{"title":"Quality issues of implied volatilities of index and stock options in the OptionMetrics IvyDB database","authors":"Martin Wallmeier","doi":"10.1002/fut.22495","DOIUrl":null,"url":null,"abstract":"<p>For stock and index options in the United States, OptionMetrics records prices at 3:59 p.m., not 4:00 p.m. as assumed in previous literature. The resulting 1-min time discrepancy with closing share prices creates artificial variability in implied volatility spreads and strongly affects market-wide spreads. It leads to particularly large distortions at the onset of the COVID-19 pandemic. For index options in Europe, OptionMetrics data show large deviations from put-call parity even though the original option prices match the parity exactly. Finally, the implied volatilities of stock options in Europe show clusters of exceptional deviations due to incorrect dividend information.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 5","pages":"854-875"},"PeriodicalIF":2.3000,"publicationDate":"2024-03-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22495","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22495","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

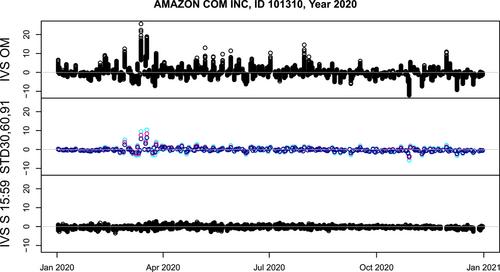

Abstract

For stock and index options in the United States, OptionMetrics records prices at 3:59 p.m., not 4:00 p.m. as assumed in previous literature. The resulting 1-min time discrepancy with closing share prices creates artificial variability in implied volatility spreads and strongly affects market-wide spreads. It leads to particularly large distortions at the onset of the COVID-19 pandemic. For index options in Europe, OptionMetrics data show large deviations from put-call parity even though the original option prices match the parity exactly. Finally, the implied volatilities of stock options in Europe show clusters of exceptional deviations due to incorrect dividend information.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们