{"title":"Volatility Spillovers Among the Three Places Across the Taiwan Strait: Evidence from a BEKK-CARR Approach*","authors":"Chun Chou Wu, Wen Xu","doi":"10.1111/ajfs.12405","DOIUrl":null,"url":null,"abstract":"<p>This study introduces a new BEKK-CARR model to explore the volatility spillover effects among mainland China, Hong Kong, and Taiwan stock markets during the COVID-19 pandemic. We also extend the approach of Diebold and Yilmaz (2009, 2012) to infer a brand-new volatility spillover index to discuss the bi-directional volatility transmission. Our results show that the trading information flow among these three markets has changed significantly as a result of the COVID-19 pandemic. The strength of volatility spillover is increasing during this momentous period. The Hong Kong stock market plays a pivotal role in volatility transmission. The values for half-lives by exogenous shocks keep relatively low during the pandemic period. A reasonable explanation is that the trading information transmissions among stock markets are quicker than in the non-pandemic period.</p>","PeriodicalId":8570,"journal":{"name":"Asia-Pacific Journal of Financial Studies","volume":"51 6","pages":"896-913"},"PeriodicalIF":1.5000,"publicationDate":"2023-01-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ajfs.12405","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Journal of Financial Studies","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ajfs.12405","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

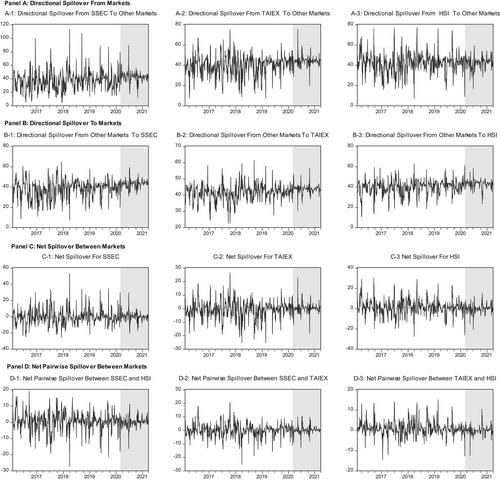

Abstract

This study introduces a new BEKK-CARR model to explore the volatility spillover effects among mainland China, Hong Kong, and Taiwan stock markets during the COVID-19 pandemic. We also extend the approach of Diebold and Yilmaz (2009, 2012) to infer a brand-new volatility spillover index to discuss the bi-directional volatility transmission. Our results show that the trading information flow among these three markets has changed significantly as a result of the COVID-19 pandemic. The strength of volatility spillover is increasing during this momentous period. The Hong Kong stock market plays a pivotal role in volatility transmission. The values for half-lives by exogenous shocks keep relatively low during the pandemic period. A reasonable explanation is that the trading information transmissions among stock markets are quicker than in the non-pandemic period.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们