{"title":"Prediction and Allocation of Stocks, Bonds, and REITs in the US Market","authors":"Ana Sofia Monteiro, Helder Sebastião, Nuno Silva","doi":"10.1007/s10614-024-10589-2","DOIUrl":null,"url":null,"abstract":"<p>This study employs dynamic model averaging and selection of Vector Autoregressive and Time-Varying Parameters Vector Autoregressive models to forecast out-of-sample monthly returns of US stocks, bonds, and Real Estate Investment Trusts (REITs) indexes from October 2006 to December 2021. The models were recursively estimated using 17 additional predictors chosen by a genetic algorithm applied to an initial list of 155 predictors. These forecasts were then used to dynamically choose portfolios formed by these assets and the riskless asset proxied by the 3-month US treasury bills. Although we did not find any predictability in the stock market, positive results were obtained for REITs and especially for bonds. The Bayesian-based approaches applied to just the returns of the three risky assets resulted in portfolios that remarkably outperform the portfolios based on the historical means and covariances and the equally weighted portfolio in terms of certainty equivalent return, Sharpe ratio, Sortino ratio and even Conditional Value-at-Risk at 5%. This study points out that Constant Relative Risk Averse investors should use Bayesian-based approaches to forecast and choose the investment portfolios, focusing their attention on different types of assets.</p>","PeriodicalId":50647,"journal":{"name":"Computational Economics","volume":"50 1","pages":""},"PeriodicalIF":2.2000,"publicationDate":"2024-04-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10614-024-10589-2","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

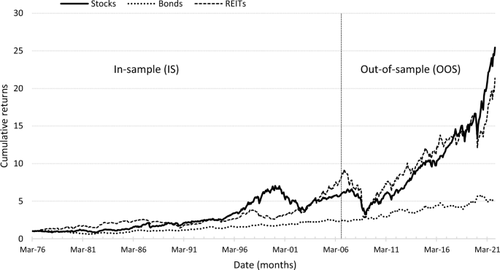

This study employs dynamic model averaging and selection of Vector Autoregressive and Time-Varying Parameters Vector Autoregressive models to forecast out-of-sample monthly returns of US stocks, bonds, and Real Estate Investment Trusts (REITs) indexes from October 2006 to December 2021. The models were recursively estimated using 17 additional predictors chosen by a genetic algorithm applied to an initial list of 155 predictors. These forecasts were then used to dynamically choose portfolios formed by these assets and the riskless asset proxied by the 3-month US treasury bills. Although we did not find any predictability in the stock market, positive results were obtained for REITs and especially for bonds. The Bayesian-based approaches applied to just the returns of the three risky assets resulted in portfolios that remarkably outperform the portfolios based on the historical means and covariances and the equally weighted portfolio in terms of certainty equivalent return, Sharpe ratio, Sortino ratio and even Conditional Value-at-Risk at 5%. This study points out that Constant Relative Risk Averse investors should use Bayesian-based approaches to forecast and choose the investment portfolios, focusing their attention on different types of assets.

期刊介绍:

Computational Economics, the official journal of the Society for Computational Economics, presents new research in a rapidly growing multidisciplinary field that uses advanced computing capabilities to understand and solve complex problems from all branches in economics. The topics of Computational Economics include computational methods in econometrics like filtering, bayesian and non-parametric approaches, markov processes and monte carlo simulation; agent based methods, machine learning, evolutionary algorithms, (neural) network modeling; computational aspects of dynamic systems, optimization, optimal control, games, equilibrium modeling; hardware and software developments, modeling languages, interfaces, symbolic processing, distributed and parallel processing

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们