Economic policy uncertainty, investor sentiment and financial stability-an empirical study based on the time varying parameter-vector autoregression model.

{"title":"Economic policy uncertainty, investor sentiment and financial stability-an empirical study based on the time varying parameter-vector autoregression model.","authors":"Xin-Zhou Qi, Zhong Ning, Meng Qin","doi":"10.1007/s11403-021-00342-5","DOIUrl":null,"url":null,"abstract":"<p><p>This paper applies the time varying parameter-vector autoregression model to explore the dynamic relationship between economic policy uncertainty, investor sentiment and financial stability in China in different periods and at different time points. The empirical results show that economic policy uncertainty has an obvious negative impact on investor sentiment before 2012 and financial stability in the short term, and the influence of economic policy uncertainty on investor sentiment is greater than that of economic policy uncertainty on financial stability. These influences were more significant during the period of the global financial crisis in 2008. Moreover, investor sentiment had a positive and gradually increasing effect on financial stability, while after 2010, the positive impact gradually weakened. Furthermore, economic policy uncertainty is negatively affected by financial stability, and the effect of financial stability on investor sentiment is positive. In terms of mediating effects, economic policy uncertainty has an indirect impact on financial stability through investor sentiment and vice versa. This paper provides a new solution to economic problems explored in behavioral finance research. Additionally, Chinese government agencies can achieve the goal of preventing financial crises and maintaining financial stability by monitoring investor sentiment and implementing targeted economic policies.</p>","PeriodicalId":45479,"journal":{"name":"Journal of Economic Interaction and Coordination","volume":"17 3","pages":"779-799"},"PeriodicalIF":1.0000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8713736/pdf/","citationCount":"7","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Economic Interaction and Coordination","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11403-021-00342-5","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/12/28 0:00:00","PubModel":"Epub","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 7

Abstract

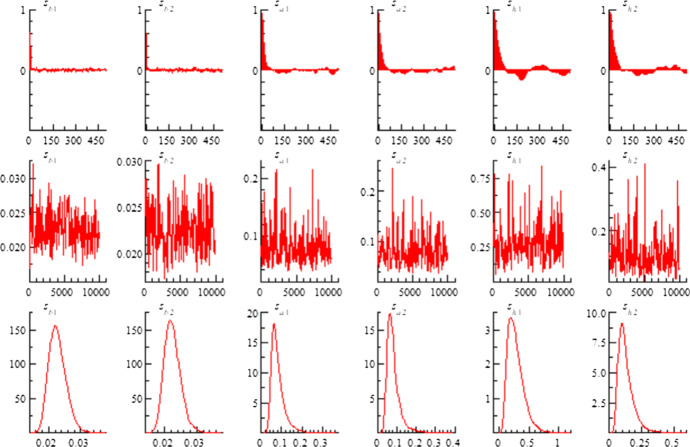

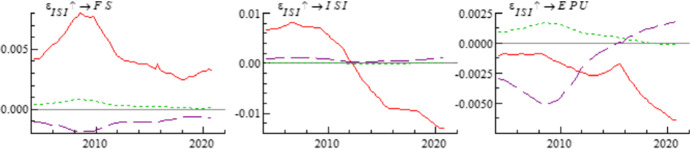

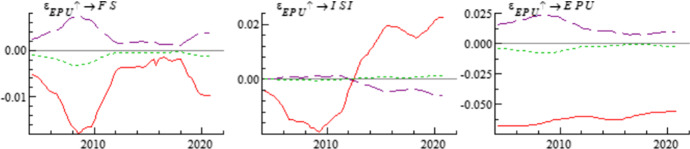

This paper applies the time varying parameter-vector autoregression model to explore the dynamic relationship between economic policy uncertainty, investor sentiment and financial stability in China in different periods and at different time points. The empirical results show that economic policy uncertainty has an obvious negative impact on investor sentiment before 2012 and financial stability in the short term, and the influence of economic policy uncertainty on investor sentiment is greater than that of economic policy uncertainty on financial stability. These influences were more significant during the period of the global financial crisis in 2008. Moreover, investor sentiment had a positive and gradually increasing effect on financial stability, while after 2010, the positive impact gradually weakened. Furthermore, economic policy uncertainty is negatively affected by financial stability, and the effect of financial stability on investor sentiment is positive. In terms of mediating effects, economic policy uncertainty has an indirect impact on financial stability through investor sentiment and vice versa. This paper provides a new solution to economic problems explored in behavioral finance research. Additionally, Chinese government agencies can achieve the goal of preventing financial crises and maintaining financial stability by monitoring investor sentiment and implementing targeted economic policies.

期刊介绍:

Journal of Economic Interaction and Coordination addresses the vibrant and interdisciplinary field of agent-based approaches to economics and social sciences.

It focuses on simulating and synthesizing emergent phenomena and collective behavior in order to understand economic and social systems. Relevant topics include, but are not limited to, the following: markets as complex adaptive systems, multi-agents in economics, artificial markets with heterogeneous agents, financial markets with heterogeneous agents, theory and simulation of agent-based models, adaptive agents with artificial intelligence, interacting particle systems in economics, social and complex networks, econophysics, non-linear economic dynamics, evolutionary games, market mechanisms in distributed computing systems, experimental economics, collective decisions.

Contributions are mostly from economics, physics, computer science and related fields and are typically based on sound theoretical models and supported by experimental validation. Survey papers are also welcome.

Journal of Economic Interaction and Coordination is the official journal of the Association of Economic Science with Heterogeneous Interacting Agents.

Officially cited as: J Econ Interact Coord

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们