{"title":"Predicting tail risks by a Markov switching MGARCH model with varying copula regimes","authors":"Markus J. Fülle, Helmut Herwartz","doi":"10.1002/for.3117","DOIUrl":null,"url":null,"abstract":"<p>To improve the dynamic assessment of risks of speculative assets, we apply a Markov switching MGARCH approach to portfolio risk forecasting. More specifically, we take advantage of the flexible Markov switching copula multivariate GARCH (MS-C-MGARCH) model of Fülle and Herwartz (2022). As an empirical illustration, we take the perspective of a risk-averse agent and employ the suggested model for assessments of future risks of portfolios composed of a high-yield equity index (S&P 500) and two safe-haven investment instruments (i.e., Gold and US Treasury Bond Futures). We follow recent suggestions to employ the expected shortfall as a prime assessment of tail risks. To accurately evaluate the merits of the new model, we back-test the risk forecasting for daily returns over 10 years for heterogeneous market environments including, for example, the COVID-19 pandemic. We find that the MS-C-MGARCH model outperforms benchmark volatility models (MGARCH, C-MGARCH) in predicting both value-at-risk and expected shortfall. The superiority of the MS-C-MGARCH model becomes stronger, when the share of comparably risky assets in the portfolio is relatively large.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"43 6","pages":"2163-2186"},"PeriodicalIF":2.7000,"publicationDate":"2024-03-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3117","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3117","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

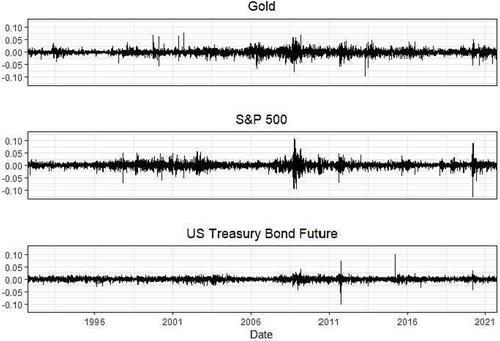

To improve the dynamic assessment of risks of speculative assets, we apply a Markov switching MGARCH approach to portfolio risk forecasting. More specifically, we take advantage of the flexible Markov switching copula multivariate GARCH (MS-C-MGARCH) model of Fülle and Herwartz (2022). As an empirical illustration, we take the perspective of a risk-averse agent and employ the suggested model for assessments of future risks of portfolios composed of a high-yield equity index (S&P 500) and two safe-haven investment instruments (i.e., Gold and US Treasury Bond Futures). We follow recent suggestions to employ the expected shortfall as a prime assessment of tail risks. To accurately evaluate the merits of the new model, we back-test the risk forecasting for daily returns over 10 years for heterogeneous market environments including, for example, the COVID-19 pandemic. We find that the MS-C-MGARCH model outperforms benchmark volatility models (MGARCH, C-MGARCH) in predicting both value-at-risk and expected shortfall. The superiority of the MS-C-MGARCH model becomes stronger, when the share of comparably risky assets in the portfolio is relatively large.

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们