{"title":"PCA-ICA-LSTM: A Hybrid Deep Learning Model Based on Dimension Reduction Methods to Predict S&P 500 Index Price","authors":"Mehmet Sarıkoç, Mete Celik","doi":"10.1007/s10614-024-10629-x","DOIUrl":null,"url":null,"abstract":"<p>In this paper, we propose a new hybrid model based on a deep learning network to predict the prices of financial assets. The study addresses two key limitations in existing research: (1) the lack of standardized datasets, time scales, and evaluation metrics, and (2) the focus on prediction return. The proposed model employs a two-stage preprocessing approach utilizing Principal Component Analysis (PCA) for dimensionality reduction and de-noising, followed by Independent Component Analysis (ICA) for feature extraction. A Long Short-Term Memory (LSTM) network with five layers is fed with this preprocessed data to predict the price of the next day using a 5 day time horizon. To ensure comparability with existing literature, experiments employ an 18 year dataset of the Standard & Poor's 500 (S&P500) index and include over 40 technical indicators. Performance evaluation encompasses six metrics, highlighting the model's superiority in accuracy and return rates. Comparative analyses demonstrate the superiority of the proposed PCA-ICA-LSTM model over single-stage statistical methods and other deep learning architectures, achieving notable improvements in evaluation metrics. Evaluation against previous studies using similar datasets corroborates the model's superior performance. Moreover, extensions to the study include adjustments to dataset parameters to account for the COVID-19 pandemic, resulting in improved return rates surpassing traditional trading strategies. PCA-ICA-LSTM achieves a 220% higher return compared to the “hold and wait” strategy in the extended S&P500 dataset, along with a 260% higher return than its closest competitor in the comparison. Furthermore, it outperformed other models in additional case studies.</p><h3 data-test=\"abstract-sub-heading\">Graphical Abstract</h3>","PeriodicalId":50647,"journal":{"name":"Computational Economics","volume":"4 1","pages":""},"PeriodicalIF":2.2000,"publicationDate":"2024-05-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10614-024-10629-x","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

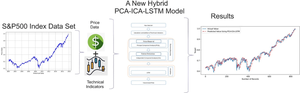

Abstract

In this paper, we propose a new hybrid model based on a deep learning network to predict the prices of financial assets. The study addresses two key limitations in existing research: (1) the lack of standardized datasets, time scales, and evaluation metrics, and (2) the focus on prediction return. The proposed model employs a two-stage preprocessing approach utilizing Principal Component Analysis (PCA) for dimensionality reduction and de-noising, followed by Independent Component Analysis (ICA) for feature extraction. A Long Short-Term Memory (LSTM) network with five layers is fed with this preprocessed data to predict the price of the next day using a 5 day time horizon. To ensure comparability with existing literature, experiments employ an 18 year dataset of the Standard & Poor's 500 (S&P500) index and include over 40 technical indicators. Performance evaluation encompasses six metrics, highlighting the model's superiority in accuracy and return rates. Comparative analyses demonstrate the superiority of the proposed PCA-ICA-LSTM model over single-stage statistical methods and other deep learning architectures, achieving notable improvements in evaluation metrics. Evaluation against previous studies using similar datasets corroborates the model's superior performance. Moreover, extensions to the study include adjustments to dataset parameters to account for the COVID-19 pandemic, resulting in improved return rates surpassing traditional trading strategies. PCA-ICA-LSTM achieves a 220% higher return compared to the “hold and wait” strategy in the extended S&P500 dataset, along with a 260% higher return than its closest competitor in the comparison. Furthermore, it outperformed other models in additional case studies.

期刊介绍:

Computational Economics, the official journal of the Society for Computational Economics, presents new research in a rapidly growing multidisciplinary field that uses advanced computing capabilities to understand and solve complex problems from all branches in economics. The topics of Computational Economics include computational methods in econometrics like filtering, bayesian and non-parametric approaches, markov processes and monte carlo simulation; agent based methods, machine learning, evolutionary algorithms, (neural) network modeling; computational aspects of dynamic systems, optimization, optimal control, games, equilibrium modeling; hardware and software developments, modeling languages, interfaces, symbolic processing, distributed and parallel processing

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们