{"title":"Averaging Estimation for Instrumental Variables Quantile Regression","authors":"Xin Liu","doi":"10.1111/obes.12612","DOIUrl":null,"url":null,"abstract":"<p>This paper proposes two averaging estimation methods to improve the finite-sample efficiency of the instrumental variables quantile regression (IVQR) estimator. I propose using the usual quantile regression for averaging to take advantage of cases when endogeneity is not too strong. I also propose using two-stage least squares to take advantage of cases when heterogeneity is not too strong. The first averaging method is to apply a recent proposal for GMM averaging to the IVQR model based on this proposed intuition. My implementation involves many computational considerations and builds on recent developments in the quantile literature. The second averaging method is a new bootstrap model averaging method that directly averages among IVQR, quantile regression, and two-stage least squares estimators. More specifically, I find the optimal weights from bootstrapped samples and then apply the bootstrap-optimal weights to the original sample. The bootstrap method is simpler to compute and generally performs better in simulations, but uniform dominance results have not been formally proved. Simulation results demonstrate that in the multiple-regressors/instruments case, both the GMM averaging and bootstrap estimators have uniformly smaller risk than the IVQR estimator across data-generating processes with a variety of combinations of different endogeneity levels and heterogeneity levels.</p>","PeriodicalId":54654,"journal":{"name":"Oxford Bulletin of Economics and Statistics","volume":"86 5","pages":"1290-1312"},"PeriodicalIF":1.4000,"publicationDate":"2024-05-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/obes.12612","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Oxford Bulletin of Economics and Statistics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/obes.12612","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

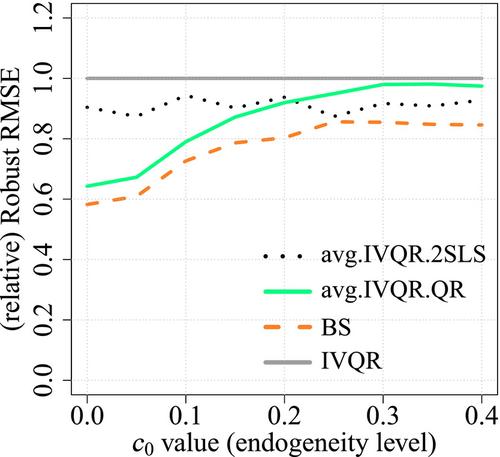

This paper proposes two averaging estimation methods to improve the finite-sample efficiency of the instrumental variables quantile regression (IVQR) estimator. I propose using the usual quantile regression for averaging to take advantage of cases when endogeneity is not too strong. I also propose using two-stage least squares to take advantage of cases when heterogeneity is not too strong. The first averaging method is to apply a recent proposal for GMM averaging to the IVQR model based on this proposed intuition. My implementation involves many computational considerations and builds on recent developments in the quantile literature. The second averaging method is a new bootstrap model averaging method that directly averages among IVQR, quantile regression, and two-stage least squares estimators. More specifically, I find the optimal weights from bootstrapped samples and then apply the bootstrap-optimal weights to the original sample. The bootstrap method is simpler to compute and generally performs better in simulations, but uniform dominance results have not been formally proved. Simulation results demonstrate that in the multiple-regressors/instruments case, both the GMM averaging and bootstrap estimators have uniformly smaller risk than the IVQR estimator across data-generating processes with a variety of combinations of different endogeneity levels and heterogeneity levels.

期刊介绍:

Whilst the Oxford Bulletin of Economics and Statistics publishes papers in all areas of applied economics, emphasis is placed on the practical importance, theoretical interest and policy-relevance of their substantive results, as well as on the methodology and technical competence of the research.

Contributions on the topical issues of economic policy and the testing of currently controversial economic theories are encouraged, as well as more empirical research on both developed and developing countries.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们