Fahim Afzal, Haiying Pan, Farman Afzal, Rana Faizan Gul

{"title":"Analyzing risk contagion and volatility spillover across multi-market capital flow using EVT theory and C-vine Copula.","authors":"Fahim Afzal, Haiying Pan, Farman Afzal, Rana Faizan Gul","doi":"10.1016/j.heliyon.2024.e39918","DOIUrl":null,"url":null,"abstract":"<p><p>There exists a potential interdependence among the United States markets, alongside an exceptional dependence on the East Asian stock markets. This transmission of risks is similarly evident in funds that are traded within markets. The current study seeks to uncover the pathways of risk contagion among various financial markets. This study examines how risks of funds spread across borders among China, the United States, and East Asia using Extreme Value Theory (EVT) and C vine copula quantile regression. It uses models such as AR (1), EGARCH (1, 1), Peak over Threshold (POT), and Copula methods to predict volatility events and correlation patterns during times of high volatility versus regular periods. Notably, the United States exhibits a risk transmission effect on the East Asian market compared to China. Furthermore, the findings indicate that, in times of high volatility, the risk spillover effect is comparatively weak, which is contrary to the situation of the US market. The study suggests that China's financial impact could progressively rise due to initiatives aimed at sector integration and enhancing financial independence. These findings have enlightening consequences for macro-prudential regulatory agencies, emphasizing the necessity of effective regulation to address cross-border risk spillovers. International investors can benefit from these results by incorporating risk-hedging strategies, accurately evaluating derivatives, and making wise investment decisions.</p>","PeriodicalId":12894,"journal":{"name":"Heliyon","volume":"10 21","pages":"e39918"},"PeriodicalIF":3.6000,"publicationDate":"2024-10-29","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC11564031/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Heliyon","FirstCategoryId":"103","ListUrlMain":"https://doi.org/10.1016/j.heliyon.2024.e39918","RegionNum":3,"RegionCategory":"综合性期刊","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2024/11/15 0:00:00","PubModel":"eCollection","JCR":"Q1","JCRName":"MULTIDISCIPLINARY SCIENCES","Score":null,"Total":0}

引用次数: 0

Abstract

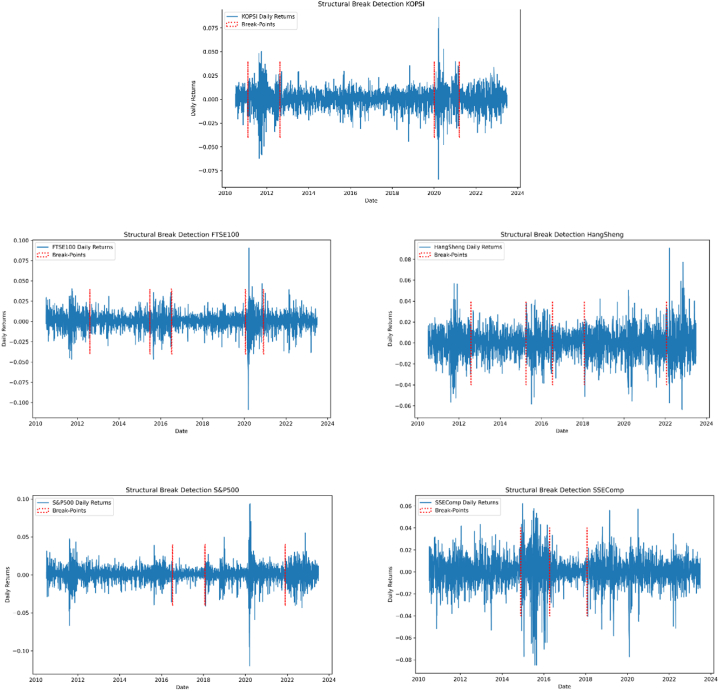

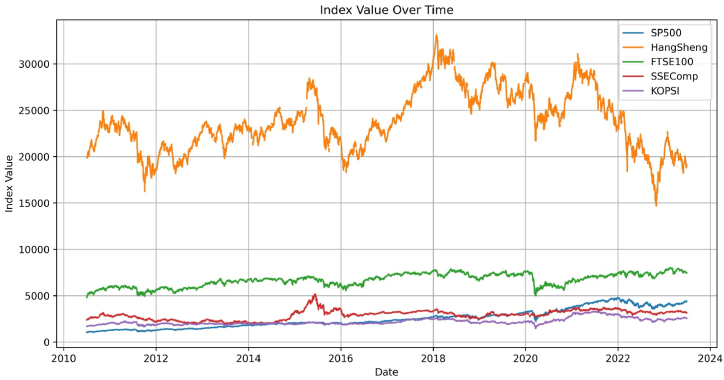

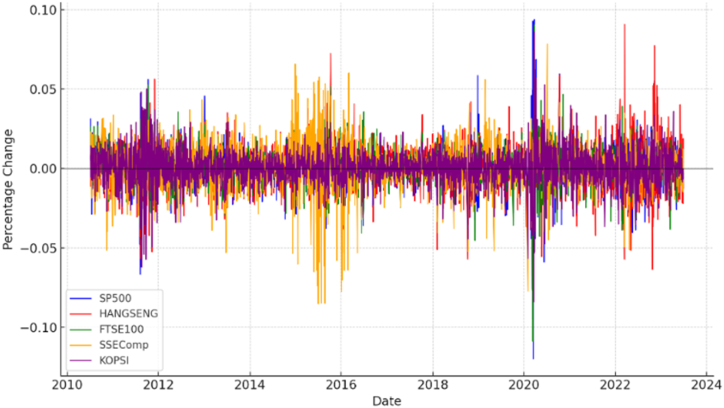

There exists a potential interdependence among the United States markets, alongside an exceptional dependence on the East Asian stock markets. This transmission of risks is similarly evident in funds that are traded within markets. The current study seeks to uncover the pathways of risk contagion among various financial markets. This study examines how risks of funds spread across borders among China, the United States, and East Asia using Extreme Value Theory (EVT) and C vine copula quantile regression. It uses models such as AR (1), EGARCH (1, 1), Peak over Threshold (POT), and Copula methods to predict volatility events and correlation patterns during times of high volatility versus regular periods. Notably, the United States exhibits a risk transmission effect on the East Asian market compared to China. Furthermore, the findings indicate that, in times of high volatility, the risk spillover effect is comparatively weak, which is contrary to the situation of the US market. The study suggests that China's financial impact could progressively rise due to initiatives aimed at sector integration and enhancing financial independence. These findings have enlightening consequences for macro-prudential regulatory agencies, emphasizing the necessity of effective regulation to address cross-border risk spillovers. International investors can benefit from these results by incorporating risk-hedging strategies, accurately evaluating derivatives, and making wise investment decisions.

美国市场之间存在着潜在的相互依存关系,同时对东亚股票市场也存在着特殊的依赖性。这种风险传染在市场内交易的基金中同样明显。本研究试图揭示不同金融市场之间风险传染的途径。本研究利用极值理论(EVT)和 C vine copula 量子回归法研究了基金风险如何在中国、美国和东亚之间跨境传播。研究使用了 AR (1)、EGARCH (1,1)、Peak over Threshold (POT) 和 Copula 等模型来预测高波动期与正常波动期的波动事件和相关模式。值得注意的是,与中国相比,美国对东亚市场表现出风险传导效应。此外,研究结果表明,在高波动率时期,风险溢出效应相对较弱,这与美国市场的情况相反。研究表明,中国的金融影响力可能会因行业整合和增强金融独立性的举措而逐步上升。这些研究结果对宏观审慎监管机构具有启发意义,强调了有效监管以应对跨境风险溢出的必要性。国际投资者可以从这些结果中获益,纳入风险对冲策略,准确评估衍生工具,做出明智的投资决策。

期刊介绍:

Heliyon is an all-science, open access journal that is part of the Cell Press family. Any paper reporting scientifically accurate and valuable research, which adheres to accepted ethical and scientific publishing standards, will be considered for publication. Our growing team of dedicated section editors, along with our in-house team, handle your paper and manage the publication process end-to-end, giving your research the editorial support it deserves.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们