{"title":"交易集群是否降低了交易成本?算法交易的周期性证据","authors":"Dmitriy Muravyev, Joerg Picard","doi":"10.1111/fima.12405","DOIUrl":null,"url":null,"abstract":"<p>We study how trading activity affects liquidity and volatility by introducing two periodicities in trading activity. First, trades and quote updates are much more frequent within the first 100 ms of a second than during its remainder. Second, trading activity often spikes at intervals of exactly one second. For these two periodicities, higher trade and quote intensities lead to higher volatility, but they do not significantly affect stock liquidity. These periodicities are likely caused by algorithms that trade predictably by repeating instructions in loops with round start times and time increments. Such predictable behavior may provide an example of behavioral biases in trading algorithms.</p>","PeriodicalId":48123,"journal":{"name":"Financial Management","volume":"51 4","pages":"1201-1229"},"PeriodicalIF":7.5000,"publicationDate":"2022-05-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fima.12405","citationCount":"0","resultStr":"{\"title\":\"Does trade clustering reduce trading costs? Evidence from periodicity in algorithmic trading\",\"authors\":\"Dmitriy Muravyev, Joerg Picard\",\"doi\":\"10.1111/fima.12405\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study how trading activity affects liquidity and volatility by introducing two periodicities in trading activity. First, trades and quote updates are much more frequent within the first 100 ms of a second than during its remainder. Second, trading activity often spikes at intervals of exactly one second. For these two periodicities, higher trade and quote intensities lead to higher volatility, but they do not significantly affect stock liquidity. These periodicities are likely caused by algorithms that trade predictably by repeating instructions in loops with round start times and time increments. Such predictable behavior may provide an example of behavioral biases in trading algorithms.</p>\",\"PeriodicalId\":48123,\"journal\":{\"name\":\"Financial Management\",\"volume\":\"51 4\",\"pages\":\"1201-1229\"},\"PeriodicalIF\":7.5000,\"publicationDate\":\"2022-05-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fima.12405\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Management\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/fima.12405\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Management","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/fima.12405","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Does trade clustering reduce trading costs? Evidence from periodicity in algorithmic trading

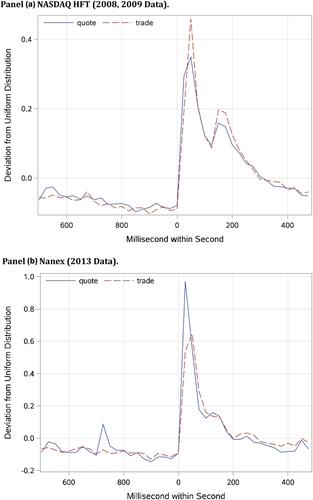

We study how trading activity affects liquidity and volatility by introducing two periodicities in trading activity. First, trades and quote updates are much more frequent within the first 100 ms of a second than during its remainder. Second, trading activity often spikes at intervals of exactly one second. For these two periodicities, higher trade and quote intensities lead to higher volatility, but they do not significantly affect stock liquidity. These periodicities are likely caused by algorithms that trade predictably by repeating instructions in loops with round start times and time increments. Such predictable behavior may provide an example of behavioral biases in trading algorithms.

期刊介绍:

Financial Management (FM) serves both academics and practitioners concerned with the financial management of nonfinancial businesses, financial institutions, and public or private not-for-profit organizations.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们