthen their IC performance. The findings may also give input for policymakers to integrate the intellectual capital in the decision-making process for policy formulation and implementation for the establishment of a robust banking sector.

Originality/value

Considering the modified value-added IC coefficient (M-VAIC) and 2SYS-GMM models, this research is the first study to analyze the relationships between CG and banks’ IC in Ethiopia.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们