{"title":"Forecasting Bitcoin returns: Econometric time series analysis vs. machine learning","authors":"Theo Berger, Jana Koubová","doi":"10.1002/for.3165","DOIUrl":null,"url":null,"abstract":"<p>We study the statistical properties of the Bitcoin return series and provide a thorough forecasting exercise. Also, we calibrate state-of-the-art machine learning techniques and compare the results with econometric time series models. The empirical assessment provides evidence that the application of machine learning techniques outperforms econometric benchmarks in terms of forecasting precision for both in- and out-of-sample forecasts. We find that both deep learning architectures as well as complex layers, such as LSTM, do not increase the precision of daily forecasts. Specifically, a simple recurrent neural network describes a sensible choice for forecasting daily return series.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"43 7","pages":"2904-2916"},"PeriodicalIF":2.7000,"publicationDate":"2024-05-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3165","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3165","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

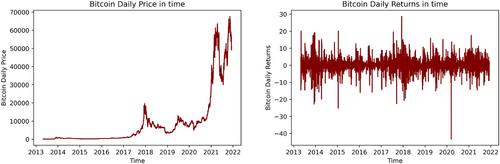

We study the statistical properties of the Bitcoin return series and provide a thorough forecasting exercise. Also, we calibrate state-of-the-art machine learning techniques and compare the results with econometric time series models. The empirical assessment provides evidence that the application of machine learning techniques outperforms econometric benchmarks in terms of forecasting precision for both in- and out-of-sample forecasts. We find that both deep learning architectures as well as complex layers, such as LSTM, do not increase the precision of daily forecasts. Specifically, a simple recurrent neural network describes a sensible choice for forecasting daily return series.

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们