{"title":"Derivatives-based portfolio decisions: an expected utility insight","authors":"Marcos Escobar-Anel, Matt Davison, Yichen Zhu","doi":"10.1007/s10436-022-00409-8","DOIUrl":null,"url":null,"abstract":"<div><p>This paper challenges the use of stocks in portfolio construction, instead we demonstrate that Asian derivatives, straddles, or baskets could be more convenient substitutes. Our results are obtained under the assumptions of the Black–Scholes–Merton setting, uncovering a hidden benefit of derivatives that complements their well-known gains for hedging, risk management, and to increase utility in market incompleteness. The new insights are also transferable to more advanced stochastic settings. The analysis relies on the infinite number of optimal choices of derivatives for a maximized expected utility theory agent; we propose risk exposure minimization as an additional optimization criterion inspired by regulations. Working with two assets, for simplicity, we demonstrate that only two derivatives are needed to maximize utility while minimizing risky exposure. In a comparison among one-asset options, e.g. American, European, Asian, Calls and Puts, we demonstrate that the deepest out-of-the-money Asian products available are the best choices to minimize exposure. We also explore optimal selections among straddles, which are better practical choice than out-of-the-money Calls and Puts due to liquidity and rebalancing needs. The optimality of multi-asset derivatives is also considered, establishing that a basket option could be a better choice than one-asset Asian call/put in many realistic situations.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":"18 2","pages":"217 - 246"},"PeriodicalIF":0.7000,"publicationDate":"2022-04-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://link.springer.com/content/pdf/10.1007/s10436-022-00409-8.pdf","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-022-00409-8","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 1

Abstract

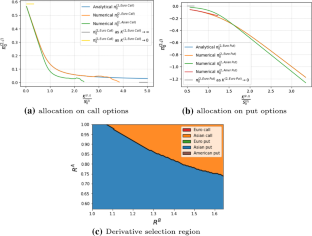

This paper challenges the use of stocks in portfolio construction, instead we demonstrate that Asian derivatives, straddles, or baskets could be more convenient substitutes. Our results are obtained under the assumptions of the Black–Scholes–Merton setting, uncovering a hidden benefit of derivatives that complements their well-known gains for hedging, risk management, and to increase utility in market incompleteness. The new insights are also transferable to more advanced stochastic settings. The analysis relies on the infinite number of optimal choices of derivatives for a maximized expected utility theory agent; we propose risk exposure minimization as an additional optimization criterion inspired by regulations. Working with two assets, for simplicity, we demonstrate that only two derivatives are needed to maximize utility while minimizing risky exposure. In a comparison among one-asset options, e.g. American, European, Asian, Calls and Puts, we demonstrate that the deepest out-of-the-money Asian products available are the best choices to minimize exposure. We also explore optimal selections among straddles, which are better practical choice than out-of-the-money Calls and Puts due to liquidity and rebalancing needs. The optimality of multi-asset derivatives is also considered, establishing that a basket option could be a better choice than one-asset Asian call/put in many realistic situations.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们