{"title":"Nowcasting Euro area GDP with news sentiment: A tale of two crises","authors":"Julian Ashwin, Eleni Kalamara, Lorena Saiz","doi":"10.1002/jae.3057","DOIUrl":null,"url":null,"abstract":"<p>This paper shows that newspaper articles contain signals that can materially improve real-time nowcasts of real GDP growth for the Euro area. Using articles from 15 popular European newspapers, which are machine translated into English, we create sentiment metrics that update daily and assess their value for nowcasting, comparing with competitive and rigorous benchmarks. We find that newspaper text is especially helpful early in the quarter before other indicators are available. We also find that general-purpose sentiment measures perform better than more economics-focused ones in response to unanticipated events and nonlinear supervised models can help capture extreme movements in growth but require sufficient training data to be effective.</p>","PeriodicalId":48363,"journal":{"name":"Journal of Applied Econometrics","volume":"39 5","pages":"887-905"},"PeriodicalIF":3.1000,"publicationDate":"2024-05-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3057","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Econometrics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jae.3057","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

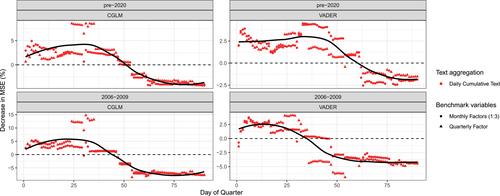

This paper shows that newspaper articles contain signals that can materially improve real-time nowcasts of real GDP growth for the Euro area. Using articles from 15 popular European newspapers, which are machine translated into English, we create sentiment metrics that update daily and assess their value for nowcasting, comparing with competitive and rigorous benchmarks. We find that newspaper text is especially helpful early in the quarter before other indicators are available. We also find that general-purpose sentiment measures perform better than more economics-focused ones in response to unanticipated events and nonlinear supervised models can help capture extreme movements in growth but require sufficient training data to be effective.

期刊介绍:

The Journal of Applied Econometrics is an international journal published bi-monthly, plus 1 additional issue (total 7 issues). It aims to publish articles of high quality dealing with the application of existing as well as new econometric techniques to a wide variety of problems in economics and related subjects, covering topics in measurement, estimation, testing, forecasting, and policy analysis. The emphasis is on the careful and rigorous application of econometric techniques and the appropriate interpretation of the results. The economic content of the articles is stressed. A special feature of the Journal is its emphasis on the replicability of results by other researchers. To achieve this aim, authors are expected to make available a complete set of the data used as well as any specialised computer programs employed through a readily accessible medium, preferably in a machine-readable form. The use of microcomputers in applied research and transferability of data is emphasised. The Journal also features occasional sections of short papers re-evaluating previously published papers. The intention of the Journal of Applied Econometrics is to provide an outlet for innovative, quantitative research in economics which cuts across areas of specialisation, involves transferable techniques, and is easily replicable by other researchers. Contributions that introduce statistical methods that are applicable to a variety of economic problems are actively encouraged. The Journal also aims to publish review and survey articles that make recent developments in the field of theoretical and applied econometrics more readily accessible to applied economists in general.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们