{"title":"Transparency of local government financial statements: Analyzing citizens’ perceptions","authors":"Ellen Haustein, Peter C. Lorson","doi":"10.1111/faam.12353","DOIUrl":null,"url":null,"abstract":"<p>Worldwide, open data initiatives aim at making information publicly available and transparent. Increasingly, local governments (LGs) are publishing financial statements in order to inform citizens, in their function as both service recipients and resource providers, about the LGs’ financial situation. However, it remains questionable as to whether LG financial statements are appropriate mechanisms of public accountability: it is debated, on the one hand, whether citizens are interested in accounting information, and on the other hand, if they are able to understand the information presented in financial statements. This study is the first of its kind applying the think aloud method to analyze citizens’ perceptions of LGs’ financial statements in a sample of 30 German citizens with diverse socio-demographic characteristics. The paper explores citizens’ general interest in accounting information and their ability to extract basic financial information from these statements so that increased transparency can be assumed. This explorative study reveals that although citizens demand transparency and financial information, they find it challenging to understand financial statements. Citizens seem to be overwhelmed by the information and call for delegation of the tasks or simplified reporting formats.</p>","PeriodicalId":47120,"journal":{"name":"Financial Accountability & Management","volume":"39 2","pages":"375-393"},"PeriodicalIF":2.6000,"publicationDate":"2022-11-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/faam.12353","citationCount":"3","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Accountability & Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/faam.12353","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 3

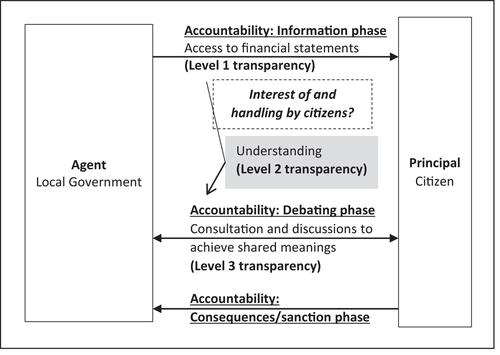

Abstract

Worldwide, open data initiatives aim at making information publicly available and transparent. Increasingly, local governments (LGs) are publishing financial statements in order to inform citizens, in their function as both service recipients and resource providers, about the LGs’ financial situation. However, it remains questionable as to whether LG financial statements are appropriate mechanisms of public accountability: it is debated, on the one hand, whether citizens are interested in accounting information, and on the other hand, if they are able to understand the information presented in financial statements. This study is the first of its kind applying the think aloud method to analyze citizens’ perceptions of LGs’ financial statements in a sample of 30 German citizens with diverse socio-demographic characteristics. The paper explores citizens’ general interest in accounting information and their ability to extract basic financial information from these statements so that increased transparency can be assumed. This explorative study reveals that although citizens demand transparency and financial information, they find it challenging to understand financial statements. Citizens seem to be overwhelmed by the information and call for delegation of the tasks or simplified reporting formats.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们