{"title":"监管技术-现代信息技术在监管事务中的应用:研究和实践的兴趣领域","authors":"Michael Becker, Kevin Merz, Rüdiger Buchkremer","doi":"10.1002/isaf.1479","DOIUrl":null,"url":null,"abstract":"<p>We provide a high-level view on topics addressed in scientific articles about regulatory technology (RegTech), with a particular focus on technologies used. For this purpose, we first explore different denominations for RegTech and derive search queries to search relevant literature portals. From the hits of that information retrieval process, we select 55 articles outlining the application of information technology in regulatory affairs with an emphasis on the financial sector. In comparison, we examine the technological scope of 347 RegTech companies and compare our findings with the scientific literature. Our research reveals that ‘compliance management’ is the most relevant topic in practice, and ‘risk management’ is the primary subject in research. The most significant technologies as of today are ‘artificial intelligence’ and distributed ledger technologies such as ‘blockchain’.</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"27 4","pages":"161-167"},"PeriodicalIF":3.7000,"publicationDate":"2020-06-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/isaf.1479","citationCount":"13","resultStr":"{\"title\":\"RegTech—the application of modern information technology in regulatory affairs: areas of interest in research and practice\",\"authors\":\"Michael Becker, Kevin Merz, Rüdiger Buchkremer\",\"doi\":\"10.1002/isaf.1479\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We provide a high-level view on topics addressed in scientific articles about regulatory technology (RegTech), with a particular focus on technologies used. For this purpose, we first explore different denominations for RegTech and derive search queries to search relevant literature portals. From the hits of that information retrieval process, we select 55 articles outlining the application of information technology in regulatory affairs with an emphasis on the financial sector. In comparison, we examine the technological scope of 347 RegTech companies and compare our findings with the scientific literature. Our research reveals that ‘compliance management’ is the most relevant topic in practice, and ‘risk management’ is the primary subject in research. The most significant technologies as of today are ‘artificial intelligence’ and distributed ledger technologies such as ‘blockchain’.</p>\",\"PeriodicalId\":53473,\"journal\":{\"name\":\"Intelligent Systems in Accounting, Finance and Management\",\"volume\":\"27 4\",\"pages\":\"161-167\"},\"PeriodicalIF\":3.7000,\"publicationDate\":\"2020-06-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1002/isaf.1479\",\"citationCount\":\"13\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Intelligent Systems in Accounting, Finance and Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1479\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1479","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

RegTech—the application of modern information technology in regulatory affairs: areas of interest in research and practice

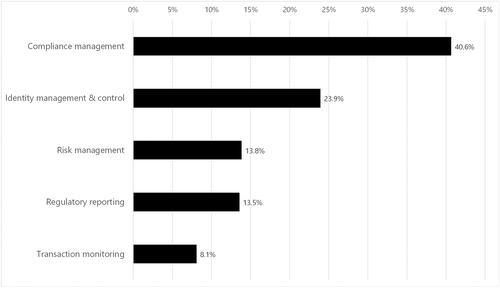

We provide a high-level view on topics addressed in scientific articles about regulatory technology (RegTech), with a particular focus on technologies used. For this purpose, we first explore different denominations for RegTech and derive search queries to search relevant literature portals. From the hits of that information retrieval process, we select 55 articles outlining the application of information technology in regulatory affairs with an emphasis on the financial sector. In comparison, we examine the technological scope of 347 RegTech companies and compare our findings with the scientific literature. Our research reveals that ‘compliance management’ is the most relevant topic in practice, and ‘risk management’ is the primary subject in research. The most significant technologies as of today are ‘artificial intelligence’ and distributed ledger technologies such as ‘blockchain’.

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们