{"title":"Tests for the existence of group effects and interactions for two-way models with dependent errors","authors":"Yuichi Goto, Kotone Suzuki, Xiaofei Xu, Masanobu Taniguchi","doi":"10.1007/s10463-022-00853-3","DOIUrl":null,"url":null,"abstract":"<div><p>In this paper, we propose tests for the existence of random effects and interactions for two-way models with dependent errors. We prove that the proposed tests are asymptotically distribution-free which have asymptotically size <span>\\({{\\tau }}\\)</span> and are consistent. We elucidate the nontrivial power under the local alternative when a sample size tends to infinity and the number of groups is fixed. A simulation study is performed to investigate the finite-sample performance of the proposed tests. In the real data analysis, we apply our tests to the daily log-returns of 24 stock prices from six countries and four sectors. We find that there is no strong evidence to support the existence of substantial differences in the log-return across countries, nor to the existence of interactions between countries and sectors. However, there exists random effect differences in the daily log-return series across different sectors.</p></div>","PeriodicalId":55511,"journal":{"name":"Annals of the Institute of Statistical Mathematics","volume":"75 3","pages":"511 - 532"},"PeriodicalIF":0.6000,"publicationDate":"2022-10-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of the Institute of Statistical Mathematics","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1007/s10463-022-00853-3","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

引用次数: 0

Abstract

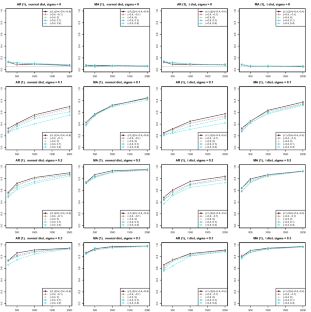

In this paper, we propose tests for the existence of random effects and interactions for two-way models with dependent errors. We prove that the proposed tests are asymptotically distribution-free which have asymptotically size \({{\tau }}\) and are consistent. We elucidate the nontrivial power under the local alternative when a sample size tends to infinity and the number of groups is fixed. A simulation study is performed to investigate the finite-sample performance of the proposed tests. In the real data analysis, we apply our tests to the daily log-returns of 24 stock prices from six countries and four sectors. We find that there is no strong evidence to support the existence of substantial differences in the log-return across countries, nor to the existence of interactions between countries and sectors. However, there exists random effect differences in the daily log-return series across different sectors.

期刊介绍:

Annals of the Institute of Statistical Mathematics (AISM) aims to provide a forum for open communication among statisticians, and to contribute to the advancement of statistics as a science to enable humans to handle information in order to cope with uncertainties. It publishes high-quality papers that shed new light on the theoretical, computational and/or methodological aspects of statistical science. Emphasis is placed on (a) development of new methodologies motivated by real data, (b) development of unifying theories, and (c) analysis and improvement of existing methodologies and theories.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们