Bluford Putnam, Graham McDannel, Mohandas Ayikara, Lakshmi Sameera Peyyalamitta

{"title":"描述政治事件风险事件中交易成本的动态性质","authors":"Bluford Putnam, Graham McDannel, Mohandas Ayikara, Lakshmi Sameera Peyyalamitta","doi":"10.1002/hf2.10018","DOIUrl":null,"url":null,"abstract":"<div>\n \n <p>Transactions costs as measured by how wide the bid-ask spread expands to execute fully large trades is a dynamically evolving process, especially during political risk event episodes. Our research looks at four case studies of political event risk: The UK “Brexit” referendum of June 2016, the US elections of November 2016, the first round of the French Presidential election in April 2017, and the UK “snap” Parliamentary election in June 2017. Each of these political events represented cases where the date of the event was known while the pre-event expectations were dealing with highly polar possible outcomes. This created the possibility of pre-event bi-modal return expectation probability distributions, which would resolve into single-mode distributions as the outcome become known. We examine second-by-second order book data for the relevant futures products and describe how transactions costs dynamically evolved during the “outcome discovery” period and then the “post-outcome re-balancing” period.</p>\n </div>","PeriodicalId":100604,"journal":{"name":"High Frequency","volume":"1 1","pages":"6-20"},"PeriodicalIF":0.0000,"publicationDate":"2018-04-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/hf2.10018","citationCount":"2","resultStr":"{\"title\":\"Describing the dynamic nature of transactions costs during political event risk episodes†\",\"authors\":\"Bluford Putnam, Graham McDannel, Mohandas Ayikara, Lakshmi Sameera Peyyalamitta\",\"doi\":\"10.1002/hf2.10018\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div>\\n \\n <p>Transactions costs as measured by how wide the bid-ask spread expands to execute fully large trades is a dynamically evolving process, especially during political risk event episodes. Our research looks at four case studies of political event risk: The UK “Brexit” referendum of June 2016, the US elections of November 2016, the first round of the French Presidential election in April 2017, and the UK “snap” Parliamentary election in June 2017. Each of these political events represented cases where the date of the event was known while the pre-event expectations were dealing with highly polar possible outcomes. This created the possibility of pre-event bi-modal return expectation probability distributions, which would resolve into single-mode distributions as the outcome become known. We examine second-by-second order book data for the relevant futures products and describe how transactions costs dynamically evolved during the “outcome discovery” period and then the “post-outcome re-balancing” period.</p>\\n </div>\",\"PeriodicalId\":100604,\"journal\":{\"name\":\"High Frequency\",\"volume\":\"1 1\",\"pages\":\"6-20\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2018-04-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1002/hf2.10018\",\"citationCount\":\"2\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"High Frequency\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10018\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"High Frequency","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10018","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Describing the dynamic nature of transactions costs during political event risk episodes†

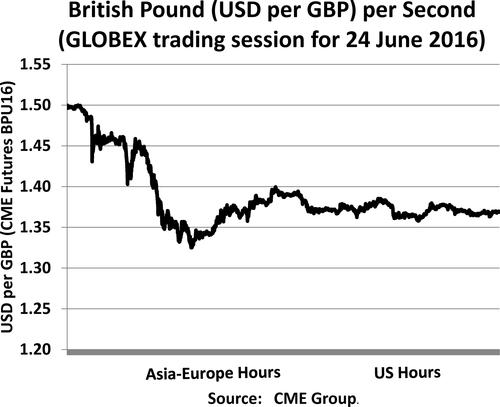

Transactions costs as measured by how wide the bid-ask spread expands to execute fully large trades is a dynamically evolving process, especially during political risk event episodes. Our research looks at four case studies of political event risk: The UK “Brexit” referendum of June 2016, the US elections of November 2016, the first round of the French Presidential election in April 2017, and the UK “snap” Parliamentary election in June 2017. Each of these political events represented cases where the date of the event was known while the pre-event expectations were dealing with highly polar possible outcomes. This created the possibility of pre-event bi-modal return expectation probability distributions, which would resolve into single-mode distributions as the outcome become known. We examine second-by-second order book data for the relevant futures products and describe how transactions costs dynamically evolved during the “outcome discovery” period and then the “post-outcome re-balancing” period.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们