Xavier Martínez-Barbero, Roberto Cervelló-Royo, Javier Ribal

{"title":"Portfolio Optimization with Prediction-Based Return Using Long Short-Term Memory Neural Networks: Testing on Upward and Downward European Markets","authors":"Xavier Martínez-Barbero, Roberto Cervelló-Royo, Javier Ribal","doi":"10.1007/s10614-024-10604-6","DOIUrl":null,"url":null,"abstract":"<p>In recent years, artificial intelligence has helped to improve processes and performance in many different areas: in the field of portfolio optimization, the inputs play a crucial role, and the use of machine learning algorithms can improve the estimation of the inputs to create robust portfolios able to generate returns consistently. This paper combines classical mean–variance optimization and machine learning techniques, concretely long short-term memory neural networks to provide more accurate predicted returns and generate profitable portfolios for 10 holding periods that present different financial contexts. The proposed algorithm is trained and tested with historical EURO STOXX 50® Index data from January 2015 to December 2020, and from January 2021 to June 2022, respectively. Empirical results show that our LSTM neural networks are able to achieve minor predictive errors since the average of the MSE of the 10 holding periods is 0.00047, the average of the MAE is 0.01634, and predict the direction of returns with an average accuracy over the 10 investment periods of 95.8%. Our prediction-based portfolios consistently beat the EURO STOXX 50® Index, achieving superior positive results even during bear markets.</p>","PeriodicalId":50647,"journal":{"name":"Computational Economics","volume":"61 1","pages":""},"PeriodicalIF":2.2000,"publicationDate":"2024-05-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10614-024-10604-6","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

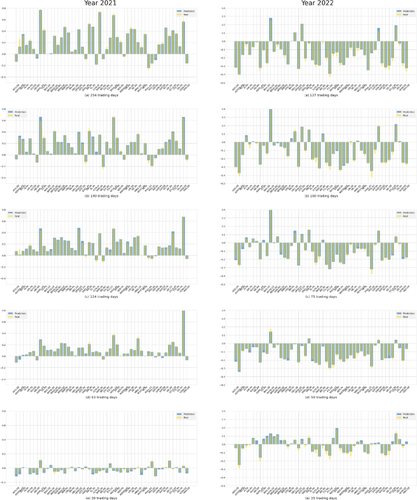

In recent years, artificial intelligence has helped to improve processes and performance in many different areas: in the field of portfolio optimization, the inputs play a crucial role, and the use of machine learning algorithms can improve the estimation of the inputs to create robust portfolios able to generate returns consistently. This paper combines classical mean–variance optimization and machine learning techniques, concretely long short-term memory neural networks to provide more accurate predicted returns and generate profitable portfolios for 10 holding periods that present different financial contexts. The proposed algorithm is trained and tested with historical EURO STOXX 50® Index data from January 2015 to December 2020, and from January 2021 to June 2022, respectively. Empirical results show that our LSTM neural networks are able to achieve minor predictive errors since the average of the MSE of the 10 holding periods is 0.00047, the average of the MAE is 0.01634, and predict the direction of returns with an average accuracy over the 10 investment periods of 95.8%. Our prediction-based portfolios consistently beat the EURO STOXX 50® Index, achieving superior positive results even during bear markets.

期刊介绍:

Computational Economics, the official journal of the Society for Computational Economics, presents new research in a rapidly growing multidisciplinary field that uses advanced computing capabilities to understand and solve complex problems from all branches in economics. The topics of Computational Economics include computational methods in econometrics like filtering, bayesian and non-parametric approaches, markov processes and monte carlo simulation; agent based methods, machine learning, evolutionary algorithms, (neural) network modeling; computational aspects of dynamic systems, optimization, optimal control, games, equilibrium modeling; hardware and software developments, modeling languages, interfaces, symbolic processing, distributed and parallel processing

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们