{"title":"Asymptotics for function derivatives estimators based on stationary and ergodic discrete time processes","authors":"Salim Bouzebda, Mohamed Chaouch, Sultana Didi Biha","doi":"10.1007/s10463-021-00814-2","DOIUrl":null,"url":null,"abstract":"<div><p>The main purpose of the present work is to investigate kernel-type estimate of a class of function derivatives including parameters such as the density, the conditional cumulative distribution function and the regression function. The uniform strong convergence rate is obtained for the proposed estimates and the central limit theorem is established under mild conditions. Moreover, we study the asymptotic mean integrated square error of kernel derivative estimator which plays a fundamental role in the characterization of the optimal bandwidth. The obtained results in this paper are established under a general setting of discrete time stationary and ergodic processes. A simulation study is performed to assess the performance of the estimate of the derivatives of the density function as well as the regression function under the framework of a discretized stochastic processes. An application to financial asset prices is also considered for illustration.</p></div>","PeriodicalId":55511,"journal":{"name":"Annals of the Institute of Statistical Mathematics","volume":"74 4","pages":"737 - 771"},"PeriodicalIF":0.6000,"publicationDate":"2022-01-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"2","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of the Institute of Statistical Mathematics","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1007/s10463-021-00814-2","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

引用次数: 2

Abstract

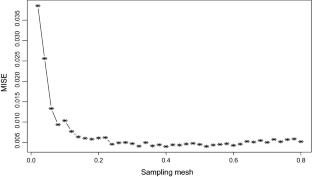

The main purpose of the present work is to investigate kernel-type estimate of a class of function derivatives including parameters such as the density, the conditional cumulative distribution function and the regression function. The uniform strong convergence rate is obtained for the proposed estimates and the central limit theorem is established under mild conditions. Moreover, we study the asymptotic mean integrated square error of kernel derivative estimator which plays a fundamental role in the characterization of the optimal bandwidth. The obtained results in this paper are established under a general setting of discrete time stationary and ergodic processes. A simulation study is performed to assess the performance of the estimate of the derivatives of the density function as well as the regression function under the framework of a discretized stochastic processes. An application to financial asset prices is also considered for illustration.

期刊介绍:

Annals of the Institute of Statistical Mathematics (AISM) aims to provide a forum for open communication among statisticians, and to contribute to the advancement of statistics as a science to enable humans to handle information in order to cope with uncertainties. It publishes high-quality papers that shed new light on the theoretical, computational and/or methodological aspects of statistical science. Emphasis is placed on (a) development of new methodologies motivated by real data, (b) development of unifying theories, and (c) analysis and improvement of existing methodologies and theories.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们