{"title":"全球股市对俄乌战争的反应:经验证据","authors":"Emon Kalyan Chowdhury, Iffat Ishrat Khan","doi":"10.1007/s10690-023-09429-4","DOIUrl":null,"url":null,"abstract":"<div><p>This study measures the immediate impact of Russia–Ukraine war on the global stock markets for the first four months since Russia’s first invasion attempt on February 24, 2022. Daily closing stock indices have been used from selected stock markets of six different continents. By applying event study method, it observes mixed impact on different stock markets. Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH 1,1) indicates the presence of significant volatility and leverage effect in all the markets. Regression estimates show significantly positive impact of VIX and negative impact of oil on the abnormal returns of the global stock markets. Diversifying energy supply and source, accelerating deployment of renewables and promoting electronic vehicles and machines might bring positive result for the financial market. It is expected that this research will provide policymakers, regulatory authorities, investors and all concerned stakeholders a precise guideline to handle the immediate impact of war on the stock prices and to formulate appropriate strategies to keep investment free from risk and uncertainties.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"31 3","pages":"755 - 778"},"PeriodicalIF":2.6000,"publicationDate":"2023-10-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Reactions of Global Stock Markets to the Russia–Ukraine War: An Empirical Evidence\",\"authors\":\"Emon Kalyan Chowdhury, Iffat Ishrat Khan\",\"doi\":\"10.1007/s10690-023-09429-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study measures the immediate impact of Russia–Ukraine war on the global stock markets for the first four months since Russia’s first invasion attempt on February 24, 2022. Daily closing stock indices have been used from selected stock markets of six different continents. By applying event study method, it observes mixed impact on different stock markets. Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH 1,1) indicates the presence of significant volatility and leverage effect in all the markets. Regression estimates show significantly positive impact of VIX and negative impact of oil on the abnormal returns of the global stock markets. Diversifying energy supply and source, accelerating deployment of renewables and promoting electronic vehicles and machines might bring positive result for the financial market. It is expected that this research will provide policymakers, regulatory authorities, investors and all concerned stakeholders a precise guideline to handle the immediate impact of war on the stock prices and to formulate appropriate strategies to keep investment free from risk and uncertainties.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"31 3\",\"pages\":\"755 - 778\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-10-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-023-09429-4\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09429-4","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Reactions of Global Stock Markets to the Russia–Ukraine War: An Empirical Evidence

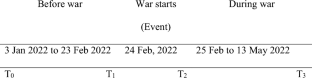

This study measures the immediate impact of Russia–Ukraine war on the global stock markets for the first four months since Russia’s first invasion attempt on February 24, 2022. Daily closing stock indices have been used from selected stock markets of six different continents. By applying event study method, it observes mixed impact on different stock markets. Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH 1,1) indicates the presence of significant volatility and leverage effect in all the markets. Regression estimates show significantly positive impact of VIX and negative impact of oil on the abnormal returns of the global stock markets. Diversifying energy supply and source, accelerating deployment of renewables and promoting electronic vehicles and machines might bring positive result for the financial market. It is expected that this research will provide policymakers, regulatory authorities, investors and all concerned stakeholders a precise guideline to handle the immediate impact of war on the stock prices and to formulate appropriate strategies to keep investment free from risk and uncertainties.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们