{"title":"拟合高维协整向量自回归模型的惩罚方法:综述","authors":"Marie Levakova, Susanne Ditlevsen","doi":"10.1111/insr.12553","DOIUrl":null,"url":null,"abstract":"<p>Cointegration has shown useful for modeling non-stationary data with long-run equilibrium relationships among variables, with applications in many fields such as econometrics, climate research and biology. However, the analyses of vector autoregressive models are becoming more difficult as data sets of higher dimensions are becoming available, in particular because the number of parameters is quadratic in the number of variables. This leads to lack of statistical robustness, and regularisation methods are paramount for obtaining valid estimates. In the last decade, many papers have appeared suggesting different penalisation approaches to the inference problem. Here, we make a comprehensive review of different penalisation methods adapted to the specific structure of vector cointegrated models suggested in the literature, with relevant references to software packages. The methods are evaluated and compared according to a range of error measures in a simulation study, considering combinations of low and high dimension of the system and small and large sample sizes.</p>","PeriodicalId":14479,"journal":{"name":"International Statistical Review","volume":"92 2","pages":"160-193"},"PeriodicalIF":1.8000,"publicationDate":"2023-09-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/insr.12553","citationCount":"0","resultStr":"{\"title\":\"Penalisation Methods in Fitting High-Dimensional Cointegrated Vector Autoregressive Models: A Review\",\"authors\":\"Marie Levakova, Susanne Ditlevsen\",\"doi\":\"10.1111/insr.12553\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Cointegration has shown useful for modeling non-stationary data with long-run equilibrium relationships among variables, with applications in many fields such as econometrics, climate research and biology. However, the analyses of vector autoregressive models are becoming more difficult as data sets of higher dimensions are becoming available, in particular because the number of parameters is quadratic in the number of variables. This leads to lack of statistical robustness, and regularisation methods are paramount for obtaining valid estimates. In the last decade, many papers have appeared suggesting different penalisation approaches to the inference problem. Here, we make a comprehensive review of different penalisation methods adapted to the specific structure of vector cointegrated models suggested in the literature, with relevant references to software packages. The methods are evaluated and compared according to a range of error measures in a simulation study, considering combinations of low and high dimension of the system and small and large sample sizes.</p>\",\"PeriodicalId\":14479,\"journal\":{\"name\":\"International Statistical Review\",\"volume\":\"92 2\",\"pages\":\"160-193\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-09-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/insr.12553\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Statistical Review\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/insr.12553\",\"RegionNum\":3,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Statistical Review","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/insr.12553","RegionNum":3,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

Penalisation Methods in Fitting High-Dimensional Cointegrated Vector Autoregressive Models: A Review

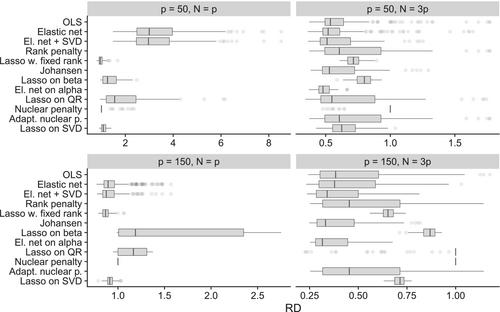

Cointegration has shown useful for modeling non-stationary data with long-run equilibrium relationships among variables, with applications in many fields such as econometrics, climate research and biology. However, the analyses of vector autoregressive models are becoming more difficult as data sets of higher dimensions are becoming available, in particular because the number of parameters is quadratic in the number of variables. This leads to lack of statistical robustness, and regularisation methods are paramount for obtaining valid estimates. In the last decade, many papers have appeared suggesting different penalisation approaches to the inference problem. Here, we make a comprehensive review of different penalisation methods adapted to the specific structure of vector cointegrated models suggested in the literature, with relevant references to software packages. The methods are evaluated and compared according to a range of error measures in a simulation study, considering combinations of low and high dimension of the system and small and large sample sizes.

期刊介绍:

International Statistical Review is the flagship journal of the International Statistical Institute (ISI) and of its family of Associations. It publishes papers of broad and general interest in statistics and probability. The term Review is to be interpreted broadly. The types of papers that are suitable for publication include (but are not limited to) the following: reviews/surveys of significant developments in theory, methodology, statistical computing and graphics, statistical education, and application areas; tutorials on important topics; expository papers on emerging areas of research or application; papers describing new developments and/or challenges in relevant areas; papers addressing foundational issues; papers on the history of statistics and probability; white papers on topics of importance to the profession or society; and historical assessment of seminal papers in the field and their impact.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们