{"title":"利用递归神经网络探索基于区间的波动估计器的可预测性","authors":"Gábor Petneházi, József Gáll","doi":"10.1002/isaf.1455","DOIUrl":null,"url":null,"abstract":"<p>We investigate the predictability of several range-based stock volatility estimates and compare them with the standard close-to-close estimate, which is most commonly acknowledged as the volatility. The patterns of volatility changes are analysed using long short-term memory recurrent neural networks, which are a state-of-the-art method of sequence learning. We implement the analysis on all current constituents of the Dow Jones Industrial Average index and report averaged evaluation results. We find that the direction of changes in the values of range-based estimates are more predictable than that of the estimate from daily closing values only.</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"26 3","pages":"109-116"},"PeriodicalIF":2.0000,"publicationDate":"2019-08-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/isaf.1455","citationCount":"6","resultStr":"{\"title\":\"Exploring the predictability of range-based volatility estimators using recurrent neural networks\",\"authors\":\"Gábor Petneházi, József Gáll\",\"doi\":\"10.1002/isaf.1455\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We investigate the predictability of several range-based stock volatility estimates and compare them with the standard close-to-close estimate, which is most commonly acknowledged as the volatility. The patterns of volatility changes are analysed using long short-term memory recurrent neural networks, which are a state-of-the-art method of sequence learning. We implement the analysis on all current constituents of the Dow Jones Industrial Average index and report averaged evaluation results. We find that the direction of changes in the values of range-based estimates are more predictable than that of the estimate from daily closing values only.</p>\",\"PeriodicalId\":53473,\"journal\":{\"name\":\"Intelligent Systems in Accounting, Finance and Management\",\"volume\":\"26 3\",\"pages\":\"109-116\"},\"PeriodicalIF\":2.0000,\"publicationDate\":\"2019-08-09\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1002/isaf.1455\",\"citationCount\":\"6\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Intelligent Systems in Accounting, Finance and Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1455\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1455","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

Exploring the predictability of range-based volatility estimators using recurrent neural networks

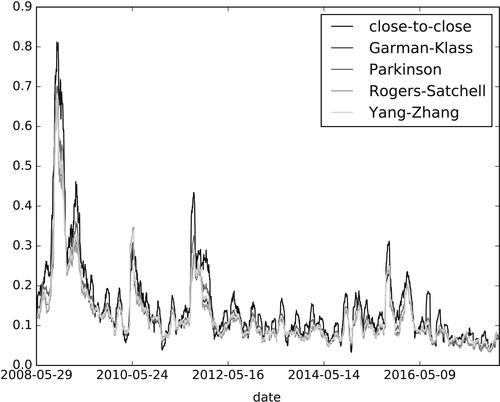

We investigate the predictability of several range-based stock volatility estimates and compare them with the standard close-to-close estimate, which is most commonly acknowledged as the volatility. The patterns of volatility changes are analysed using long short-term memory recurrent neural networks, which are a state-of-the-art method of sequence learning. We implement the analysis on all current constituents of the Dow Jones Industrial Average index and report averaged evaluation results. We find that the direction of changes in the values of range-based estimates are more predictable than that of the estimate from daily closing values only.

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们