{"title":"Identifying the systemic importance and systemic vulnerability of financial institutions based on portfolio similarity correlation network","authors":"Manjin Shao, Hong Fan","doi":"10.1140/epjds/s13688-024-00449-2","DOIUrl":null,"url":null,"abstract":"<p>The indirect correlation among financial institutions, stemming from similarities in their portfolios, is a primary driver of systemic risk. However, most existing research overlooks the influence of portfolio similarity among various types of financial institutions on this risk. Therefore, we construct the network of portfolio similarity correlations among different types of financial institutions, based on measurements of portfolio similarity. Utilizing the expanded fire sale contagion model, we offer a comprehensive assessment of systemic risk for Chinese financial institutions. Initially, we introduce indicators for systemic risk, systemic importance, and systemic vulnerability. Subsequently, we examine the cross-sectional and time-series characteristics of these institutions’ systemic importance and vulnerability within the context of the portfolio similarity correlation network. Our empirical findings reveal a high degree of portfolio similarity between banks and insurance companies, contrasted with lower similarity between banks and securities firms. Moreover, when considering the portfolio similarity correlation network, both the systemic importance and vulnerability of Chinese banks and insurance companies surpass those of securities firms in both cross-sectional and temporal dimensions. Notably, our analysis further illustrates that a financial institution’s systemic importance and vulnerability are strongly and positively associated with the magnitude of portfolio similarity between that institution and others.</p>","PeriodicalId":11887,"journal":{"name":"EPJ Data Science","volume":"2 1","pages":""},"PeriodicalIF":2.5000,"publicationDate":"2024-01-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"EPJ Data Science","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1140/epjds/s13688-024-00449-2","RegionNum":2,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

引用次数: 0

Abstract

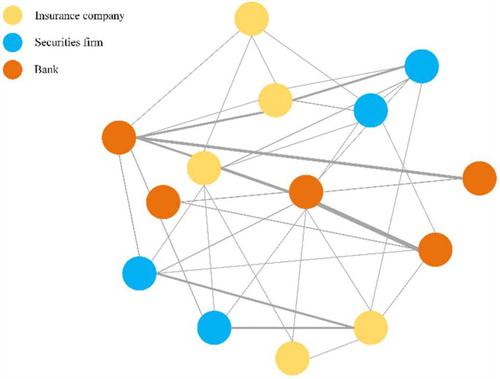

The indirect correlation among financial institutions, stemming from similarities in their portfolios, is a primary driver of systemic risk. However, most existing research overlooks the influence of portfolio similarity among various types of financial institutions on this risk. Therefore, we construct the network of portfolio similarity correlations among different types of financial institutions, based on measurements of portfolio similarity. Utilizing the expanded fire sale contagion model, we offer a comprehensive assessment of systemic risk for Chinese financial institutions. Initially, we introduce indicators for systemic risk, systemic importance, and systemic vulnerability. Subsequently, we examine the cross-sectional and time-series characteristics of these institutions’ systemic importance and vulnerability within the context of the portfolio similarity correlation network. Our empirical findings reveal a high degree of portfolio similarity between banks and insurance companies, contrasted with lower similarity between banks and securities firms. Moreover, when considering the portfolio similarity correlation network, both the systemic importance and vulnerability of Chinese banks and insurance companies surpass those of securities firms in both cross-sectional and temporal dimensions. Notably, our analysis further illustrates that a financial institution’s systemic importance and vulnerability are strongly and positively associated with the magnitude of portfolio similarity between that institution and others.

期刊介绍:

EPJ Data Science covers a broad range of research areas and applications and particularly encourages contributions from techno-socio-economic systems, where it comprises those research lines that now regard the digital “tracks” of human beings as first-order objects for scientific investigation. Topics include, but are not limited to, human behavior, social interaction (including animal societies), economic and financial systems, management and business networks, socio-technical infrastructure, health and environmental systems, the science of science, as well as general risk and crisis scenario forecasting up to and including policy advice.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们