{"title":"Cryptocurrency volatility markets.","authors":"Fabian Woebbeking","doi":"10.1007/s42521-021-00037-3","DOIUrl":null,"url":null,"abstract":"<p><p>By computing a volatility index (CVX) from cryptocurrency option prices, we analyze this market's expectation of future volatility. Our method addresses the challenging liquidity environment of this young asset class and allows us to extract stable market implied volatilities. Two alternative methods are considered to compute volatilities from granular intra-day cryptocurrency options data, which spans over the COVID-19 pandemic period. CVX data therefore capture 'normal' market dynamics as well as distress and recovery periods. The methods yield two cointegrated index series, where the corresponding error correction model can be used as an indicator for market implied tail-risk. Comparing our CVX to existing volatility benchmarks for traditional asset classes, such as VIX (equity) or GVX (gold), confirms that cryptocurrency volatility dynamics are often disconnected from traditional markets, yet, share common shocks.</p>","PeriodicalId":72817,"journal":{"name":"Digital finance","volume":"3 3-4","pages":"273-298"},"PeriodicalIF":0.0000,"publicationDate":"2021-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1007/s42521-021-00037-3","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Digital finance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s42521-021-00037-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/8/2 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

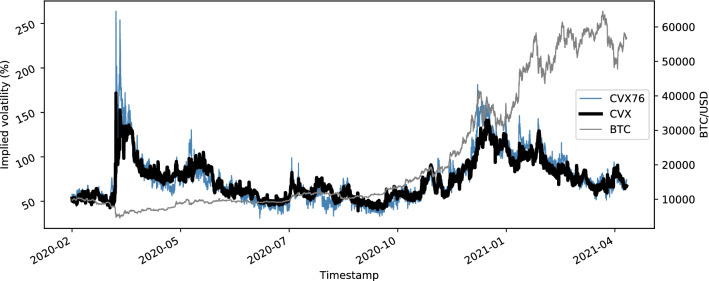

By computing a volatility index (CVX) from cryptocurrency option prices, we analyze this market's expectation of future volatility. Our method addresses the challenging liquidity environment of this young asset class and allows us to extract stable market implied volatilities. Two alternative methods are considered to compute volatilities from granular intra-day cryptocurrency options data, which spans over the COVID-19 pandemic period. CVX data therefore capture 'normal' market dynamics as well as distress and recovery periods. The methods yield two cointegrated index series, where the corresponding error correction model can be used as an indicator for market implied tail-risk. Comparing our CVX to existing volatility benchmarks for traditional asset classes, such as VIX (equity) or GVX (gold), confirms that cryptocurrency volatility dynamics are often disconnected from traditional markets, yet, share common shocks.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们