{"title":"A new unique impulse response function in linear vector autoregressive models","authors":"Yanlin Shi","doi":"10.1111/irfi.12396","DOIUrl":null,"url":null,"abstract":"<p>This article proposes a new unique impulse response function (IRF) measure, or MIRF, based on the popular vector autoregressive model to study interdependency of multivariate time series. Same as the orthogonal IRF, the estimator of MIRF has an analytical form with well-established asymptotics, and is invariant to ordering of series. Compared to alternative unique IRF measures, MIRF does not depend on extreme identifications, and the associated forecast error variance measure is explainable. An illustrative empirical example is also provided.</p>","PeriodicalId":46664,"journal":{"name":"International Review of Finance","volume":"23 2","pages":"460-468"},"PeriodicalIF":2.6000,"publicationDate":"2022-10-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/irfi.12396","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Review of Finance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/irfi.12396","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

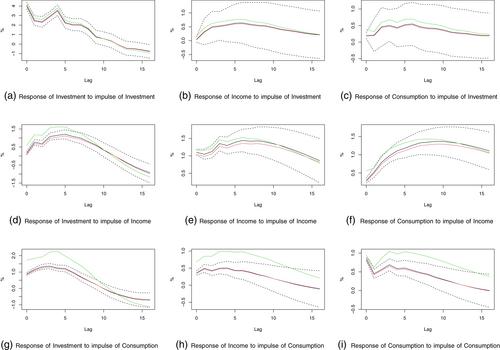

Abstract

This article proposes a new unique impulse response function (IRF) measure, or MIRF, based on the popular vector autoregressive model to study interdependency of multivariate time series. Same as the orthogonal IRF, the estimator of MIRF has an analytical form with well-established asymptotics, and is invariant to ordering of series. Compared to alternative unique IRF measures, MIRF does not depend on extreme identifications, and the associated forecast error variance measure is explainable. An illustrative empirical example is also provided.

期刊介绍:

The International Review of Finance (IRF) publishes high-quality research on all aspects of financial economics, including traditional areas such as asset pricing, corporate finance, market microstructure, financial intermediation and regulation, financial econometrics, financial engineering and risk management, as well as new areas such as markets and institutions of emerging market economies, especially those in the Asia-Pacific region. In addition, the Letters Section in IRF is a premium outlet of letter-length research in all fields of finance. The length of the articles in the Letters Section is limited to a maximum of eight journal pages.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们