{"title":"Bet on innovation, not ESG metrics, to lead the net zero transition","authors":"Bartley J. Madden","doi":"10.1111/jacf.12554","DOIUrl":null,"url":null,"abstract":"<p>In 1987, the United Nations defined sustainable development as meeting the needs of present generations without compromising the needs of future generations. Today, the top priority for sustainability is the transition to Net Zero—that is, net zero greenhouse gas (GHG) emissions. Carbon dioxide, a GHG, is a major contributor to global warming.</p><p>In the pages that follow, I provide three different perspectives on how companies are most likely to help get us to Net Zero. The first is the widespread, conventional perspective that Environmental, Social, and Governance (ESG) metrics will lead the way to a successful transition to Net Zero. The second uses systems thinking to better describe the complexity of navigating a path to Net Zero and highlights the critical role of innovation. The third promotes systems thinking for corporate boards with the aim of improving decision-making and accelerating innovation and adaptation in a fast-changing Net Zero world.</p><p>Facing pressure from institutional asset managers, companies today must begin navigating a path to Net Zero.1 As metrics keyed to the “E” of ESG and specifically related to GHG emissions proliferate, investors are increasingly using ESG scorecards as part of their decision-making. At the beginning of 2022, the capital devoted to exchange-traded, ESG-focused funds exceeded $2.7 trillion. Moreover, regulatory bodies continue to make this kind of data mandatory in corporate reports. As a consequence, managements and boards of directors are motivated to take actions that can make their companies look good at least in terms of ESG metrics.</p><p>But the objective of such companies ought, of course, to be to reduce their GHG emissions. The current default reporting methodology is the GHG Protocol, in accord with which Scope 1 emissions are those directly produced by a firm's operations—for example, from driving owned and leased vehicles. Scope 2 missions are those produced by facilities that generate electricity bought and consumed by the company. Scope 3 emissions originate from upstream operations in a company's supply chain and from downstream use by both its “wholesale” and end-use consumers. The GHG Protocol methodology has been criticized as lacking accuracy and verifiability (primarily in terms of Scope 3), in significant part for requiring that the same emissions reported multiple times by different companies.</p><p>To address this and other limitations of the Protocol, Robert Kaplan and Karthik Ramanna have proposed an innovative solution that recognizes the integrated nature of pollution activities across the economy. A company's existing accounting system and cost-accounting infrastructure would record the GHG units emitted during operations as an <i>E-liability</i>.2 All along the supply chain, companies would transfer the E-liability associated with goods delivered and record their end-of-period E-liability. This method eliminates multiple counting of emissions in the conceptually flawed Stage 3 method while also limiting opportunities for greenwashing gamesmanship.</p><p>The conventional perspective with its emphasis on ESG metrics represents linear cause-and-effect thinking. That is, a logically tight path is assumed to exist from implementing ESG metrics to “incentivizing” companies to take actions to improve their ESG scores, eventually leading to a successful Net Zero transition. Interestingly, those who embrace this perspective invariably do appreciate the complexity and messiness of the climate change problem reflected in the interrelatedness that brings together political, economic, ecological, and social issues with multiple causes generating multiple effects often separated in time and space.3</p><p>Linear cause-and-effect thinking frequently leads to the promotion of overly simplistic means to achieve goals. Why? Mainly because written and verbal communications are perceived as persuasive when key points are presented in a logically tight <i>linear</i> manner. Today's leaders frequently prefer confident conclusions to the tentativeness and epistemological humility exhibited by systems thinkers. Why not put systems thinking front and center since it facilitates the use of alternative ways of seeing the world that can overcome more narrow perceptual processes often driven by rigid and ossified assumptions?4 To embrace systems thinking is to continually question key assumptions, to organize feedback (especially from experimentation), and to appreciate, and actively seek, diverse points of view; along with a <i>sustained curiosity</i> about mapping the intricacies of interrelationships in a complex system.5 Such alternative perspectives can reveal faulty assumptions and lead to expedited learning that helps identify key constraints and leverage points in order to improve system performance. Easier said than done.</p><p>The linear cause-and-effect choice appears sensible to many because promoting a pure systems-thinking approach means a journey full of surprises and the need to adapt and deal with unforeseen problems, while making mistakes along the way as a necessary part of learning about system complexity. But some may perceive this as a journey to climb a mountain that has no top—that is, an integrated, holistic understanding of the climate system with all the interrelatedness with other systems. Hence, the preference to minimize future surprises and to take the easier route laid out by ESG metrics.</p><p>The interrelatedness of GHG emissions with geopolitical risk became readily apparent with Russia's invasion of Ukraine beginning in February 2022, coupled with the dependency of many European countries on imports of Russian oil, gas, and coal. European policy makers concerned with their energy security began reassessing their increased fossil fuel usage from non-Russian sources, including liquefied natural gas from the U.S. A related geopolitical risk is China's assertion of control over Taiwan. Under this scenario, those countries that actively oppose China could find their supply of Chinese rare earth minerals—those required for electrical vehicle batteries—suffering a long-term disruption.</p><p>Take lithium, which is a critical component of batteries. One of the world's largest deposits of lithium has been discovered in Nevada's Thacker Pass. A mining permit was issued in February 2022 after a lengthy battle with U.S. environmentalists who, notwithstanding their support for green energy are adamantly opposed to such mining in the U.S. They have filed additional lawsuits to stop this mining operation. Keep in mind that batteries for electric vehicles contain a witches’ brew of metals—lithium, nickel, cobalt, copper, and rare earth metals such as neodymium and dysprosium. The current mining process results in substantial environmental degradation, which will only get worse thanks to accelerating demand. Nevertheless, U.S. mining of these metals—which means replacing a portion mined outside the U.S.—would entail highly regulated processes that, from a global system perspective, would yield a net environmental improvement and reduce the risk of supply disruptions for U.S. electric vehicle manufacturers.</p><p>Solar panels, wind turbines, battery-powered electric vehicles, and the retirement of coal-burning power plants are the face of decarbonization for the general public. The problem, however, is that such initiatives fall well short of what will be needed to achieve Net Zero. Complexities abound. Solar and wind are intermittent sources of electricity, needing to be transported over an old and inefficient electric grid. Plus their intermittency requires carbon dioxide-emitting natural gas powerplants (assuming declining nuclear and retired coal plants) to even out supply and demand. In addition, intermittent renewables do not address hard-to-electrify sectors like steel, cement, and air travel.</p><p>Complex systems are built on the premise of a world of great uncertainty, in which some possibly as yet unknown variables are almost <i>expected</i> to emerge (“we know something important is going to change, we just don't know what it will be”), thereby upsetting the plans of those who extrapolate the future based on what is known today.13 When operating in such a world, management and boards should give top priority to monitoring innovation developments and ensuring they have adaptable plans for the Net Zero journey.14</p><p>Let's take a quick look at some of the Net Zero activities of three large established companies that have largely gone under the radar, unheralded if not actually scorned by ESG rating agencies. One is Honeywell, which currently receives an “F” overall grade for GHG disclosures/targets/reductions by As You Sow.15 Another is Weyerhaeuser, which has become a timber REIT and not customarily viewed as a source of significant innovation. The third is Occidental Petroleum, a large oil producer certainly not revered by environmental activists.</p><p>Honeywell's businesses focus on aerospace, building technologies, performance materials and technologies, and safety and productivity solutions. Given the firm's deep knowledge of customer needs coupled to its innovation skill, you might expect that management's decision to commit 60% of its R&D budget to customer-ESG improvements would yield significant results. You would be right.</p><p>Here are a few highlights of important Honeywell innovations that advance Net Zero. The use of Honeywell's Solstice line of low global warming refrigerants, propellants, and solvents has resulted to date in the equivalent of removing 42 million cars from the road for 1 year. The company is also developing a green jet fuel that would replace petroleum jet fuel. Honeywell's green diesel fuel reduces GHG emissions by 80%, its unique flow battery technology is on a path to enable large-scale renewable energy storage, and its core business of control and automation of building and factory operations continues to enable its customers to attain higher-sustainability performance.</p><p>For 120 years, Weyerhaeuser has been growing, harvesting, and regrowing forests on a continuous cycle. Weyerhaeuser has historically been a sustainability leader, and is carbon negative by virtue of trees’ absorption of carbon dioxide. The company meets 70% of its energy needs using renewable biomass. Weyerhaeuser is also well positioned to promote and seize a big opportunity for engineered “mass timber”—glued- together wooden pieces—to replace concrete and steel in new building construction. Along with lower construction costs and aesthetically pleasing buildings, GHG emissions are substantially reduced versus the status quo. Weyerhaeuser has also announced plans to lease portions of its 11 million acres of U.S. timberland for wind and solar production and to participate in the carbon offsets market.</p><p>The firm has a unique opportunity for high-ROI projects that use selected land parcels with the right geological formation to store carbon dioxide. As one example, Oxy Low Carbon Ventures, a subsidiary of Occidental Petroleum, will use Carbon Engineering's Direct Air Capture (DAC) technology on Weyerhaeuser land to capture and permanently sequester carbon dioxide from the atmosphere.16 This planned one-million-ton annual capacity plant will be the world's biggest DAC facility, and aerospace leader Airbus has signed up for 400,000 tons of carbon-removed credits.</p><p>From a corporate finance valuation perspective, Occidental Petroleum's challenge is also an opportunity and one that all large oil and gas companies now face. If we view the firm's current market value as the sum of the net present value of existing assets and future investments, then one can “back out” the implied value of future investments by subtracting the estimated value of its current, established operations from today's known total market value of equity plus debt. But when one does this calculation, whether for Oxy or most of the majors, one finds a value for future investments that is substantially negative, indicating that investors are forecasting ROIs on future investments to be well below the cost of capital.</p><p>The flip side of this problem is the opportunity for the majors to gain substantial market value by giving investors reasons to forecast ROIs at least equal to the cost of capital on future capital expenditures. The key here is to be making new investments that can meet the cost-of-capital criterion at scale—new, big market opportunities. These opportunities exist in hydrogen, SMRs, carbon capture and storage, hard-to-decarbonize sectors, and new ways to use carbon dioxide and so avoid releasing it in the atmosphere. Occidental Petroleum is investing in most of these areas while aiming to take advantage of its core competency in carbon dioxide management. The above-mentioned DAC plant is one example.</p><p>To sum up, the rate of progress in getting to Net Zero critically depends upon innovation at the firm level; specifically, how management adapts and leverages existing capabilities to seize Net-Zero-related opportunities for innovation. Hence, a deeper understanding of how companies create value in today's economy can provide a lens to better see Net Zero progress at ground level, as opposed to high-level goals for GHG emissions and related ESG metrics. That lens has two components. First is greater appreciation of the New Economy that has spawned ecosystems that increasingly offer a path to shared value. Second are insights about long-run corporate performance in relation to the all-important cost-of-capital criterion that come from viewing companies with the life-cycle framework I say more about below.</p><p>The success of the Net Zero transition will depend heavily on boards’ effectiveness in motivating, compensating, and monitoring management in ways consistent with long-term value creation, including sustaining a pro-innovation culture with potential to gain competitive advantage. There is little doubt that companies will develop new ways of reducing emissions from their internal processes. But one should expect such best practices to be widely implemented by industry competitors. Hence, no competitive advantage here. As suggested earlier, the big promise is almost certain to come from new, and as yet largely unrecognized, opportunities to earn ROIs well in excess of the cost of capital on large-scale capital outlays—opportunities that will be discovered in their products and services that are uniquely suited to meet customers’ needs in the Net Zero world and are difficult for competitors to duplicate at the scale of the innovators. This is the story we have been telling about companies like Honeywell and Cummins.25</p><p>Compensation plans in shareholder proxy documents often contain <i>short-term</i> (3 years or less) plan horizons with no references to corporate returns or the cost of capital. But to repeat my earlier message, companies that consistently fail to earn the cost of capital will not survive as independent companies—and thus there will be no <i>long term</i>. Compensation plans should accordingly be designed as part of a company-wide financial management system focused on creating long-term value, not as an isolated document that compensation consultants craft with simplistic quartile rankings and short-term metrics and indicators.26 Boards would benefit from having directors with systems thinking expertise. The more attention to systems thinking, the more apparent becomes the inadequacy of the information provided to boards, which is typically orchestrated by CEOs (especially when the CEO also serves as the board's chairperson).</p><p>Consider an environment where the board is fully engaged with a management team that provides the information that the board believes is needed. What might that look like, beginning with resource allocation decisions for the firm's business units? In many if not most cases, the best information choice for evaluating ongoing business-unit investments is a life-cycle track record that displays the business unit's historical performance (similar to Cummins’ track record shown in Figure 2) set alongside a forecast of future life-cycle performance. The forecast's plausibility could be judged by comparison to the business unit's historical track record and to track records for competitors. Note that a life-cycle track record can be condensed into data displays that focus on economic value added (EVA).28 One particularly valuable use of life-cycle thinking is its ability to provide milestones or guideposts, as previously discussed, as to top priorities depending upon a company's (or business unit's) life-cycle stage.</p><p>With systems thinking, the interrelatedness of the compensation plan with strategic considerations also becomes more apparent. On the one hand, the compensation plan focuses on <i>what</i> is measured as to financial performance and that should work to encourage long-term value creation. But at the same time, <i>how</i> such results are achieved is also likely to matter. This link to strategy and the means of value creation ties back to a company's degree of success in sustaining a knowledge-building culture that facilitates the training, support, and motivation of employees at all levels to be problem solvers who excel in building teamwork and collaboration.29 An integral part of an innovative, well-functioning culture is the development and promotion of leaders with the right skills for the job. The higher one goes in the management ranks, the more important becomes their systems thinking skill.</p><p>The culture so described is likely to prove the bedrock of an innovation process that, when successful, shows up as favorable fade in life-cycle track records. And to promote and reinforce such a culture, the compensation plan should be long-term oriented with two well-designed and complementary components: financial performance and culture performance.</p><p>Systems thinking encourages the questioning of assumptions and soliciting of diverse views that are likely to shed light on promising solutions to specific problems or even better ways of organizing the firm and how it is managed. When the CEO and board are fully engaged with systems thinking, major changes can be expedited because of a shared goal to improve the performance of the overall system (the entire firm itself) and greater willingness to disrupt business as usual. Management and boards that cling to a business-as-usual mindset coupled with greenwashing communications about emission reductions will surely prove laggards in the new Net Zero world.</p><p>A board's fiduciary duty with respect to its company's long-term survival and prosperity requires that directors periodically evaluate their firm's past and projected future long-term financial performance. Such a viability test should include, as noted, <i>a comparison of returns-on-capital versus the cost of capital</i> and address not only a status-quo scenario of no carbon tax, but also multiple scenarios addressing a range of plausible future carbon taxes (per ton of carbon dioxide gas equivalent emitted). Such a test may well lead to large-scale changes in strategy and/or restructuring of business units.</p><p>Too much attention to looking good on the basis of trendy ESG metrics can easily turn out to be at cross-purposes with a long-term planning horizon keyed to innovation. A sizable portion of a company's major innovations may not move the needle much in terms of ESG metrics but may score high in the eyes of customers as to value creation (and quite possibly improve their customers’ ESG performance). Recent research shows a tendency during quarterly earnings conference calls for those managements who have reported weaker-than-expected profits to talk less about financial results and more about their ESG progress.31 Keep in mind that innovation is the key to <i>sustainable progress</i> that jointly delivers on financial performance and taking care of future generations through environmental improvements.</p><p>Expect the most significant innovations that advance the Net Zero transition to be delivered by managements that question assumptions, experiment, expand their firm's knowledge base, and continually adapt their business model to a fast-changing world—resulting in high ROIs achieved on new investments.</p>","PeriodicalId":46789,"journal":{"name":"Journal of Applied Corporate Finance","volume":"35 2","pages":"35-44"},"PeriodicalIF":1.4000,"publicationDate":"2023-06-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12554","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Corporate Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12554","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

In 1987, the United Nations defined sustainable development as meeting the needs of present generations without compromising the needs of future generations. Today, the top priority for sustainability is the transition to Net Zero—that is, net zero greenhouse gas (GHG) emissions. Carbon dioxide, a GHG, is a major contributor to global warming.

In the pages that follow, I provide three different perspectives on how companies are most likely to help get us to Net Zero. The first is the widespread, conventional perspective that Environmental, Social, and Governance (ESG) metrics will lead the way to a successful transition to Net Zero. The second uses systems thinking to better describe the complexity of navigating a path to Net Zero and highlights the critical role of innovation. The third promotes systems thinking for corporate boards with the aim of improving decision-making and accelerating innovation and adaptation in a fast-changing Net Zero world.

Facing pressure from institutional asset managers, companies today must begin navigating a path to Net Zero.1 As metrics keyed to the “E” of ESG and specifically related to GHG emissions proliferate, investors are increasingly using ESG scorecards as part of their decision-making. At the beginning of 2022, the capital devoted to exchange-traded, ESG-focused funds exceeded $2.7 trillion. Moreover, regulatory bodies continue to make this kind of data mandatory in corporate reports. As a consequence, managements and boards of directors are motivated to take actions that can make their companies look good at least in terms of ESG metrics.

But the objective of such companies ought, of course, to be to reduce their GHG emissions. The current default reporting methodology is the GHG Protocol, in accord with which Scope 1 emissions are those directly produced by a firm's operations—for example, from driving owned and leased vehicles. Scope 2 missions are those produced by facilities that generate electricity bought and consumed by the company. Scope 3 emissions originate from upstream operations in a company's supply chain and from downstream use by both its “wholesale” and end-use consumers. The GHG Protocol methodology has been criticized as lacking accuracy and verifiability (primarily in terms of Scope 3), in significant part for requiring that the same emissions reported multiple times by different companies.

To address this and other limitations of the Protocol, Robert Kaplan and Karthik Ramanna have proposed an innovative solution that recognizes the integrated nature of pollution activities across the economy. A company's existing accounting system and cost-accounting infrastructure would record the GHG units emitted during operations as an E-liability.2 All along the supply chain, companies would transfer the E-liability associated with goods delivered and record their end-of-period E-liability. This method eliminates multiple counting of emissions in the conceptually flawed Stage 3 method while also limiting opportunities for greenwashing gamesmanship.

The conventional perspective with its emphasis on ESG metrics represents linear cause-and-effect thinking. That is, a logically tight path is assumed to exist from implementing ESG metrics to “incentivizing” companies to take actions to improve their ESG scores, eventually leading to a successful Net Zero transition. Interestingly, those who embrace this perspective invariably do appreciate the complexity and messiness of the climate change problem reflected in the interrelatedness that brings together political, economic, ecological, and social issues with multiple causes generating multiple effects often separated in time and space.3

Linear cause-and-effect thinking frequently leads to the promotion of overly simplistic means to achieve goals. Why? Mainly because written and verbal communications are perceived as persuasive when key points are presented in a logically tight linear manner. Today's leaders frequently prefer confident conclusions to the tentativeness and epistemological humility exhibited by systems thinkers. Why not put systems thinking front and center since it facilitates the use of alternative ways of seeing the world that can overcome more narrow perceptual processes often driven by rigid and ossified assumptions?4 To embrace systems thinking is to continually question key assumptions, to organize feedback (especially from experimentation), and to appreciate, and actively seek, diverse points of view; along with a sustained curiosity about mapping the intricacies of interrelationships in a complex system.5 Such alternative perspectives can reveal faulty assumptions and lead to expedited learning that helps identify key constraints and leverage points in order to improve system performance. Easier said than done.

The linear cause-and-effect choice appears sensible to many because promoting a pure systems-thinking approach means a journey full of surprises and the need to adapt and deal with unforeseen problems, while making mistakes along the way as a necessary part of learning about system complexity. But some may perceive this as a journey to climb a mountain that has no top—that is, an integrated, holistic understanding of the climate system with all the interrelatedness with other systems. Hence, the preference to minimize future surprises and to take the easier route laid out by ESG metrics.

The interrelatedness of GHG emissions with geopolitical risk became readily apparent with Russia's invasion of Ukraine beginning in February 2022, coupled with the dependency of many European countries on imports of Russian oil, gas, and coal. European policy makers concerned with their energy security began reassessing their increased fossil fuel usage from non-Russian sources, including liquefied natural gas from the U.S. A related geopolitical risk is China's assertion of control over Taiwan. Under this scenario, those countries that actively oppose China could find their supply of Chinese rare earth minerals—those required for electrical vehicle batteries—suffering a long-term disruption.

Take lithium, which is a critical component of batteries. One of the world's largest deposits of lithium has been discovered in Nevada's Thacker Pass. A mining permit was issued in February 2022 after a lengthy battle with U.S. environmentalists who, notwithstanding their support for green energy are adamantly opposed to such mining in the U.S. They have filed additional lawsuits to stop this mining operation. Keep in mind that batteries for electric vehicles contain a witches’ brew of metals—lithium, nickel, cobalt, copper, and rare earth metals such as neodymium and dysprosium. The current mining process results in substantial environmental degradation, which will only get worse thanks to accelerating demand. Nevertheless, U.S. mining of these metals—which means replacing a portion mined outside the U.S.—would entail highly regulated processes that, from a global system perspective, would yield a net environmental improvement and reduce the risk of supply disruptions for U.S. electric vehicle manufacturers.

Solar panels, wind turbines, battery-powered electric vehicles, and the retirement of coal-burning power plants are the face of decarbonization for the general public. The problem, however, is that such initiatives fall well short of what will be needed to achieve Net Zero. Complexities abound. Solar and wind are intermittent sources of electricity, needing to be transported over an old and inefficient electric grid. Plus their intermittency requires carbon dioxide-emitting natural gas powerplants (assuming declining nuclear and retired coal plants) to even out supply and demand. In addition, intermittent renewables do not address hard-to-electrify sectors like steel, cement, and air travel.

Complex systems are built on the premise of a world of great uncertainty, in which some possibly as yet unknown variables are almost expected to emerge (“we know something important is going to change, we just don't know what it will be”), thereby upsetting the plans of those who extrapolate the future based on what is known today.13 When operating in such a world, management and boards should give top priority to monitoring innovation developments and ensuring they have adaptable plans for the Net Zero journey.14

Let's take a quick look at some of the Net Zero activities of three large established companies that have largely gone under the radar, unheralded if not actually scorned by ESG rating agencies. One is Honeywell, which currently receives an “F” overall grade for GHG disclosures/targets/reductions by As You Sow.15 Another is Weyerhaeuser, which has become a timber REIT and not customarily viewed as a source of significant innovation. The third is Occidental Petroleum, a large oil producer certainly not revered by environmental activists.

Honeywell's businesses focus on aerospace, building technologies, performance materials and technologies, and safety and productivity solutions. Given the firm's deep knowledge of customer needs coupled to its innovation skill, you might expect that management's decision to commit 60% of its R&D budget to customer-ESG improvements would yield significant results. You would be right.

Here are a few highlights of important Honeywell innovations that advance Net Zero. The use of Honeywell's Solstice line of low global warming refrigerants, propellants, and solvents has resulted to date in the equivalent of removing 42 million cars from the road for 1 year. The company is also developing a green jet fuel that would replace petroleum jet fuel. Honeywell's green diesel fuel reduces GHG emissions by 80%, its unique flow battery technology is on a path to enable large-scale renewable energy storage, and its core business of control and automation of building and factory operations continues to enable its customers to attain higher-sustainability performance.

For 120 years, Weyerhaeuser has been growing, harvesting, and regrowing forests on a continuous cycle. Weyerhaeuser has historically been a sustainability leader, and is carbon negative by virtue of trees’ absorption of carbon dioxide. The company meets 70% of its energy needs using renewable biomass. Weyerhaeuser is also well positioned to promote and seize a big opportunity for engineered “mass timber”—glued- together wooden pieces—to replace concrete and steel in new building construction. Along with lower construction costs and aesthetically pleasing buildings, GHG emissions are substantially reduced versus the status quo. Weyerhaeuser has also announced plans to lease portions of its 11 million acres of U.S. timberland for wind and solar production and to participate in the carbon offsets market.

The firm has a unique opportunity for high-ROI projects that use selected land parcels with the right geological formation to store carbon dioxide. As one example, Oxy Low Carbon Ventures, a subsidiary of Occidental Petroleum, will use Carbon Engineering's Direct Air Capture (DAC) technology on Weyerhaeuser land to capture and permanently sequester carbon dioxide from the atmosphere.16 This planned one-million-ton annual capacity plant will be the world's biggest DAC facility, and aerospace leader Airbus has signed up for 400,000 tons of carbon-removed credits.

From a corporate finance valuation perspective, Occidental Petroleum's challenge is also an opportunity and one that all large oil and gas companies now face. If we view the firm's current market value as the sum of the net present value of existing assets and future investments, then one can “back out” the implied value of future investments by subtracting the estimated value of its current, established operations from today's known total market value of equity plus debt. But when one does this calculation, whether for Oxy or most of the majors, one finds a value for future investments that is substantially negative, indicating that investors are forecasting ROIs on future investments to be well below the cost of capital.

The flip side of this problem is the opportunity for the majors to gain substantial market value by giving investors reasons to forecast ROIs at least equal to the cost of capital on future capital expenditures. The key here is to be making new investments that can meet the cost-of-capital criterion at scale—new, big market opportunities. These opportunities exist in hydrogen, SMRs, carbon capture and storage, hard-to-decarbonize sectors, and new ways to use carbon dioxide and so avoid releasing it in the atmosphere. Occidental Petroleum is investing in most of these areas while aiming to take advantage of its core competency in carbon dioxide management. The above-mentioned DAC plant is one example.

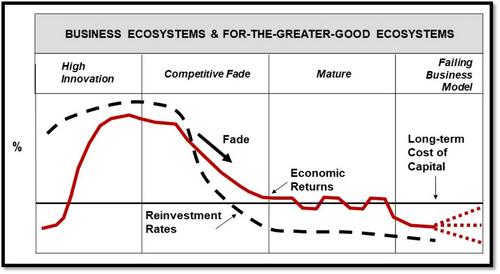

To sum up, the rate of progress in getting to Net Zero critically depends upon innovation at the firm level; specifically, how management adapts and leverages existing capabilities to seize Net-Zero-related opportunities for innovation. Hence, a deeper understanding of how companies create value in today's economy can provide a lens to better see Net Zero progress at ground level, as opposed to high-level goals for GHG emissions and related ESG metrics. That lens has two components. First is greater appreciation of the New Economy that has spawned ecosystems that increasingly offer a path to shared value. Second are insights about long-run corporate performance in relation to the all-important cost-of-capital criterion that come from viewing companies with the life-cycle framework I say more about below.

The success of the Net Zero transition will depend heavily on boards’ effectiveness in motivating, compensating, and monitoring management in ways consistent with long-term value creation, including sustaining a pro-innovation culture with potential to gain competitive advantage. There is little doubt that companies will develop new ways of reducing emissions from their internal processes. But one should expect such best practices to be widely implemented by industry competitors. Hence, no competitive advantage here. As suggested earlier, the big promise is almost certain to come from new, and as yet largely unrecognized, opportunities to earn ROIs well in excess of the cost of capital on large-scale capital outlays—opportunities that will be discovered in their products and services that are uniquely suited to meet customers’ needs in the Net Zero world and are difficult for competitors to duplicate at the scale of the innovators. This is the story we have been telling about companies like Honeywell and Cummins.25

Compensation plans in shareholder proxy documents often contain short-term (3 years or less) plan horizons with no references to corporate returns or the cost of capital. But to repeat my earlier message, companies that consistently fail to earn the cost of capital will not survive as independent companies—and thus there will be no long term. Compensation plans should accordingly be designed as part of a company-wide financial management system focused on creating long-term value, not as an isolated document that compensation consultants craft with simplistic quartile rankings and short-term metrics and indicators.26 Boards would benefit from having directors with systems thinking expertise. The more attention to systems thinking, the more apparent becomes the inadequacy of the information provided to boards, which is typically orchestrated by CEOs (especially when the CEO also serves as the board's chairperson).

Consider an environment where the board is fully engaged with a management team that provides the information that the board believes is needed. What might that look like, beginning with resource allocation decisions for the firm's business units? In many if not most cases, the best information choice for evaluating ongoing business-unit investments is a life-cycle track record that displays the business unit's historical performance (similar to Cummins’ track record shown in Figure 2) set alongside a forecast of future life-cycle performance. The forecast's plausibility could be judged by comparison to the business unit's historical track record and to track records for competitors. Note that a life-cycle track record can be condensed into data displays that focus on economic value added (EVA).28 One particularly valuable use of life-cycle thinking is its ability to provide milestones or guideposts, as previously discussed, as to top priorities depending upon a company's (or business unit's) life-cycle stage.

With systems thinking, the interrelatedness of the compensation plan with strategic considerations also becomes more apparent. On the one hand, the compensation plan focuses on what is measured as to financial performance and that should work to encourage long-term value creation. But at the same time, how such results are achieved is also likely to matter. This link to strategy and the means of value creation ties back to a company's degree of success in sustaining a knowledge-building culture that facilitates the training, support, and motivation of employees at all levels to be problem solvers who excel in building teamwork and collaboration.29 An integral part of an innovative, well-functioning culture is the development and promotion of leaders with the right skills for the job. The higher one goes in the management ranks, the more important becomes their systems thinking skill.

The culture so described is likely to prove the bedrock of an innovation process that, when successful, shows up as favorable fade in life-cycle track records. And to promote and reinforce such a culture, the compensation plan should be long-term oriented with two well-designed and complementary components: financial performance and culture performance.

Systems thinking encourages the questioning of assumptions and soliciting of diverse views that are likely to shed light on promising solutions to specific problems or even better ways of organizing the firm and how it is managed. When the CEO and board are fully engaged with systems thinking, major changes can be expedited because of a shared goal to improve the performance of the overall system (the entire firm itself) and greater willingness to disrupt business as usual. Management and boards that cling to a business-as-usual mindset coupled with greenwashing communications about emission reductions will surely prove laggards in the new Net Zero world.

A board's fiduciary duty with respect to its company's long-term survival and prosperity requires that directors periodically evaluate their firm's past and projected future long-term financial performance. Such a viability test should include, as noted, a comparison of returns-on-capital versus the cost of capital and address not only a status-quo scenario of no carbon tax, but also multiple scenarios addressing a range of plausible future carbon taxes (per ton of carbon dioxide gas equivalent emitted). Such a test may well lead to large-scale changes in strategy and/or restructuring of business units.

Too much attention to looking good on the basis of trendy ESG metrics can easily turn out to be at cross-purposes with a long-term planning horizon keyed to innovation. A sizable portion of a company's major innovations may not move the needle much in terms of ESG metrics but may score high in the eyes of customers as to value creation (and quite possibly improve their customers’ ESG performance). Recent research shows a tendency during quarterly earnings conference calls for those managements who have reported weaker-than-expected profits to talk less about financial results and more about their ESG progress.31 Keep in mind that innovation is the key to sustainable progress that jointly delivers on financial performance and taking care of future generations through environmental improvements.

Expect the most significant innovations that advance the Net Zero transition to be delivered by managements that question assumptions, experiment, expand their firm's knowledge base, and continually adapt their business model to a fast-changing world—resulting in high ROIs achieved on new investments.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们