{"title":"The Impact of Arbitrage Between Stock Markets With and Without Maker–Taker Fees Using an Agent-Based Simulation","authors":"Xin Guan, Mahiro Hoshino, Takanobu Mizuta, Isao Yagi","doi":"10.1007/s00354-023-00239-w","DOIUrl":null,"url":null,"abstract":"<p>An increasing number of exchanges, mainly in the U.S., have adopted a commission structure called maker–taker fees in which traders placing limit orders (makers) are paid a rebate (negative trading commission) and traders placing market orders (takers) are charged a trading fee. The reason is that by paying rebates to makers, exchanges can expect to receive a large number of maker’s orders and gain market share. Makers include arbitrageurs who make large transactions. Maker–taker fees constitute one of the most important commission structures for exchanges, because they are expected to attract arbitrageurs who are looking for rebate profits, on top of their trading profits. There have been many studies about arbitrage trading, but none we could find focused on the impact of arbitrage trading between markets with maker–taker fees where arbitrage traders place limit orders and markets without maker–taker fees where they place market orders. In this study, we investigated volatility and market liquidity by changing the amount of rebate under our proposed artificial markets, where there are or are not maker–taker fees. Then we checked the performance of arbitrage trading when the rebate increased. The results were that volatility in the market with maker–taker fees decreased and that in the market without maker–taker fees increased, and that market liquidity and arbitrage performance both increased in the market with maker–taker fees when rebates increased. The above results indicate that exchanges that operate markets adopting maker–taker fees can provide investors with more attractive markets than those that do not adopt them. However, if more arbitrageurs participate in the market with maker–taker fees to take advantage of these rebates, the cost burden on exchanges may increase unnecessarily.</p>","PeriodicalId":54726,"journal":{"name":"New Generation Computing","volume":"35 1","pages":""},"PeriodicalIF":2.8000,"publicationDate":"2024-02-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"New Generation Computing","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1007/s00354-023-00239-w","RegionNum":4,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"COMPUTER SCIENCE, HARDWARE & ARCHITECTURE","Score":null,"Total":0}

引用次数: 0

Abstract

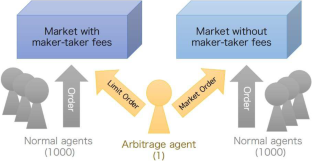

An increasing number of exchanges, mainly in the U.S., have adopted a commission structure called maker–taker fees in which traders placing limit orders (makers) are paid a rebate (negative trading commission) and traders placing market orders (takers) are charged a trading fee. The reason is that by paying rebates to makers, exchanges can expect to receive a large number of maker’s orders and gain market share. Makers include arbitrageurs who make large transactions. Maker–taker fees constitute one of the most important commission structures for exchanges, because they are expected to attract arbitrageurs who are looking for rebate profits, on top of their trading profits. There have been many studies about arbitrage trading, but none we could find focused on the impact of arbitrage trading between markets with maker–taker fees where arbitrage traders place limit orders and markets without maker–taker fees where they place market orders. In this study, we investigated volatility and market liquidity by changing the amount of rebate under our proposed artificial markets, where there are or are not maker–taker fees. Then we checked the performance of arbitrage trading when the rebate increased. The results were that volatility in the market with maker–taker fees decreased and that in the market without maker–taker fees increased, and that market liquidity and arbitrage performance both increased in the market with maker–taker fees when rebates increased. The above results indicate that exchanges that operate markets adopting maker–taker fees can provide investors with more attractive markets than those that do not adopt them. However, if more arbitrageurs participate in the market with maker–taker fees to take advantage of these rebates, the cost burden on exchanges may increase unnecessarily.

期刊介绍:

The journal is specially intended to support the development of new computational and cognitive paradigms stemming from the cross-fertilization of various research fields. These fields include, but are not limited to, programming (logic, constraint, functional, object-oriented), distributed/parallel computing, knowledge-based systems, agent-oriented systems, and cognitive aspects of human embodied knowledge. It also encourages theoretical and/or practical papers concerning all types of learning, knowledge discovery, evolutionary mechanisms, human cognition and learning, and emergent systems that can lead to key technologies enabling us to build more complex and intelligent systems. The editorial board hopes that New Generation Computing will work as a catalyst among active researchers with broad interests by ensuring a smooth publication process.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们