{"title":"Synchronization in Cycles of China and India During Recent Crises: A Markov Switching Analysis.","authors":"Pami Dua, Divya Tuteja","doi":"10.1007/s40953-023-00343-0","DOIUrl":null,"url":null,"abstract":"<p><p>We study the impact of recent crisis episodes viz<i>.</i> the Great Recession of 2007-09, the Euro Area crisis of 2010-12 and the COVID-19 pandemic of 2020-21 on the Emerging Market Economies (EMEs) of China and India using data from January, 1986 till June, 2021. A Markov-switching (MS) analysis is applied to discern economy-specific cycles/regimes and common cycles/regimes in the growth rates of the economies. We apply the univariate MS Autoregressive (MS-AR) model to characterize country-specific negative growth, moderate growth and high growth regimes of China and India. We examine the extent of overlap of the identified regimes with the Great Recession, the Eurozone crisis, and the COVID-19 pandemic. Thereafter, we study the regimes depicting common phases in growth rates of China-India and China-India-US by using multivariate MS Vector Autoregressive (MS-VAR) models. The multivariate analysis shows the presence of common negative growth during the turbulent periods during the study period. These results can be explained by the existence of strong trade and financial linkages between the two EMEs and the Advanced economies. The pandemic triggered a recession in the Chinese, Indian and U.S. economies and its impact on growth is much worse than the Great Recession and the Eurozone crises.</p>","PeriodicalId":73920,"journal":{"name":"","volume":"21 2","pages":"317-337"},"PeriodicalIF":0.0,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10071472/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s40953-023-00343-0","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/4/4 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

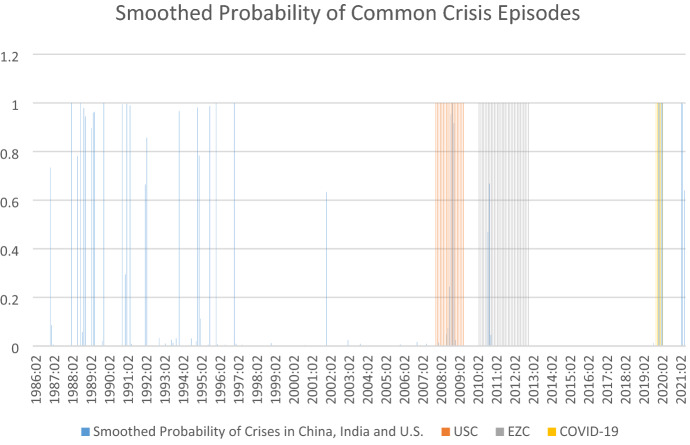

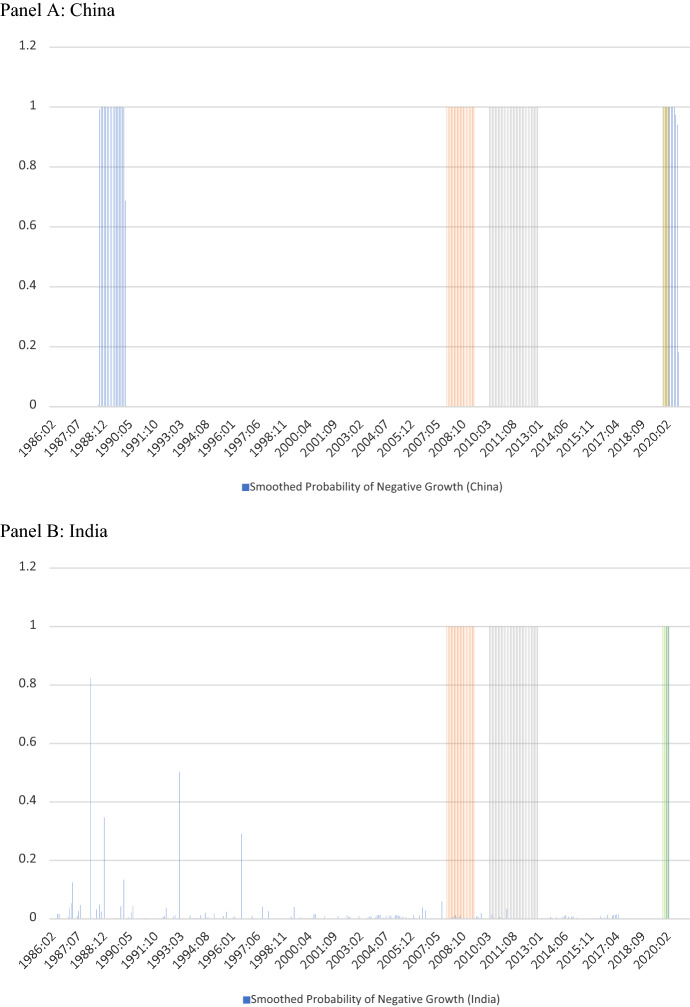

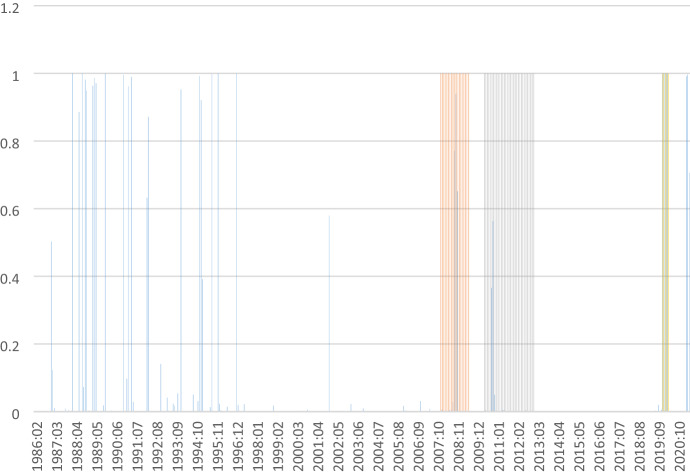

We study the impact of recent crisis episodes viz. the Great Recession of 2007-09, the Euro Area crisis of 2010-12 and the COVID-19 pandemic of 2020-21 on the Emerging Market Economies (EMEs) of China and India using data from January, 1986 till June, 2021. A Markov-switching (MS) analysis is applied to discern economy-specific cycles/regimes and common cycles/regimes in the growth rates of the economies. We apply the univariate MS Autoregressive (MS-AR) model to characterize country-specific negative growth, moderate growth and high growth regimes of China and India. We examine the extent of overlap of the identified regimes with the Great Recession, the Eurozone crisis, and the COVID-19 pandemic. Thereafter, we study the regimes depicting common phases in growth rates of China-India and China-India-US by using multivariate MS Vector Autoregressive (MS-VAR) models. The multivariate analysis shows the presence of common negative growth during the turbulent periods during the study period. These results can be explained by the existence of strong trade and financial linkages between the two EMEs and the Advanced economies. The pandemic triggered a recession in the Chinese, Indian and U.S. economies and its impact on growth is much worse than the Great Recession and the Eurozone crises.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们