{"title":"Impact of Depreciation Information on Capital Budgeting among Local Governments: A Survey Experiment","authors":"Makoto Kuroki","doi":"10.1111/auar.12355","DOIUrl":null,"url":null,"abstract":"<p>This study investigates the impact of depreciation practices on the internal decision making of local government (LG) budget officers. Prior studies focus on depreciation practices that influence decision making and policy formulation through financial performance indicators. However, such practices are also expected to affect capital asset management. Specifically, the presence of depreciation information makes it possible for budget officers to account for the burden of current and future generations such as depreciation costs and debt interests when budgeting. Thus, this study tests the impact of depreciation information on capital budgeting by conducting a survey experiment with all 1788 LGs in Japan. A questionnaire was sent to LG budget officers with two patterns of experimental groups: decision making for capital budgeting (a) without depreciation information and (b) with depreciation information. The experimental results show that budget officers’ capital budget decisions are influenced by the presence of depreciation information. This study contributes to accounting and public sector research and practice by showing the impact of depreciation information on the decision making of LG budget officers for capital budgeting.</p>","PeriodicalId":51552,"journal":{"name":"Australian Accounting Review","volume":"32 2","pages":"201-213"},"PeriodicalIF":3.3000,"publicationDate":"2021-10-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/auar.12355","citationCount":"2","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Accounting Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/auar.12355","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 2

Abstract

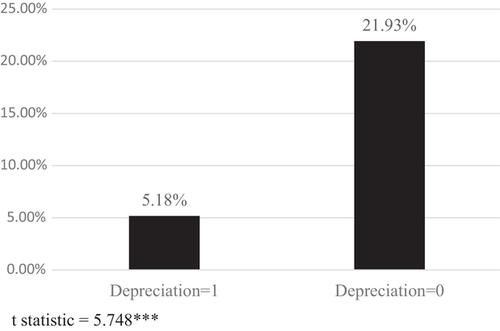

This study investigates the impact of depreciation practices on the internal decision making of local government (LG) budget officers. Prior studies focus on depreciation practices that influence decision making and policy formulation through financial performance indicators. However, such practices are also expected to affect capital asset management. Specifically, the presence of depreciation information makes it possible for budget officers to account for the burden of current and future generations such as depreciation costs and debt interests when budgeting. Thus, this study tests the impact of depreciation information on capital budgeting by conducting a survey experiment with all 1788 LGs in Japan. A questionnaire was sent to LG budget officers with two patterns of experimental groups: decision making for capital budgeting (a) without depreciation information and (b) with depreciation information. The experimental results show that budget officers’ capital budget decisions are influenced by the presence of depreciation information. This study contributes to accounting and public sector research and practice by showing the impact of depreciation information on the decision making of LG budget officers for capital budgeting.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们