Rodrigo Moreira, Larissa Ferreira Rodrigues Moreira, Flávio de Oliveira Silva

{"title":"Brazilian Selic Rate Forecasting with Deep Neural Networks","authors":"Rodrigo Moreira, Larissa Ferreira Rodrigues Moreira, Flávio de Oliveira Silva","doi":"10.1007/s10614-024-10597-2","DOIUrl":null,"url":null,"abstract":"<p>Artificial intelligence has shortened edges in many areas, especially the economy, to support long-term and accurate forecasting of financial indicators. Traditional statistical methods perform poorly compared to those based on artificial intelligence, which can achieve higher rates even with high-dimensional datasets. This method still needs evolution and studies. In emerging countries, decision-makers and investors must follow the basic interest rate, such as in Brazil, with a Special System of Settlement and Custody (Selic). Prior works used deep neural networks (DNNs) for forecasting time series economic indicators such as interest rates, inflation, and the stock market. However, there is no empirical evaluation of the prediction models for the Selic interest rate, especially the impact of training time and the optimization of hyperparameters. In this paper, we shed light on these issues and evaluate, through a fair comparison, the use of DNNs models for Selic time series forecasting. Our results demonstrate the potential of DNNs with an error rate above 0.00219 and training time above 84.28 s. Our findings open up opportunities for further investigations toward real-time interest rate forecasting, facilitating more reliable and timely forecasting of interest rates for decision-makers and investors.</p>","PeriodicalId":50647,"journal":{"name":"Computational Economics","volume":"49 1","pages":""},"PeriodicalIF":2.2000,"publicationDate":"2024-04-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10614-024-10597-2","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

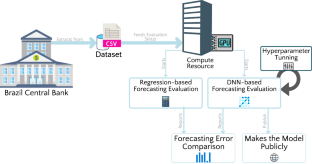

Artificial intelligence has shortened edges in many areas, especially the economy, to support long-term and accurate forecasting of financial indicators. Traditional statistical methods perform poorly compared to those based on artificial intelligence, which can achieve higher rates even with high-dimensional datasets. This method still needs evolution and studies. In emerging countries, decision-makers and investors must follow the basic interest rate, such as in Brazil, with a Special System of Settlement and Custody (Selic). Prior works used deep neural networks (DNNs) for forecasting time series economic indicators such as interest rates, inflation, and the stock market. However, there is no empirical evaluation of the prediction models for the Selic interest rate, especially the impact of training time and the optimization of hyperparameters. In this paper, we shed light on these issues and evaluate, through a fair comparison, the use of DNNs models for Selic time series forecasting. Our results demonstrate the potential of DNNs with an error rate above 0.00219 and training time above 84.28 s. Our findings open up opportunities for further investigations toward real-time interest rate forecasting, facilitating more reliable and timely forecasting of interest rates for decision-makers and investors.

期刊介绍:

Computational Economics, the official journal of the Society for Computational Economics, presents new research in a rapidly growing multidisciplinary field that uses advanced computing capabilities to understand and solve complex problems from all branches in economics. The topics of Computational Economics include computational methods in econometrics like filtering, bayesian and non-parametric approaches, markov processes and monte carlo simulation; agent based methods, machine learning, evolutionary algorithms, (neural) network modeling; computational aspects of dynamic systems, optimization, optimal control, games, equilibrium modeling; hardware and software developments, modeling languages, interfaces, symbolic processing, distributed and parallel processing

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们