Benjamin Salomon Diboma , Flavian Emmanuel Sapnken , Mohammed Hamaidi , Yong Wang , Prosper Gopdjim Noumo , Jean Gaston Tamba

{"title":"Improved exponential smoothing grey-holt models for electricity price forecasting using whale optimization","authors":"Benjamin Salomon Diboma , Flavian Emmanuel Sapnken , Mohammed Hamaidi , Yong Wang , Prosper Gopdjim Noumo , Jean Gaston Tamba","doi":"10.1016/j.mex.2024.102926","DOIUrl":null,"url":null,"abstract":"<div><p>This study introduces a ground-breaking approach, the Whale Optimization Algorithm (WOA)-based multivariate exponential smoothing Grey-Holt (GMHES) model, designed for electricity price forecasting. Key features of the proposed WOA-GMHES(1,N) model include leveraging historical data to comprehend the underlying trends in electricity prices and utilizing the WOA algorithm for adaptive optimization of model parameters to capture evolving market dynamics. Evaluating the model on authentic high- and low-voltage electricity price data from Cameroon demonstrates its superiority over competing models. The WOA-GMHES(1,N) model achieves remarkable performance with RMSE and SMAPE scores of 12.63 and 0.01 %, respectively, showcasing its accuracy and reliability. Notably, the model proves to be computationally efficient, generating forecasts in <1.3 s. Three key aspects of customization distinguish this novel approach:</p><ul><li><span>•</span><span><p>The WOA algorithm dynamically adjusts model parameters based on evolving electricity market dynamics.</p></span></li><li><span>•</span><span><p>The model employs a sophisticated GMHES approach, considering multiple factors for a comprehensive understanding of price trends.</p></span></li><li><span>•</span><span><p>The WOA-GMHES(1,N) model stands out for its computational efficiency, providing rapid and precise forecasts, making it a valuable tool for time-sensitive decision-making in the energy sector.</p></span></li></ul></div>","PeriodicalId":18446,"journal":{"name":"MethodsX","volume":"13 ","pages":"Article 102926"},"PeriodicalIF":1.9000,"publicationDate":"2024-12-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.sciencedirect.com/science/article/pii/S2215016124003777/pdfft?md5=b3de9678a248d83a65c1392c037eb07a&pid=1-s2.0-S2215016124003777-main.pdf","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"MethodsX","FirstCategoryId":"1085","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S2215016124003777","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2024/9/1 0:00:00","PubModel":"Epub","JCR":"Q2","JCRName":"MULTIDISCIPLINARY SCIENCES","Score":null,"Total":0}

引用次数: 0

Abstract

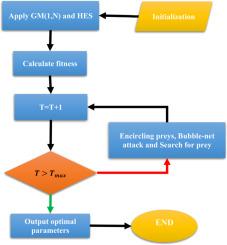

This study introduces a ground-breaking approach, the Whale Optimization Algorithm (WOA)-based multivariate exponential smoothing Grey-Holt (GMHES) model, designed for electricity price forecasting. Key features of the proposed WOA-GMHES(1,N) model include leveraging historical data to comprehend the underlying trends in electricity prices and utilizing the WOA algorithm for adaptive optimization of model parameters to capture evolving market dynamics. Evaluating the model on authentic high- and low-voltage electricity price data from Cameroon demonstrates its superiority over competing models. The WOA-GMHES(1,N) model achieves remarkable performance with RMSE and SMAPE scores of 12.63 and 0.01 %, respectively, showcasing its accuracy and reliability. Notably, the model proves to be computationally efficient, generating forecasts in <1.3 s. Three key aspects of customization distinguish this novel approach:

•

The WOA algorithm dynamically adjusts model parameters based on evolving electricity market dynamics.

•

The model employs a sophisticated GMHES approach, considering multiple factors for a comprehensive understanding of price trends.

•

The WOA-GMHES(1,N) model stands out for its computational efficiency, providing rapid and precise forecasts, making it a valuable tool for time-sensitive decision-making in the energy sector.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们