{"title":"The Credit Suisse CoCo wipeout: Facts, misperceptions, and lessons for financial regulation","authors":"Patrick Bolton, Wei Jiang, Anastasia Kartasheva","doi":"10.1111/jacf.12553","DOIUrl":null,"url":null,"abstract":"<p>The response to the global financial crisis (GFC) of 2007–2008 has famously been described as the problem of too-big-to-fail.1 In the middle of a worsening crisis, financial regulators had to recognize that bank bailouts were the only way to stabilize financial markets. One of the two priorities of regulatory reforms post-crisis was to address the too-big-to-fail problem by introducing a resolution procedure for systemically important financial institutions.2 Among financial regulators (with the notable exception of the USA), contingent convertible bonds (CoCos) were seen as a major innovation to address the too-big-to-fail problem and quickly became a popular “bail-in” instrument to facilitate the instant recapitalization of a distressed bank. The quick deleveraging that could be achieved with CoCo conversions would serve the dual roles of recapitalizing “a going-concern bank” and reducing the resolution costs for a “gone concern” bank.</p><p>During the press conference on March 19, 2023 the Swiss Financial Market Supervisory Authority (FINMA) announced that, as part of the emergency package in response to the loss of trust and the run on Credit Suisse, the contingent convertible bonds that were part of the Credit Suisse Additional Tier 1 (AT1) regulatory capital had been written off.3 The decision by FINMA took many by surprise and provoked a flood of negative market commentary, with the commonly stated view that conversion violated the priority order of claims between debt and equity. Indeed, in the final rescue deal, the shareholders of Credit Suisse retain around $3 billion of equity value, while the CoCo bond principal write-down amounted to a wipeout of $17 billion for CoCo investors. Implicitly corroborating this commentary, the European Central Bank (ECB), the Bank of England, and other regulators made public statements on the Monday following the Credit Suisse deal that they do not intend to follow the FINMA approach and that they intend to respect the usual priority order of claims in resolution.4 How can these divergent views of regulators be reconciled? Why did the Credit Suisse AT1 CoCo bondholders face losses before shareholders were wiped out? What are the lessons for the effectiveness of post-GFC too-big-to-fail reforms? This article provides clarification of these important questions.</p><p>CoCo bonds are designed to absorb losses of a distressed going-concern bank at conversion, thereby helping to capitalize the bank. Their primary purpose is to reduce the need for a capital injection by the government in times of crisis when nobody else is willing to provide additional external capital. Such public support is costly to taxpayers and exacerbates moral hazard.</p><p>CoCo bonds have two main contract features: the loss absorption mechanism and the trigger that activates that mechanism (illustrated in Graph 1).5 CoCos can absorb losses either by converting into common equity or through a principal write-down (partial or full). The trigger can be either mechanical (i.e., defined in terms of a capital ratio) or discretionary (subject to supervisory judgment).</p><p>The trigger defines the point at which the loss absorption mechanism is activated. The mechanical trigger activates the loss absorption mechanism when the capital of the CoCo-issuing bank drops below a pre-specified fraction of its risk-weighted assets. The bank's equity capital can be measured either based on book value or market value. The discretionary, or point of non-viability (PONV), trigger is activated based on the supervisor's assessment of the bank's possible insolvency. PONV triggers give regulators authority to convert, if and when they decide that the issuer has reached that state. Because the PONV is difficult to determine <i>ex ante</i>, PONV triggers introduce uncertainty about the timing and circumstances leading to the activation of the loss absorption mechanism by the regulator.</p><p>CoCo bonds typically have more than one trigger. In case of multiple triggers, the loss absorption mechanism can be activated when any trigger is breached. Under Basel III rules, all regulatory capital CoCos are required to have a discretionary PONV trigger. The activation of the discretionary trigger, which was present in all CoCos issued by Credit Suisse, was exactly what allowed FINMA to write down Credit Suisse AT1 capital instruments on March 19, 2023.</p><p>The loss absorption mechanism is the second contract feature of CoCos. Once the trigger is activated, CoCos can be either converted to equity at a pre-defined conversion rate or subject to a principal write-down. In either case, the conversion delevers the bank and/or boosts its equity capital ratio. For conversion to equity CoCos, the conversion rate can be based either on the market price of the stock at the time of conversion, or on a pre-specified price, like the stock price at the time of issuance. It is also possible to have a combination of market price and prespecified price floor, where the latter defines the floor for the conversion rate and hence protects existing equity holders from unlimited dilution. The various options for setting the conversion price lead to different exposures to dilution risk for existing equity holders, and thus create varying incentives to avoid conversion by existing equity holders. In the case of the principal write-down CoCos, the haircut can be either full or partial. However, most of the principal write-down CoCos of Credit Suisse were full write-down CoCos. The write-down CoCos potentially encourage risk taking by managers acting in the interest of shareholders.</p><p>The regulatory treatment of CoCos under Basel III and the supplementary requirements of national regulators shape the design choices of CoCo contract features of issuing banks (that can be seen in Graph 2). Under the Basel III framework, CoCos must satisfy two requirements to qualify as regulatory capital. The first requirement, which applies to both AT1 and T2 instruments, is satisfied by the PONV trigger. The second requirement is the going-concern rule, which specifies that the minimum trigger level of CET1/RWA to qualify as AT1 is 5.125%. In addition, AT1 instruments must be perpetual. Importantly, these features are not necessarily outcomes of optimal financial contracting between the issuer and its investors.</p><p>The regulatory rationale for CoCos is to improve banks’ resilience to financial shocks by strengthening their capital buffers in a crisis, while also providing investors with an investment opportunity that is distinct from debt and equity. By issuing CoCos, banks can raise capital while limiting the dilution costs of current shareholders at issuance and reduce the likelihood of becoming insolvent or requiring a government bailout. In particular, CoCos allow banks to seamlessly recapitalize during times of financial stress. The conversion or write-down of CoCos allows the bank to transfer some of the losses to CoCo investors, ensuring that the costs of bank failures are borne by investors rather than taxpayers. In addition to reducing the cost of distress, the possibility of CoCo conversion provides bankers with incentives to limit the probability of distress.</p><p>CoCos can be an attractive investment opportunity for long-term investors who understand and are able to take losses in a crisis. CoCos typically offer higher yields than traditional bonds due to their contingent nature, their low priority ranking (on par or even lower than equity investors), and the high systematic component in their risk. Because institutional mandates often block traditional fixed income investors from taking positions in conversion to equity CoCos, the market yield on the instruments may also contain a premium for sophisticated and flexible investors in terms of market segregation.</p><p>In their 2013 Primer on CoCos published by the Bank for International Settlements, colleagues Stefan Avdjiev, Anastasia Kartasheva, and Bilyana Bogdanova show that the yield-to-maturity of newly issued CoCos are on average 2.8% higher than the subordinated debt, and 4.7% higher than the senior unsecured debt, of the same bank.6 However, the popularity of CoCos could also be partly driven by the search for yield in a low interest rate environment, which have been touted by financial advisors that sometimes misrepresented the product as a relatively safe way of boosting yield.</p><p>CoCos are often perceived as similar to total loss absorbing capacity (TLAC) instruments, since they are also financial instruments designed to “bail-in” troubled systemically important banks. There are, however, key differences between the two. The primary purpose of CoCos is to delever a bank amid a crisis, by writing down debt or providing equity capital, or both. CoCos are thus designed to maintain the equity cushion of a going concern bank. TLAC, which are usually T2 capital, are additional loss absorption requirements for global systemically important banks (GSIBs) like Credit Suisse to enable a single point of entry resolution. The goal of TLAC is to ensure that the holding companies of systematically important banks have sufficient capacity to absorb losses so that their operating affiliates can continue operating without putting their liabilities at risk. By contrast, CoCo conversion could take place while the bank is still a going concern.</p><p>A 2020 article in the <i>Journal of Financial Economics</i> we wrote with Stefan Avdjiev and Bilyana Bogdanova provides the first comprehensive analysis of bank CoCo issuance.7 Out of the 731 Coco issues raising over $500 billion between 2009 and 2015, European issues took the largest share (39%), while U.S. was absent from the list. At the time of the Credit Suisse trigger event, the global AT1 CoCos market was estimated to be $254 billion.8 About 56% of these CoCos include a mechanical trigger. Though in the first years of our sample mandatory conversion CoCos were prevalent, principal write-down CoCos have become more popular over time, eventually dominating the market. Finally, slightly more than half (55%) of the CoCos up to 2015 were classified as AT1 capital, while most of the T2 CoCos tend to be issued by banks in emerging economies.</p><p>Our 2020 <i>Journal of Financial Economics</i> article also shows that the propensity to issue a CoCo is higher for larger and better capitalized banks. Presumably only relatively healthy banks, with remote conversion risk, are able to issue CoCos at a reasonable cost. Another reason is that the principal beneficiaries from a CoCo issue are senior bondholders, whereas shareholders expose themselves to dilution risk. The same JFE article shows that the CDS spreads of CoCo issuers decline upon the announcement of a CoCo issue, indicating that they generate risk-reduction benefits and lower costs of debt. While the average reduction in CDS spread was 2.7 basis points, the drop was more prominent for conversion CoCos (5.0 bps), including those with mechanical triggers (3.3 bps). Conversion CoCos with mechanical triggers are also associated with a reduction of 6.2 bps in CDS spreads. Only Additional Tier 1 instruments contributed to the reduction of CDS.</p><p>Finally, CoCo issuances have no statistically significant impact on the issuers’ stock prices, except for the case of principal write-down CoCos with high trigger levels, which involve no dilution risk for shareholders and for which stock price responses have been significantly positive on average. Such a contrast suggests a potential moral hazard on shareholders’ part to take excess risk, since the cost will be first borne by the holders of write-down CoCos. CoCos that convert to equity offer a superior design from the point of view of reducing bank fragility. In the case of Credit Suisse, all outstanding CoCos were principal write-down CoCos, and this is the reason why their investors received no equity stake in the merger with UBS. Had they issued conversion to equity CoCos, they would have received shares in the merged company.</p><p>The collapse of Silicon Valley Bank (SVB) on March 10, 2023 sent shockwaves through the financial system and quickly drew investors’ attention to the prominent weaknesses at Credit Suisse, which was impelled to seek up to CHF 50bn in liquidity support from the Swiss National Bank (SNB) on March 16, 2023. This dramatic move failed to quash speculation, or slow down deposit withdrawals, to the extent that 2 days later the SNB and FINMA announced that they had begun proceedings to organize a takeover of Credit Suisse by UBS.</p><p>The Swiss financial regulatory authorities had decided that the best way to avert another GFC was to rescue Credit Suisse through a merger with a strong financial institution, following the playbook of the Federal Reserve and US Treasury in 2008 with its rescue of Bear Stearns through a merger with JPMorgan and what has colloquially become known as the “Jamie deal” in reference to the CEO of JPMorgan.9</p><p>It is revealing to contrast these two deals, as the contexts are different and the limits on the legal authorities of regulators are different. The Federal Reserve and Treasury did not have nearly the same authority to push through a merger as the Swiss government under the Swiss emergency law. The Federal Reserve had to invoke section 13(3) of the Federal Reserve Act to claim authority to provide liquidity support “under unusual and exigent circumstances” to a broker-dealer. Beyond the authority to provide liquidity support the Federal Reserve (and US Treasury) had no means other than moral suasion to get the management of Bear Stearns and JPMorgan to agree to merge at a proposed price of $2 per Bear Stearns share. They had no authority to sidestep shareholder agreements at both Bear Stearns and JPMorgan, and they could not write down Bear Stearns liabilities outside Chapter 11 bankruptcy. The only way the deal could be structured outside bankruptcy was as a purchase-and-assumption deal whereby JPMorgan agreed to assume all Bear Stearns liabilities. However, even at the price of $2 per share, this was seen as too risky by JPMorgan management and might not receive the blessing of JPMorgan shareholders.</p><p>To overcome this hurdle the Federal Reserve agreed to back up the deal by setting up an innovative collateralized special purpose vehicle—Maiden Lane LLC. This vehicle would be financed with a junior tranche of $1 billion from JPMorgan and a $29 billion senior tranche of the Federal Reserve, and it would purchase up to $30 billion worth of troubled assets of Bear Stearns, thereby de-risking the Bear Stearns balance sheet. The Federal Reserve and Treasury also had to make concessions to Bear Stearns shareholders by eventually raising the share price to $10.10 Although this deal was successfully implemented in May 2008, and temporarily brought back some calm in financial markets, a few months later a similar merger attempt between Lehman Brothers and Barclays failed, unleashing the GFC.</p><p>The Swiss regulatory authorities were in a much better position to engineer a deal between Credit Suisse and UBS. They could bypass shareholder approval, bringing a swift resolution of uncertainty, and they did not have to put public money at risk by setting up a complex special purpose vehicle to de-risk the Credit Suisse balance sheet. All they had to do was trigger the write-down of Credit Suisse CoCos that had been designed and issued precisely for such a contingent event. And FINMA did just that, announcing that “the extraordinary government support [of Credit Suisse] will trigger a complete write-down of the nominal value of all AT1 shares of Credit Suisse in the amount of around CHF16bn, and thus an increase in core capital.”11 The principal write-down of these AT1 instruments allowed for a swift de-levering of the Credit Suisse balance sheet.</p><p>Recall that one of the main criticisms of the Bear Stearns rescue, and later interventions in the fall of 2008, has been that the complete bailout of creditors in all these rescues created a dangerous moral hazard in lending precedent.12 Viewed in this light, the write-down of the Credit Suisse AT1 bonds would not only help de-risk the Credit Suisse balance sheet but also help counter market expectations that creditors of systemically important financial institutions would always be bailed out in a crisis.</p><p>Although the write-down of Credit Suisse CoCos following the rescue of Credit Suisse was predictable, it caused consternation in financial markets and a mini crisis in the AT1 bond market. Investors in Credit Suisse AT1 bonds were surprised that their bonds had been written down even though Credit Suisse shareholders remained standing, the first such incidence in the CoCo history.</p><p>To many people, as we have noted, this seemed to be an egregious violation of absolute priority. Jérôme Legras, a managing partner and head of research at Axiom Alternative Investments, told the <i>Financial Times</i>: “The market is likely to be shocked by such a blatant inversion of the hierarchy of creditors and by the decision to sweeten an equity deal at the expense of bond holders.” There had been a precedent of a similar CoCo write-down in 2017 when Banco Popular was taken over by Santander, but in that case Banco Popular shareholders had essentially been wiped out, so that there was at least an appearance that part of the absolute priority, that is, equity being the most junior claim, had been respected.</p><p>It is not just investors who were taken off guard but also financial regulators outside Switzerland. Fearing potential contagion in the $250 billion AT1 bond market, Dominique Laboureix, chair of the EU's Single Resolution Board (SRB) quickly reacted, saying on CNBC that “In a resolution here, in the European context, we would follow the hierarchy, and we wanted to tell it very clearly to the investors, to avoid to be misunderstood: we have no choice but to respect this hierarchy.”13 On the Monday following FINMA's decision the SRB together with the EBA and ECB issued the statement: “… common equity instruments are the first ones to absorb losses, and only after their full use would Additional Tier 1 be required to be written down. This approach has been consistently applied in past cases and will continue to guide the actions of the SRB and ECB banking supervision in crisis interventions.”14</p><p>These reactions from business and regulatory leaders understandably only led to further confusion. It was only a matter of a few days before talk of lawsuits emerged. The law firm Quinn Emanuel Urquhart & Sullivan and Pallas Partners quickly announced that a lawsuit was in order, portraying the Credit Suisse rescue as “a resolution dressed up as a merger,” and commenting on the SRB and ECB responses that “you know something has gone wrong when other regulators come and politely point out that in a resolution [they] would have respected ordinary priorities”. Major investors like David Tepper, the founder and president of Appaloosa Management, a global hedge fund, further weighed in that, “if this is left to stand, how can you trust any debt security issued in Switzerland, or for that matter wider Europe, if governments can just change laws after the fact… contracts are made to be honoured.”15</p><p>But did FINMA, in fact, change the terms ex post and violate the contractual obligations of AT1 bonds? As highlighted above, most of the recent CoCos issued by Credit Suisse are principal write-down CoCos with very similar terms. For example, the SGD 750,000,000 CoCo issued in Singapore on May 29, 2019, contains the following terms: “CET1 Write-down Trigger: 7.00%, based on Credit Suisse Group AG consolidated CET1 ratio. Write-down: If a Contingency Event, or prior to a Statutory Loss Absorption Date (if any), a Viability Event occurs, the full principal amount of the notes will be mandatorily and permanently written down…. See “Terms and Conditions of the Notes—Condition 7 “Write-down”” in the Information Memorandum for the definitions of Contingency Event, Statutory Loss Absorption Date and Viability Event.”</p><p>The information memorandum further states that “A “Contingency Event” will occur if (i) Credit Suisse group's consolidated common equity tier 1 (“CET1”) divided by its consolidated risk weighted assets (“RWA”) as of any quarterly balance sheet date (or, in the case of certain of these instruments, such other date specified by FINMA) is below 7%, and (ii) FINMA has not agreed in writing prior to publication of such CET1/RWA ratio that a full conversion or write-off, as applicable, shall not occur because it is satisfied that actions, circumstances or events have had, or imminently will have, the effect of restoring the CET1/RWA ratio to a level above 7% that it deems to be adequate.”</p><p>In addition, the following provision clarifies PONV: “A ‘Viability Event’ will occur if either (i) FINMA notifies CSG that it has determined that a conversion or write-off of the relevant instrument, together with the conversion or write-off of holders' claims in respect of all other regulatory capital instruments issued by a member of the Credit Suisse group that, pursuant to their terms or by operation of law, are capable of being converted into equity or written-off at that time, is, because customary measures to improve CSG's capital adequacy are at the time inadequate or unfeasible, an essential requirement to prevent CSG from becoming insolvent, bankrupt or unable to pay a material part of its debts as they fall due, or from ceasing to carry on its business, or (ii) customary measures to improve CSG's capital adequacy being at the time inadequate or unfeasible, CSG receives an irrevocable commitment of extraordinary support from the public sector (beyond customary transactions and arrangements in the ordinary course) that has, or imminently will have, the effect of improving CSG's capital adequacy and without which, in the determination of FINMA, CSG would have become insolvent, bankrupt, unable to pay a material part of its debts as they fall due or unable to carry on its business. The occurrence of either or both of these two events is also referred to as the ‘Point of Non-Viability’ or the ’PONV’.”</p><p>The additional Credit Suisse documentation on AT1 bonds further states that: “under certain circumstances, FINMA has the power to open restructuring proceedings with respect to CSG under Swiss banking laws (see “—CSG is subject to the resolution regime under Swiss banking laws and regulations” below), and, if the Notes have not already been subject to a write-down, could convert the Notes into equity or cancel the Notes, in each case, in whole or in part. Holders should be aware that, in the case of any such conversion into equity, FINMA would follow the order of priority set out under Swiss banking laws, which means, among other things, that the Notes would have to be converted prior to the conversion of any of CSG's subordinated debt that does not qualify as regulatory capital with a contractual write-down or conversion feature. Furthermore, in the case of any such cancellation, FINMA may not be required to follow any order of priority, which means, among other things, that the Notes could be cancelled in whole or in part prior to the cancellation of any or all of CSG's equity capital.”</p><p>Granted, such provisions are not easy to follow. FINMA nevertheless exercised its authority under these contracts to trigger conversion because it deemed that Credit Suisse had reached the PONV. The Credit Suisse CoCos were not “gone concern” CoCos but “going concern” CoCos. By triggering these CoCos, FINMA implemented the AT1 contracts as they were intended to be—namely, to allow for a swift recapitalization so that Credit Suisse could be brought back to viability after reaching a point toward insolvency.</p><p>A first lawsuit has been filed by Quinn Emanuel Urquhart & Sullivan and Pallas Partners against FINMA on April 21, 2023, claiming that the AT1 bond write-down was disproportionate and that FINMA did not act in good faith.16</p><p>Following the collapse of SVB, pressures further built up on Credit Suisse with both its stock price falling and its CDS spread rising (Graph 3). Financial markets clearly reflected an increase in investors’ perceived probability of a failure and the announcement of the $50 billion borrowing facility from the SNB did not reverse these expectations. Though investors clearly entertained the possibility that there could be a default on Credit Suisse bonds, as priced in the rising CDS spreads, interestingly, the figure below suggests that investors did not anticipate a write-down of AT1 bonds until mid-March, on the eve of the takeover of Credit Suisse (Graph 4).</p><p>It is difficult to say what proportion of investors anticipated the possibility of a write-down of AT1 bonds even if shareholders were not completely wiped out. As the example above of the Credit Suisse CoCo bond issued in Singapore in 2019 shows, these bonds offered higher interest rates than plain vanilla bonds as compensation for the risk of a write-down. These higher coupon rates attracted yield-searching investors in a low interest rate environment, and their high yields were part of a major sales pitch. Reports like this one in January 2021 by a Credit Suisse portfolio manager exemplifies the sentiment of complacence “The CoCo market offers a yield of around 3.62% … even European high-yield bonds come in at around 2.88%, so we definitely still see value in subordinated financial bonds … The average European bank would need to lose almost two-thirds of its capital to breach contractual triggers.”17 Many investors in AT1 bonds may not have been aware of the risks they were exposed to, given that CoCos were pitched as highly remunerative fixed-income securities issued by very stable systemically important financial institutions. Many might also be unaware of the fact that written-down CoCos are effectively junior to equity. This is for example the view expressed by the CEO of Farro Capital: “Most Asian private banks market AT1 bonds as fixed-income securities, and people get excited with the enhanced yields on these.”18</p><p>The surprise effect of FINMA's decision can also be seen in the AT1 bond market reaction following the write-down. As the figure below shows, there was a temporary panic in this market in the days following the Credit Suisse takeover, in addition to the realization of the contingent nature of CoCos. But the market has since recovered (Graph 5).</p><p>Except for the Banco Popular CoCo write-down in 2017, there was no precedent of CoCo conversion one could learn from until the Credit Suisse event. Would CoCos work as intended? Would CoCo conversion or write-down shore up the balance sheet of a bank in distress and help stabilize financial markets? We could only speculate and our analysis in our 2020 <i>Journal of Financial Economics</i> article could look at only what investors expected at the time of issuance. Even though the Credit Suisse event gives us only one observation, many lessons can already be drawn from this event.</p><p>The first obvious lesson is that the way CoCos have been structured is creating a lot of confusion. Even some sophisticated investors appear to have been confused about the difference between going-concern and gone-concern CoCos. Investors often did not know that there was a distinction, and for those who did, it was not easy to tell the difference. The function of going concern CoCos is to allow the bank could stay viable by triggering a write-down, that is, before equity investors are wiped out. Another layer of complexity that gave rise to a lot of uncertainty in the Credit Suisse event is the existence of multiple triggers, an automatic trigger when a CET1 capital ratio is triggered and a discretionary trigger that the financial regulator could activate if it deemed that the issuer had reached the PONV.</p><p>This contractual complexity gives rise to unnecessary and costly uncertainty. It also increases the risk of misrepresentation to investors. One of the challenges with the discretionary trigger is determining what the PONV is precisely. No clear criteria have been defined, giving regulators considerable discretion ex post, and giving rise to regulatory uncertainty. The fact that the SRB and ECB felt that they had to reassure markets that they did not intend to deviate from absolute priority to calm the AT1 bond market is revealing evidence of the extent of regulatory ambiguity that is embedded in these instruments, which leads to pricing complexity. Both the automatic and discretionary triggers, and their combination, increase the difficulty in predicting accurately the probability of a CoCo being triggered. There are no off-the-shelf financial models that can be used to price these contingent securities.</p><p>Investor dismay with FINMA's decision to write down Credit Suisse AT1 bonds, the seemingly contradictory interpretations by the SRB and ECB, and the initial panic in the AT1 bond market following the write-down have undermined the market for this important instrument and source of capital for banks. It would be a shame if the outcome of the Credit Suisse event were the elimination of CoCos from bank regulatory capital when the Credit Suisse CoCos have precisely fulfilled their purpose: allowing for a swift and seamless recapitalization, which facilitated the completion of the merger deal with UBS, and so limited Swiss taxpayers exposure to losses from Credit Suisse. In its decision FINMA also creates a healthy precedent: restoring financial discipline in AT1 bond markets by reminding investors that their investment bears the first brunt of credit risk and that due diligence is advised before investing in these products.</p><p>But reform and simplification of CoCo designs is desirable with all the confusion around the Credit Suisse event. One design proposal that has been overlooked in the early stages of introduction of CoCos following the great financial crisis that is worth revisiting is the CoCo design proposed by one of the present writers with Frederic Samama in our 2012 article in <i>Economic Policy</i>.19 The proposed design has three main virtues: simplicity, off-the-shelf pricing, and seamless recapitalization. The design, more specifically, is a CoCo without automatic or discretionary trigger, but instead an option for the issuer to convert the fixed-income claim into equity. Under this design, the CoCo-issuing bank would in essence purchase a (collateralized) option to issue new equity at a pre-specified strike price, as opposed to the conventional convertible bonds for which the investor holds the conversion option.</p><p>This is unambiguously the right design for a going-concern CoCo. It is not a substitute for debt resolution, but instead a capital line commitment for the issuing bank. It is, in effect, a form of insurance against adverse changes in equity markets that enables the issuing bank to raise equity capital at predictable terms in a crisis. In 2012, with Frederic Samama, we showed that such a capital line commitment lowers the costs of holding an equity capital buffer for banks by allowing them to raise equity capital only when it is needed at a pre-determined cost.</p><p>Because this CoCo design is structured as a reverse convertible bond (a collateralized put option for the issuer), the optimal conversion point is predictable based on well-established option pricing theory, and thus the pricing of the CoCo is straightforward using an off-the-shelf option pricing model. As a result, uncertainty and ambiguity around the instrument is substantially reduced.</p><p>Another advantage of this instrument is that it provides a simple solution to implementing countercyclical equity capital. The CoCo bond gives the issuer the option to issue new capital at favorable terms in a difficult time, often in recession, and thus relaxes its equity capital constraint. This CoCo design is, in effect, a form of countercyclical capital with the added flexibility that the issuer can decide when it is appropriate to recapitalize, thus removing the pressure on regulators to decide when it is appropriate to relax the equity capital requirement. Moreover, under this design the issuer optimally converts the CoCo into equity when the equity price-to-face value ratio is low, thereby recapitalizing the bank and strengthening its balance sheet just when it is needed.</p><p>Finally, the reverse convertible CoCo design eliminates the involvement of the regulator in the conversion decision (and all the associated legal risks), as is currently the case due to the discretionary trigger requirements of AT1 capital instruments under Basel III. In the aftermath of the Credit Suisse CoCo write-down, investors have sued the Swiss regulatory authority for a government-orchestrated rescue that led to investors’ assets being “expropriated” following the Credit Suisse takeover by UBS.20</p><p>The collapse of Credit Suisse offers an important lesson for financial regulators. Despite their enormous effort to set up resolution regimes for GSIBs after the GFC, the complexity and lack of transparency of resolution procedures has so increased the risk of resolving a GSIB like Credit Suisse that the Swiss regulatory authorities decided that a purchase and assumption deal with UBS backed by the SNB was safer.</p><p>According to the <i>Financial Times</i>,21 at the critical meeting between the Swiss regulatory authorities and Credit Suisse on Wednesday, March 15, 2023, where the SNB “authorized the CHF 50bn backstop, they also delivered another message: “You will merge with UBS and announce Sunday evening before Asia opens. This is not optional,” a person briefed on the conversation recalls.” “Resolution would have been a disaster for the financial system and introduced the threat of contagion around the world,” another UBS executive at the meeting declared. “Our interests were also aligned because a failure is not good for the Swiss wealth-management brand. So we said, on the right terms, we would help.” Later, Karin Keller-Sutter, finance minister and one of the seven members of the Swiss Federal Council, declared in an interview with the <i>Neue Zurcher Zeitung</i> that resolving Credit Suisse “would have triggered an international financial crisis… a globally active systemically important bank cannot simply be wound up according to the ‘too big to fail’ plan. Legally this would be possible. In practice, however, the economic damage would be considerable. The crash of Credit Suisse would have dragged other banks into the abyss.”22</p><p>No one disputes this assessment. The inevitable implication is that financial regulators must reassess the current approach to the too-big-to-fail problem and SIFI resolution. What is the point of TLAC and living wills if when push comes to shove regulators choose a bailout over resolution. One important positive outcome of the Credit Suisse crisis, however, is that it has shown that $17 billion of CoCos can be written off without dragging the banking system into the abyss. This quick and efficient debt write-down has gone some way in addressing the too-big-to-fail problem and has significantly reduced the cost of saving Credit Suisse for the Swiss taxpayer.</p><p>Of all the too-big-to-fail tools, the Credit Suisse CoCos did play their intended role. Going forward, financial regulation should focus on enhancing the role of contingent capital like CoCos that can be activated prior to a bank's failure. Furthermore, regulators also need to review the great variety of CoCo designs in terms of their conversion mechanism and their trigger level. Discretionary (PONV) triggers that are widespread in CoCos offer regulators a possibility to act in the middle of the crisis. But the regulatory discretion makes it difficult to price the risk of conversion and, as we showed in 2020, thereby reduces the effectiveness of CoCos.23 In 2012, we proposed an alternative CoCo design, providing the issuing bank an option to convert into equity.24 These are more standard, transparent, and flexible instruments designed to give banks the opportunity to recapitalize during a crisis, and they are more robust to price manipulation because the trigger is at the discretion of the issuer. Improving and refining CoCo requirements that enable recapitalization of a troubled but viable bank should be the focus of regulators in Switzerland and worldwide in the coming months and years.</p>","PeriodicalId":46789,"journal":{"name":"Journal of Applied Corporate Finance","volume":"35 2","pages":"66-74"},"PeriodicalIF":1.4000,"publicationDate":"2023-06-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12553","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Corporate Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12553","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

The response to the global financial crisis (GFC) of 2007–2008 has famously been described as the problem of too-big-to-fail.1 In the middle of a worsening crisis, financial regulators had to recognize that bank bailouts were the only way to stabilize financial markets. One of the two priorities of regulatory reforms post-crisis was to address the too-big-to-fail problem by introducing a resolution procedure for systemically important financial institutions.2 Among financial regulators (with the notable exception of the USA), contingent convertible bonds (CoCos) were seen as a major innovation to address the too-big-to-fail problem and quickly became a popular “bail-in” instrument to facilitate the instant recapitalization of a distressed bank. The quick deleveraging that could be achieved with CoCo conversions would serve the dual roles of recapitalizing “a going-concern bank” and reducing the resolution costs for a “gone concern” bank.

During the press conference on March 19, 2023 the Swiss Financial Market Supervisory Authority (FINMA) announced that, as part of the emergency package in response to the loss of trust and the run on Credit Suisse, the contingent convertible bonds that were part of the Credit Suisse Additional Tier 1 (AT1) regulatory capital had been written off.3 The decision by FINMA took many by surprise and provoked a flood of negative market commentary, with the commonly stated view that conversion violated the priority order of claims between debt and equity. Indeed, in the final rescue deal, the shareholders of Credit Suisse retain around $3 billion of equity value, while the CoCo bond principal write-down amounted to a wipeout of $17 billion for CoCo investors. Implicitly corroborating this commentary, the European Central Bank (ECB), the Bank of England, and other regulators made public statements on the Monday following the Credit Suisse deal that they do not intend to follow the FINMA approach and that they intend to respect the usual priority order of claims in resolution.4 How can these divergent views of regulators be reconciled? Why did the Credit Suisse AT1 CoCo bondholders face losses before shareholders were wiped out? What are the lessons for the effectiveness of post-GFC too-big-to-fail reforms? This article provides clarification of these important questions.

CoCo bonds are designed to absorb losses of a distressed going-concern bank at conversion, thereby helping to capitalize the bank. Their primary purpose is to reduce the need for a capital injection by the government in times of crisis when nobody else is willing to provide additional external capital. Such public support is costly to taxpayers and exacerbates moral hazard.

CoCo bonds have two main contract features: the loss absorption mechanism and the trigger that activates that mechanism (illustrated in Graph 1).5 CoCos can absorb losses either by converting into common equity or through a principal write-down (partial or full). The trigger can be either mechanical (i.e., defined in terms of a capital ratio) or discretionary (subject to supervisory judgment).

The trigger defines the point at which the loss absorption mechanism is activated. The mechanical trigger activates the loss absorption mechanism when the capital of the CoCo-issuing bank drops below a pre-specified fraction of its risk-weighted assets. The bank's equity capital can be measured either based on book value or market value. The discretionary, or point of non-viability (PONV), trigger is activated based on the supervisor's assessment of the bank's possible insolvency. PONV triggers give regulators authority to convert, if and when they decide that the issuer has reached that state. Because the PONV is difficult to determine ex ante, PONV triggers introduce uncertainty about the timing and circumstances leading to the activation of the loss absorption mechanism by the regulator.

CoCo bonds typically have more than one trigger. In case of multiple triggers, the loss absorption mechanism can be activated when any trigger is breached. Under Basel III rules, all regulatory capital CoCos are required to have a discretionary PONV trigger. The activation of the discretionary trigger, which was present in all CoCos issued by Credit Suisse, was exactly what allowed FINMA to write down Credit Suisse AT1 capital instruments on March 19, 2023.

The loss absorption mechanism is the second contract feature of CoCos. Once the trigger is activated, CoCos can be either converted to equity at a pre-defined conversion rate or subject to a principal write-down. In either case, the conversion delevers the bank and/or boosts its equity capital ratio. For conversion to equity CoCos, the conversion rate can be based either on the market price of the stock at the time of conversion, or on a pre-specified price, like the stock price at the time of issuance. It is also possible to have a combination of market price and prespecified price floor, where the latter defines the floor for the conversion rate and hence protects existing equity holders from unlimited dilution. The various options for setting the conversion price lead to different exposures to dilution risk for existing equity holders, and thus create varying incentives to avoid conversion by existing equity holders. In the case of the principal write-down CoCos, the haircut can be either full or partial. However, most of the principal write-down CoCos of Credit Suisse were full write-down CoCos. The write-down CoCos potentially encourage risk taking by managers acting in the interest of shareholders.

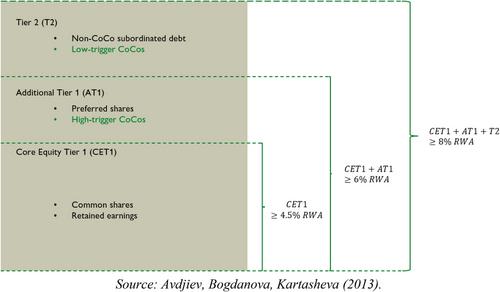

The regulatory treatment of CoCos under Basel III and the supplementary requirements of national regulators shape the design choices of CoCo contract features of issuing banks (that can be seen in Graph 2). Under the Basel III framework, CoCos must satisfy two requirements to qualify as regulatory capital. The first requirement, which applies to both AT1 and T2 instruments, is satisfied by the PONV trigger. The second requirement is the going-concern rule, which specifies that the minimum trigger level of CET1/RWA to qualify as AT1 is 5.125%. In addition, AT1 instruments must be perpetual. Importantly, these features are not necessarily outcomes of optimal financial contracting between the issuer and its investors.

The regulatory rationale for CoCos is to improve banks’ resilience to financial shocks by strengthening their capital buffers in a crisis, while also providing investors with an investment opportunity that is distinct from debt and equity. By issuing CoCos, banks can raise capital while limiting the dilution costs of current shareholders at issuance and reduce the likelihood of becoming insolvent or requiring a government bailout. In particular, CoCos allow banks to seamlessly recapitalize during times of financial stress. The conversion or write-down of CoCos allows the bank to transfer some of the losses to CoCo investors, ensuring that the costs of bank failures are borne by investors rather than taxpayers. In addition to reducing the cost of distress, the possibility of CoCo conversion provides bankers with incentives to limit the probability of distress.

CoCos can be an attractive investment opportunity for long-term investors who understand and are able to take losses in a crisis. CoCos typically offer higher yields than traditional bonds due to their contingent nature, their low priority ranking (on par or even lower than equity investors), and the high systematic component in their risk. Because institutional mandates often block traditional fixed income investors from taking positions in conversion to equity CoCos, the market yield on the instruments may also contain a premium for sophisticated and flexible investors in terms of market segregation.

In their 2013 Primer on CoCos published by the Bank for International Settlements, colleagues Stefan Avdjiev, Anastasia Kartasheva, and Bilyana Bogdanova show that the yield-to-maturity of newly issued CoCos are on average 2.8% higher than the subordinated debt, and 4.7% higher than the senior unsecured debt, of the same bank.6 However, the popularity of CoCos could also be partly driven by the search for yield in a low interest rate environment, which have been touted by financial advisors that sometimes misrepresented the product as a relatively safe way of boosting yield.

CoCos are often perceived as similar to total loss absorbing capacity (TLAC) instruments, since they are also financial instruments designed to “bail-in” troubled systemically important banks. There are, however, key differences between the two. The primary purpose of CoCos is to delever a bank amid a crisis, by writing down debt or providing equity capital, or both. CoCos are thus designed to maintain the equity cushion of a going concern bank. TLAC, which are usually T2 capital, are additional loss absorption requirements for global systemically important banks (GSIBs) like Credit Suisse to enable a single point of entry resolution. The goal of TLAC is to ensure that the holding companies of systematically important banks have sufficient capacity to absorb losses so that their operating affiliates can continue operating without putting their liabilities at risk. By contrast, CoCo conversion could take place while the bank is still a going concern.

A 2020 article in the Journal of Financial Economics we wrote with Stefan Avdjiev and Bilyana Bogdanova provides the first comprehensive analysis of bank CoCo issuance.7 Out of the 731 Coco issues raising over $500 billion between 2009 and 2015, European issues took the largest share (39%), while U.S. was absent from the list. At the time of the Credit Suisse trigger event, the global AT1 CoCos market was estimated to be $254 billion.8 About 56% of these CoCos include a mechanical trigger. Though in the first years of our sample mandatory conversion CoCos were prevalent, principal write-down CoCos have become more popular over time, eventually dominating the market. Finally, slightly more than half (55%) of the CoCos up to 2015 were classified as AT1 capital, while most of the T2 CoCos tend to be issued by banks in emerging economies.

Our 2020 Journal of Financial Economics article also shows that the propensity to issue a CoCo is higher for larger and better capitalized banks. Presumably only relatively healthy banks, with remote conversion risk, are able to issue CoCos at a reasonable cost. Another reason is that the principal beneficiaries from a CoCo issue are senior bondholders, whereas shareholders expose themselves to dilution risk. The same JFE article shows that the CDS spreads of CoCo issuers decline upon the announcement of a CoCo issue, indicating that they generate risk-reduction benefits and lower costs of debt. While the average reduction in CDS spread was 2.7 basis points, the drop was more prominent for conversion CoCos (5.0 bps), including those with mechanical triggers (3.3 bps). Conversion CoCos with mechanical triggers are also associated with a reduction of 6.2 bps in CDS spreads. Only Additional Tier 1 instruments contributed to the reduction of CDS.

Finally, CoCo issuances have no statistically significant impact on the issuers’ stock prices, except for the case of principal write-down CoCos with high trigger levels, which involve no dilution risk for shareholders and for which stock price responses have been significantly positive on average. Such a contrast suggests a potential moral hazard on shareholders’ part to take excess risk, since the cost will be first borne by the holders of write-down CoCos. CoCos that convert to equity offer a superior design from the point of view of reducing bank fragility. In the case of Credit Suisse, all outstanding CoCos were principal write-down CoCos, and this is the reason why their investors received no equity stake in the merger with UBS. Had they issued conversion to equity CoCos, they would have received shares in the merged company.

The collapse of Silicon Valley Bank (SVB) on March 10, 2023 sent shockwaves through the financial system and quickly drew investors’ attention to the prominent weaknesses at Credit Suisse, which was impelled to seek up to CHF 50bn in liquidity support from the Swiss National Bank (SNB) on March 16, 2023. This dramatic move failed to quash speculation, or slow down deposit withdrawals, to the extent that 2 days later the SNB and FINMA announced that they had begun proceedings to organize a takeover of Credit Suisse by UBS.

The Swiss financial regulatory authorities had decided that the best way to avert another GFC was to rescue Credit Suisse through a merger with a strong financial institution, following the playbook of the Federal Reserve and US Treasury in 2008 with its rescue of Bear Stearns through a merger with JPMorgan and what has colloquially become known as the “Jamie deal” in reference to the CEO of JPMorgan.9

It is revealing to contrast these two deals, as the contexts are different and the limits on the legal authorities of regulators are different. The Federal Reserve and Treasury did not have nearly the same authority to push through a merger as the Swiss government under the Swiss emergency law. The Federal Reserve had to invoke section 13(3) of the Federal Reserve Act to claim authority to provide liquidity support “under unusual and exigent circumstances” to a broker-dealer. Beyond the authority to provide liquidity support the Federal Reserve (and US Treasury) had no means other than moral suasion to get the management of Bear Stearns and JPMorgan to agree to merge at a proposed price of $2 per Bear Stearns share. They had no authority to sidestep shareholder agreements at both Bear Stearns and JPMorgan, and they could not write down Bear Stearns liabilities outside Chapter 11 bankruptcy. The only way the deal could be structured outside bankruptcy was as a purchase-and-assumption deal whereby JPMorgan agreed to assume all Bear Stearns liabilities. However, even at the price of $2 per share, this was seen as too risky by JPMorgan management and might not receive the blessing of JPMorgan shareholders.

To overcome this hurdle the Federal Reserve agreed to back up the deal by setting up an innovative collateralized special purpose vehicle—Maiden Lane LLC. This vehicle would be financed with a junior tranche of $1 billion from JPMorgan and a $29 billion senior tranche of the Federal Reserve, and it would purchase up to $30 billion worth of troubled assets of Bear Stearns, thereby de-risking the Bear Stearns balance sheet. The Federal Reserve and Treasury also had to make concessions to Bear Stearns shareholders by eventually raising the share price to $10.10 Although this deal was successfully implemented in May 2008, and temporarily brought back some calm in financial markets, a few months later a similar merger attempt between Lehman Brothers and Barclays failed, unleashing the GFC.

The Swiss regulatory authorities were in a much better position to engineer a deal between Credit Suisse and UBS. They could bypass shareholder approval, bringing a swift resolution of uncertainty, and they did not have to put public money at risk by setting up a complex special purpose vehicle to de-risk the Credit Suisse balance sheet. All they had to do was trigger the write-down of Credit Suisse CoCos that had been designed and issued precisely for such a contingent event. And FINMA did just that, announcing that “the extraordinary government support [of Credit Suisse] will trigger a complete write-down of the nominal value of all AT1 shares of Credit Suisse in the amount of around CHF16bn, and thus an increase in core capital.”11 The principal write-down of these AT1 instruments allowed for a swift de-levering of the Credit Suisse balance sheet.

Recall that one of the main criticisms of the Bear Stearns rescue, and later interventions in the fall of 2008, has been that the complete bailout of creditors in all these rescues created a dangerous moral hazard in lending precedent.12 Viewed in this light, the write-down of the Credit Suisse AT1 bonds would not only help de-risk the Credit Suisse balance sheet but also help counter market expectations that creditors of systemically important financial institutions would always be bailed out in a crisis.

Although the write-down of Credit Suisse CoCos following the rescue of Credit Suisse was predictable, it caused consternation in financial markets and a mini crisis in the AT1 bond market. Investors in Credit Suisse AT1 bonds were surprised that their bonds had been written down even though Credit Suisse shareholders remained standing, the first such incidence in the CoCo history.

To many people, as we have noted, this seemed to be an egregious violation of absolute priority. Jérôme Legras, a managing partner and head of research at Axiom Alternative Investments, told the Financial Times: “The market is likely to be shocked by such a blatant inversion of the hierarchy of creditors and by the decision to sweeten an equity deal at the expense of bond holders.” There had been a precedent of a similar CoCo write-down in 2017 when Banco Popular was taken over by Santander, but in that case Banco Popular shareholders had essentially been wiped out, so that there was at least an appearance that part of the absolute priority, that is, equity being the most junior claim, had been respected.

It is not just investors who were taken off guard but also financial regulators outside Switzerland. Fearing potential contagion in the $250 billion AT1 bond market, Dominique Laboureix, chair of the EU's Single Resolution Board (SRB) quickly reacted, saying on CNBC that “In a resolution here, in the European context, we would follow the hierarchy, and we wanted to tell it very clearly to the investors, to avoid to be misunderstood: we have no choice but to respect this hierarchy.”13 On the Monday following FINMA's decision the SRB together with the EBA and ECB issued the statement: “… common equity instruments are the first ones to absorb losses, and only after their full use would Additional Tier 1 be required to be written down. This approach has been consistently applied in past cases and will continue to guide the actions of the SRB and ECB banking supervision in crisis interventions.”14

These reactions from business and regulatory leaders understandably only led to further confusion. It was only a matter of a few days before talk of lawsuits emerged. The law firm Quinn Emanuel Urquhart & Sullivan and Pallas Partners quickly announced that a lawsuit was in order, portraying the Credit Suisse rescue as “a resolution dressed up as a merger,” and commenting on the SRB and ECB responses that “you know something has gone wrong when other regulators come and politely point out that in a resolution [they] would have respected ordinary priorities”. Major investors like David Tepper, the founder and president of Appaloosa Management, a global hedge fund, further weighed in that, “if this is left to stand, how can you trust any debt security issued in Switzerland, or for that matter wider Europe, if governments can just change laws after the fact… contracts are made to be honoured.”15

But did FINMA, in fact, change the terms ex post and violate the contractual obligations of AT1 bonds? As highlighted above, most of the recent CoCos issued by Credit Suisse are principal write-down CoCos with very similar terms. For example, the SGD 750,000,000 CoCo issued in Singapore on May 29, 2019, contains the following terms: “CET1 Write-down Trigger: 7.00%, based on Credit Suisse Group AG consolidated CET1 ratio. Write-down: If a Contingency Event, or prior to a Statutory Loss Absorption Date (if any), a Viability Event occurs, the full principal amount of the notes will be mandatorily and permanently written down…. See “Terms and Conditions of the Notes—Condition 7 “Write-down”” in the Information Memorandum for the definitions of Contingency Event, Statutory Loss Absorption Date and Viability Event.”

The information memorandum further states that “A “Contingency Event” will occur if (i) Credit Suisse group's consolidated common equity tier 1 (“CET1”) divided by its consolidated risk weighted assets (“RWA”) as of any quarterly balance sheet date (or, in the case of certain of these instruments, such other date specified by FINMA) is below 7%, and (ii) FINMA has not agreed in writing prior to publication of such CET1/RWA ratio that a full conversion or write-off, as applicable, shall not occur because it is satisfied that actions, circumstances or events have had, or imminently will have, the effect of restoring the CET1/RWA ratio to a level above 7% that it deems to be adequate.”

In addition, the following provision clarifies PONV: “A ‘Viability Event’ will occur if either (i) FINMA notifies CSG that it has determined that a conversion or write-off of the relevant instrument, together with the conversion or write-off of holders' claims in respect of all other regulatory capital instruments issued by a member of the Credit Suisse group that, pursuant to their terms or by operation of law, are capable of being converted into equity or written-off at that time, is, because customary measures to improve CSG's capital adequacy are at the time inadequate or unfeasible, an essential requirement to prevent CSG from becoming insolvent, bankrupt or unable to pay a material part of its debts as they fall due, or from ceasing to carry on its business, or (ii) customary measures to improve CSG's capital adequacy being at the time inadequate or unfeasible, CSG receives an irrevocable commitment of extraordinary support from the public sector (beyond customary transactions and arrangements in the ordinary course) that has, or imminently will have, the effect of improving CSG's capital adequacy and without which, in the determination of FINMA, CSG would have become insolvent, bankrupt, unable to pay a material part of its debts as they fall due or unable to carry on its business. The occurrence of either or both of these two events is also referred to as the ‘Point of Non-Viability’ or the ’PONV’.”

The additional Credit Suisse documentation on AT1 bonds further states that: “under certain circumstances, FINMA has the power to open restructuring proceedings with respect to CSG under Swiss banking laws (see “—CSG is subject to the resolution regime under Swiss banking laws and regulations” below), and, if the Notes have not already been subject to a write-down, could convert the Notes into equity or cancel the Notes, in each case, in whole or in part. Holders should be aware that, in the case of any such conversion into equity, FINMA would follow the order of priority set out under Swiss banking laws, which means, among other things, that the Notes would have to be converted prior to the conversion of any of CSG's subordinated debt that does not qualify as regulatory capital with a contractual write-down or conversion feature. Furthermore, in the case of any such cancellation, FINMA may not be required to follow any order of priority, which means, among other things, that the Notes could be cancelled in whole or in part prior to the cancellation of any or all of CSG's equity capital.”

Granted, such provisions are not easy to follow. FINMA nevertheless exercised its authority under these contracts to trigger conversion because it deemed that Credit Suisse had reached the PONV. The Credit Suisse CoCos were not “gone concern” CoCos but “going concern” CoCos. By triggering these CoCos, FINMA implemented the AT1 contracts as they were intended to be—namely, to allow for a swift recapitalization so that Credit Suisse could be brought back to viability after reaching a point toward insolvency.

A first lawsuit has been filed by Quinn Emanuel Urquhart & Sullivan and Pallas Partners against FINMA on April 21, 2023, claiming that the AT1 bond write-down was disproportionate and that FINMA did not act in good faith.16

Following the collapse of SVB, pressures further built up on Credit Suisse with both its stock price falling and its CDS spread rising (Graph 3). Financial markets clearly reflected an increase in investors’ perceived probability of a failure and the announcement of the $50 billion borrowing facility from the SNB did not reverse these expectations. Though investors clearly entertained the possibility that there could be a default on Credit Suisse bonds, as priced in the rising CDS spreads, interestingly, the figure below suggests that investors did not anticipate a write-down of AT1 bonds until mid-March, on the eve of the takeover of Credit Suisse (Graph 4).

It is difficult to say what proportion of investors anticipated the possibility of a write-down of AT1 bonds even if shareholders were not completely wiped out. As the example above of the Credit Suisse CoCo bond issued in Singapore in 2019 shows, these bonds offered higher interest rates than plain vanilla bonds as compensation for the risk of a write-down. These higher coupon rates attracted yield-searching investors in a low interest rate environment, and their high yields were part of a major sales pitch. Reports like this one in January 2021 by a Credit Suisse portfolio manager exemplifies the sentiment of complacence “The CoCo market offers a yield of around 3.62% … even European high-yield bonds come in at around 2.88%, so we definitely still see value in subordinated financial bonds … The average European bank would need to lose almost two-thirds of its capital to breach contractual triggers.”17 Many investors in AT1 bonds may not have been aware of the risks they were exposed to, given that CoCos were pitched as highly remunerative fixed-income securities issued by very stable systemically important financial institutions. Many might also be unaware of the fact that written-down CoCos are effectively junior to equity. This is for example the view expressed by the CEO of Farro Capital: “Most Asian private banks market AT1 bonds as fixed-income securities, and people get excited with the enhanced yields on these.”18

The surprise effect of FINMA's decision can also be seen in the AT1 bond market reaction following the write-down. As the figure below shows, there was a temporary panic in this market in the days following the Credit Suisse takeover, in addition to the realization of the contingent nature of CoCos. But the market has since recovered (Graph 5).

Except for the Banco Popular CoCo write-down in 2017, there was no precedent of CoCo conversion one could learn from until the Credit Suisse event. Would CoCos work as intended? Would CoCo conversion or write-down shore up the balance sheet of a bank in distress and help stabilize financial markets? We could only speculate and our analysis in our 2020 Journal of Financial Economics article could look at only what investors expected at the time of issuance. Even though the Credit Suisse event gives us only one observation, many lessons can already be drawn from this event.

The first obvious lesson is that the way CoCos have been structured is creating a lot of confusion. Even some sophisticated investors appear to have been confused about the difference between going-concern and gone-concern CoCos. Investors often did not know that there was a distinction, and for those who did, it was not easy to tell the difference. The function of going concern CoCos is to allow the bank could stay viable by triggering a write-down, that is, before equity investors are wiped out. Another layer of complexity that gave rise to a lot of uncertainty in the Credit Suisse event is the existence of multiple triggers, an automatic trigger when a CET1 capital ratio is triggered and a discretionary trigger that the financial regulator could activate if it deemed that the issuer had reached the PONV.

This contractual complexity gives rise to unnecessary and costly uncertainty. It also increases the risk of misrepresentation to investors. One of the challenges with the discretionary trigger is determining what the PONV is precisely. No clear criteria have been defined, giving regulators considerable discretion ex post, and giving rise to regulatory uncertainty. The fact that the SRB and ECB felt that they had to reassure markets that they did not intend to deviate from absolute priority to calm the AT1 bond market is revealing evidence of the extent of regulatory ambiguity that is embedded in these instruments, which leads to pricing complexity. Both the automatic and discretionary triggers, and their combination, increase the difficulty in predicting accurately the probability of a CoCo being triggered. There are no off-the-shelf financial models that can be used to price these contingent securities.

Investor dismay with FINMA's decision to write down Credit Suisse AT1 bonds, the seemingly contradictory interpretations by the SRB and ECB, and the initial panic in the AT1 bond market following the write-down have undermined the market for this important instrument and source of capital for banks. It would be a shame if the outcome of the Credit Suisse event were the elimination of CoCos from bank regulatory capital when the Credit Suisse CoCos have precisely fulfilled their purpose: allowing for a swift and seamless recapitalization, which facilitated the completion of the merger deal with UBS, and so limited Swiss taxpayers exposure to losses from Credit Suisse. In its decision FINMA also creates a healthy precedent: restoring financial discipline in AT1 bond markets by reminding investors that their investment bears the first brunt of credit risk and that due diligence is advised before investing in these products.

But reform and simplification of CoCo designs is desirable with all the confusion around the Credit Suisse event. One design proposal that has been overlooked in the early stages of introduction of CoCos following the great financial crisis that is worth revisiting is the CoCo design proposed by one of the present writers with Frederic Samama in our 2012 article in Economic Policy.19 The proposed design has three main virtues: simplicity, off-the-shelf pricing, and seamless recapitalization. The design, more specifically, is a CoCo without automatic or discretionary trigger, but instead an option for the issuer to convert the fixed-income claim into equity. Under this design, the CoCo-issuing bank would in essence purchase a (collateralized) option to issue new equity at a pre-specified strike price, as opposed to the conventional convertible bonds for which the investor holds the conversion option.

This is unambiguously the right design for a going-concern CoCo. It is not a substitute for debt resolution, but instead a capital line commitment for the issuing bank. It is, in effect, a form of insurance against adverse changes in equity markets that enables the issuing bank to raise equity capital at predictable terms in a crisis. In 2012, with Frederic Samama, we showed that such a capital line commitment lowers the costs of holding an equity capital buffer for banks by allowing them to raise equity capital only when it is needed at a pre-determined cost.

Because this CoCo design is structured as a reverse convertible bond (a collateralized put option for the issuer), the optimal conversion point is predictable based on well-established option pricing theory, and thus the pricing of the CoCo is straightforward using an off-the-shelf option pricing model. As a result, uncertainty and ambiguity around the instrument is substantially reduced.

Another advantage of this instrument is that it provides a simple solution to implementing countercyclical equity capital. The CoCo bond gives the issuer the option to issue new capital at favorable terms in a difficult time, often in recession, and thus relaxes its equity capital constraint. This CoCo design is, in effect, a form of countercyclical capital with the added flexibility that the issuer can decide when it is appropriate to recapitalize, thus removing the pressure on regulators to decide when it is appropriate to relax the equity capital requirement. Moreover, under this design the issuer optimally converts the CoCo into equity when the equity price-to-face value ratio is low, thereby recapitalizing the bank and strengthening its balance sheet just when it is needed.

Finally, the reverse convertible CoCo design eliminates the involvement of the regulator in the conversion decision (and all the associated legal risks), as is currently the case due to the discretionary trigger requirements of AT1 capital instruments under Basel III. In the aftermath of the Credit Suisse CoCo write-down, investors have sued the Swiss regulatory authority for a government-orchestrated rescue that led to investors’ assets being “expropriated” following the Credit Suisse takeover by UBS.20

The collapse of Credit Suisse offers an important lesson for financial regulators. Despite their enormous effort to set up resolution regimes for GSIBs after the GFC, the complexity and lack of transparency of resolution procedures has so increased the risk of resolving a GSIB like Credit Suisse that the Swiss regulatory authorities decided that a purchase and assumption deal with UBS backed by the SNB was safer.

According to the Financial Times,21 at the critical meeting between the Swiss regulatory authorities and Credit Suisse on Wednesday, March 15, 2023, where the SNB “authorized the CHF 50bn backstop, they also delivered another message: “You will merge with UBS and announce Sunday evening before Asia opens. This is not optional,” a person briefed on the conversation recalls.” “Resolution would have been a disaster for the financial system and introduced the threat of contagion around the world,” another UBS executive at the meeting declared. “Our interests were also aligned because a failure is not good for the Swiss wealth-management brand. So we said, on the right terms, we would help.” Later, Karin Keller-Sutter, finance minister and one of the seven members of the Swiss Federal Council, declared in an interview with the Neue Zurcher Zeitung that resolving Credit Suisse “would have triggered an international financial crisis… a globally active systemically important bank cannot simply be wound up according to the ‘too big to fail’ plan. Legally this would be possible. In practice, however, the economic damage would be considerable. The crash of Credit Suisse would have dragged other banks into the abyss.”22

No one disputes this assessment. The inevitable implication is that financial regulators must reassess the current approach to the too-big-to-fail problem and SIFI resolution. What is the point of TLAC and living wills if when push comes to shove regulators choose a bailout over resolution. One important positive outcome of the Credit Suisse crisis, however, is that it has shown that $17 billion of CoCos can be written off without dragging the banking system into the abyss. This quick and efficient debt write-down has gone some way in addressing the too-big-to-fail problem and has significantly reduced the cost of saving Credit Suisse for the Swiss taxpayer.

Of all the too-big-to-fail tools, the Credit Suisse CoCos did play their intended role. Going forward, financial regulation should focus on enhancing the role of contingent capital like CoCos that can be activated prior to a bank's failure. Furthermore, regulators also need to review the great variety of CoCo designs in terms of their conversion mechanism and their trigger level. Discretionary (PONV) triggers that are widespread in CoCos offer regulators a possibility to act in the middle of the crisis. But the regulatory discretion makes it difficult to price the risk of conversion and, as we showed in 2020, thereby reduces the effectiveness of CoCos.23 In 2012, we proposed an alternative CoCo design, providing the issuing bank an option to convert into equity.24 These are more standard, transparent, and flexible instruments designed to give banks the opportunity to recapitalize during a crisis, and they are more robust to price manipulation because the trigger is at the discretion of the issuer. Improving and refining CoCo requirements that enable recapitalization of a troubled but viable bank should be the focus of regulators in Switzerland and worldwide in the coming months and years.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们