Miguel Ángel Royo-Bordonada, Carlos Fernández-Escobar, Carlos José Gil-Bellosta, Elena Ordaz

{"title":"Effect of excise tax on sugar-sweetened beverages in Catalonia, Spain, three and a half years after its introduction.","authors":"Miguel Ángel Royo-Bordonada, Carlos Fernández-Escobar, Carlos José Gil-Bellosta, Elena Ordaz","doi":"10.1186/s12966-022-01262-8","DOIUrl":null,"url":null,"abstract":"<p><strong>Background: </strong>The World Health Organisation urges countries to levy specific excise taxes on SSBs. Currently, more than 50 countries have introduced some type of tax on SSBs. In March 2017, the Autonomous Region of Catalonia approved the introduction of a tiered excise tax on SSBs for public health reasons. To evaluate the effect of the Catalonian excise tax on the price and purchase of sugar-sweetened beverages (SSBs) and their possible substitutes, i.e., non-sugar-sweetened beverages (NSSBs) and bottled water, three and half years after its introduction, and 1 year after the outbreak of the COVID-19 pandemic.</p><p><strong>Methods: </strong>We analysed purchase data on soft drinks, fruit drinks and water, sourced from the Ministry of Agriculture food-consumption panel, in a random sample of 12,500 households across Spain. We applied the synthetic control method to infer the causal impact of the intervention, based on a Bayesian structural time-series model which predicts the counterfactual response that would have occurred in Catalonia, had no intervention taken place.</p><p><strong>Results: </strong>As compared to the predicted (counterfactual) response, per capita purchases of SSBs fell by 0.17 l three and a half years after implementing the SSB tax in Catalonia, a 16.7% decline (95% CI: - 23.18, - 8.74). The mean SSB price rose by 0.11 €/L, an 11% increase (95% CI: 9.0, 14.1). Although there were no changes in mean NSSB prices, NSSB consumption rose by 0.19 l per capita, a 21.7% increase (95% CI: 18.25, 25.54). There were no variations in the price or consumption of bottled water. The effects were progressively greater over time, with SSB purchases decreasing by 10.4% at 1 year, 12.3% at 2 years, 15.3% at 3 years, and 16.7% at three and a half years of the tax's introduction.</p><p><strong>Conclusions: </strong>The Catalonian SSB excise tax had a sustained and progressive impact over time, with a fall in consumption of as much as 16.7% three and half years after its introduction. The observed NSSB substitution effect should be borne in mind when considering the application of this type of tax to the rest of Spain.</p>","PeriodicalId":49582,"journal":{"name":"Russian Mathematical Surveys","volume":"55 1","pages":"24"},"PeriodicalIF":2.1000,"publicationDate":"2022-03-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8917362/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Russian Mathematical Surveys","FirstCategoryId":"3","ListUrlMain":"https://doi.org/10.1186/s12966-022-01262-8","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"MATHEMATICS","Score":null,"Total":0}

引用次数: 0

Abstract

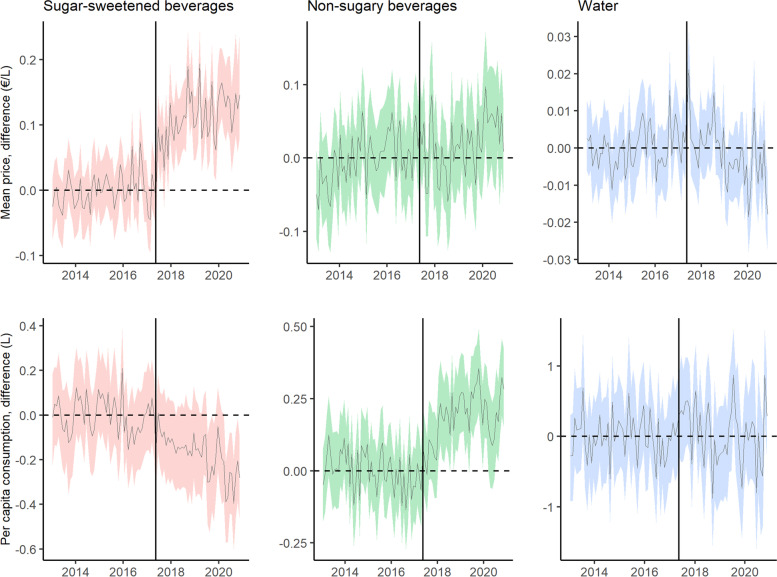

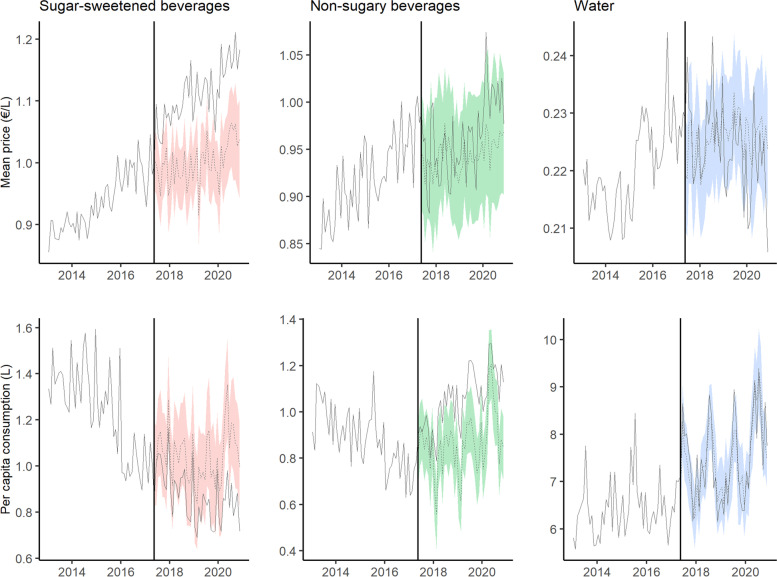

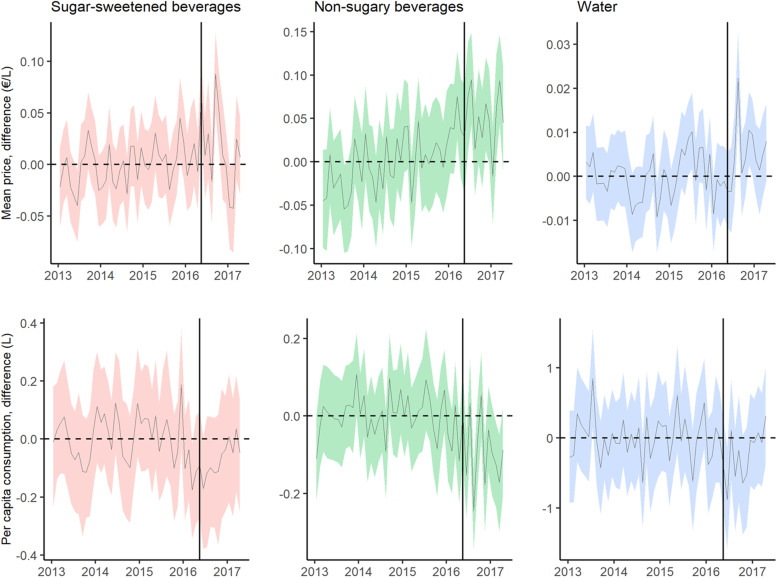

Background: The World Health Organisation urges countries to levy specific excise taxes on SSBs. Currently, more than 50 countries have introduced some type of tax on SSBs. In March 2017, the Autonomous Region of Catalonia approved the introduction of a tiered excise tax on SSBs for public health reasons. To evaluate the effect of the Catalonian excise tax on the price and purchase of sugar-sweetened beverages (SSBs) and their possible substitutes, i.e., non-sugar-sweetened beverages (NSSBs) and bottled water, three and half years after its introduction, and 1 year after the outbreak of the COVID-19 pandemic.

Methods: We analysed purchase data on soft drinks, fruit drinks and water, sourced from the Ministry of Agriculture food-consumption panel, in a random sample of 12,500 households across Spain. We applied the synthetic control method to infer the causal impact of the intervention, based on a Bayesian structural time-series model which predicts the counterfactual response that would have occurred in Catalonia, had no intervention taken place.

Results: As compared to the predicted (counterfactual) response, per capita purchases of SSBs fell by 0.17 l three and a half years after implementing the SSB tax in Catalonia, a 16.7% decline (95% CI: - 23.18, - 8.74). The mean SSB price rose by 0.11 €/L, an 11% increase (95% CI: 9.0, 14.1). Although there were no changes in mean NSSB prices, NSSB consumption rose by 0.19 l per capita, a 21.7% increase (95% CI: 18.25, 25.54). There were no variations in the price or consumption of bottled water. The effects were progressively greater over time, with SSB purchases decreasing by 10.4% at 1 year, 12.3% at 2 years, 15.3% at 3 years, and 16.7% at three and a half years of the tax's introduction.

Conclusions: The Catalonian SSB excise tax had a sustained and progressive impact over time, with a fall in consumption of as much as 16.7% three and half years after its introduction. The observed NSSB substitution effect should be borne in mind when considering the application of this type of tax to the rest of Spain.

期刊介绍:

Russian Mathematical Surveys is a high-prestige journal covering a wide area of mathematics. The Russian original is rigorously refereed in Russia and the translations are carefully scrutinised and edited by the London Mathematical Society. The survey articles on current trends in mathematics are generally written by leading experts in the field at the request of the Editorial Board.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们