{"title":"Innovation capital disclosure and independent directors: evidence from France","authors":"Fathia Elleuch Lahyani, Salma Damak Ayadi","doi":"10.1057/s41310-024-00241-8","DOIUrl":null,"url":null,"abstract":"<p>This study aims to understand whether corporate governance mechanisms affect innovation capital disclosure (ICD) provided voluntarily on corporate websites by SBF 120 listed firms in France. The study tests multivariate models using pooled OLS, random effects, and generalized method of moments models. Firms use ICD as a useful, timely communication tool to highlight their innovation efforts. Our findings suggest that independent non-executive directors (INEDs) exhibit a conservative approach to the nature of innovation that requires extensive investigations with risky outcomes. They support discretion by limiting the extent of publicly disclosed information about research and development (R&D) progress, technological advances, and innovation output to protect the firms’ intellectual proprietary. INEDs seem to balance preserving firms’ competitive advantage and ensuring higher transparency levels to satisfy stakeholders’ needs. Additionally, board tenure moderates the relationship between INEDs and ICD. This study underscores the importance of the financial reporting of information about innovation capital that captures firms’ innovation capacities in a knowledge-based economy. It provides significant insights for management, policy-makers, and regulators who are involved in refining corporate reporting policies. This study is the first to examine the incentives of INEDs in influencing reporting practices related to a firm’s innovation investments, particularly in high-technology firms.</p>","PeriodicalId":45050,"journal":{"name":"International Journal of Disclosure and Governance","volume":"25 1","pages":""},"PeriodicalIF":2.4000,"publicationDate":"2024-04-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Disclosure and Governance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41310-024-00241-8","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MANAGEMENT","Score":null,"Total":0}

引用次数: 0

Abstract

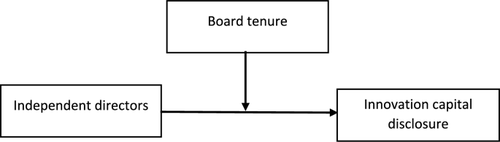

This study aims to understand whether corporate governance mechanisms affect innovation capital disclosure (ICD) provided voluntarily on corporate websites by SBF 120 listed firms in France. The study tests multivariate models using pooled OLS, random effects, and generalized method of moments models. Firms use ICD as a useful, timely communication tool to highlight their innovation efforts. Our findings suggest that independent non-executive directors (INEDs) exhibit a conservative approach to the nature of innovation that requires extensive investigations with risky outcomes. They support discretion by limiting the extent of publicly disclosed information about research and development (R&D) progress, technological advances, and innovation output to protect the firms’ intellectual proprietary. INEDs seem to balance preserving firms’ competitive advantage and ensuring higher transparency levels to satisfy stakeholders’ needs. Additionally, board tenure moderates the relationship between INEDs and ICD. This study underscores the importance of the financial reporting of information about innovation capital that captures firms’ innovation capacities in a knowledge-based economy. It provides significant insights for management, policy-makers, and regulators who are involved in refining corporate reporting policies. This study is the first to examine the incentives of INEDs in influencing reporting practices related to a firm’s innovation investments, particularly in high-technology firms.

期刊介绍:

The International Journal of Disclosure and Governance publishes a balance between academic and practitioner perspectives in law and accounting on subjects related to corporate governance and disclosure. In its emphasis on practical issues, it is the only such journal in these fields. All rigorous and thoughtful conceptual papers are encouraged.

To date, International Journal of Disclosure and Governance has published articles by a former general counsel and a former commissioner of the SEC, practitioners from Cleary Gottlieb, Skadden Arps, Wachtell Lipton, and Latham & Watkins as well as articles by academics from Harvard, Yale and NYU. The readership of the journal includes lawyers, accountants, and corporate directors and managers.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们