Matteo Bonato, Oğuzhan Çepni, Rangan Gupta, Christian Pierdzioch

{"title":"Uncertainty due to infectious diseases and forecastability of the realized variance of United States real estate investment trusts: A note","authors":"Matteo Bonato, Oğuzhan Çepni, Rangan Gupta, Christian Pierdzioch","doi":"10.1111/irfi.12357","DOIUrl":null,"url":null,"abstract":"<p>We examine the forecasting power of a daily newspaper-based index of uncertainty associated with infectious diseases (EMVID) for real estate investment trusts (REITs) realized market variance of the United States (US) via the heterogeneous autoregressive realized volatility (HAR-RV) model. Our results show that the EMVID index improves the forecast accuracy of realized variance of REITs at short-, medium-, and long-run horizons in a statistically significant manner, with the result being robust to the inclusion of additional controls (leverage, realized jumps, skewness, and kurtosis) capturing extreme market movements, and also carries over to 10 sub-sectors of the US REITs market. Our results have important portfolio implications for investors during the current period of unprecedented levels of uncertainty resulting from the outbreak of COVID-19.</p>","PeriodicalId":46664,"journal":{"name":"International Review of Finance","volume":"22 3","pages":"540-550"},"PeriodicalIF":2.6000,"publicationDate":"2021-07-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1111/irfi.12357","citationCount":"5","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Review of Finance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/irfi.12357","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 5

Abstract

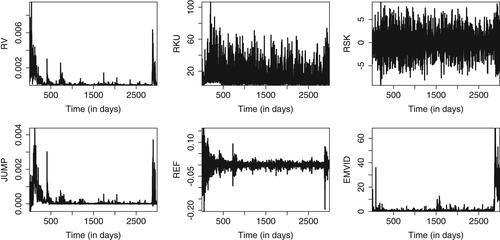

We examine the forecasting power of a daily newspaper-based index of uncertainty associated with infectious diseases (EMVID) for real estate investment trusts (REITs) realized market variance of the United States (US) via the heterogeneous autoregressive realized volatility (HAR-RV) model. Our results show that the EMVID index improves the forecast accuracy of realized variance of REITs at short-, medium-, and long-run horizons in a statistically significant manner, with the result being robust to the inclusion of additional controls (leverage, realized jumps, skewness, and kurtosis) capturing extreme market movements, and also carries over to 10 sub-sectors of the US REITs market. Our results have important portfolio implications for investors during the current period of unprecedented levels of uncertainty resulting from the outbreak of COVID-19.

期刊介绍:

The International Review of Finance (IRF) publishes high-quality research on all aspects of financial economics, including traditional areas such as asset pricing, corporate finance, market microstructure, financial intermediation and regulation, financial econometrics, financial engineering and risk management, as well as new areas such as markets and institutions of emerging market economies, especially those in the Asia-Pacific region. In addition, the Letters Section in IRF is a premium outlet of letter-length research in all fields of finance. The length of the articles in the Letters Section is limited to a maximum of eight journal pages.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们