{"title":"Earnings management and financial reports’ readability: moderating role of audit quality, cash holding, and ownership pattern","authors":"Chanchal Chatterjee","doi":"10.1057/s41310-024-00239-2","DOIUrl":null,"url":null,"abstract":"<p>The present study investigates how earnings management (EM) influences the readability of financial reports (readability) of top Indian firms. This study also examines whether cash holdings, audit quality, and ownership patterns moderate the relationship between EM and readability. To model this relationship, the study employs generalized methods of moments using 2184 management discussion and analysis (MDA) reports from 2017 to 2022. The paper examined earnings management under two different approaches: accrual-based [using Raman and Shahrur (Account Rev 83(4):1041–1081, 2008)] and real activity-based [using Lo et al. (J Account Econ 63:1–25, 2017)]. The study used the Gunning <i>fog index</i> to measure the readability of financial reports and the <i>Smog index</i> for robustness checks. The findings reveal that Indian firms that manage earnings publish complex MDA reports. Additionally, cash holdings, audit quality, and ownership patterns significantly moderate the relationship between EM and readability. Finally, findings show that COVID-19 pandemic has adversely affected the readability of financial reports. This study contributes to the limited number of studies in the global context, focusing on narrative accounting disclosures. On one hand, this study is the first of its kind performed in the Indian context, and on the other side, it contributes to the limited number of the literature in the global context focusing on the linguistic complexity of disclosures and its linkage with other relevant variables, especially ownership pattern, audit quality, and earnings management indicators.</p>","PeriodicalId":45050,"journal":{"name":"International Journal of Disclosure and Governance","volume":"36 1","pages":""},"PeriodicalIF":2.4000,"publicationDate":"2024-04-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Disclosure and Governance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41310-024-00239-2","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MANAGEMENT","Score":null,"Total":0}

引用次数: 0

Abstract

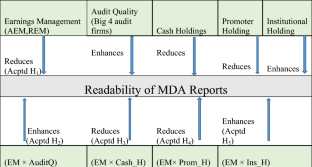

The present study investigates how earnings management (EM) influences the readability of financial reports (readability) of top Indian firms. This study also examines whether cash holdings, audit quality, and ownership patterns moderate the relationship between EM and readability. To model this relationship, the study employs generalized methods of moments using 2184 management discussion and analysis (MDA) reports from 2017 to 2022. The paper examined earnings management under two different approaches: accrual-based [using Raman and Shahrur (Account Rev 83(4):1041–1081, 2008)] and real activity-based [using Lo et al. (J Account Econ 63:1–25, 2017)]. The study used the Gunning fog index to measure the readability of financial reports and the Smog index for robustness checks. The findings reveal that Indian firms that manage earnings publish complex MDA reports. Additionally, cash holdings, audit quality, and ownership patterns significantly moderate the relationship between EM and readability. Finally, findings show that COVID-19 pandemic has adversely affected the readability of financial reports. This study contributes to the limited number of studies in the global context, focusing on narrative accounting disclosures. On one hand, this study is the first of its kind performed in the Indian context, and on the other side, it contributes to the limited number of the literature in the global context focusing on the linguistic complexity of disclosures and its linkage with other relevant variables, especially ownership pattern, audit quality, and earnings management indicators.

期刊介绍:

The International Journal of Disclosure and Governance publishes a balance between academic and practitioner perspectives in law and accounting on subjects related to corporate governance and disclosure. In its emphasis on practical issues, it is the only such journal in these fields. All rigorous and thoughtful conceptual papers are encouraged.

To date, International Journal of Disclosure and Governance has published articles by a former general counsel and a former commissioner of the SEC, practitioners from Cleary Gottlieb, Skadden Arps, Wachtell Lipton, and Latham & Watkins as well as articles by academics from Harvard, Yale and NYU. The readership of the journal includes lawyers, accountants, and corporate directors and managers.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们