Agata Kliber, Magdalena Szyszko, Mariusz Próchniak, Aleksandra Rutkowska

{"title":"不确定性对中欧和东欧国家通胀预测误差的影响","authors":"Agata Kliber, Magdalena Szyszko, Mariusz Próchniak, Aleksandra Rutkowska","doi":"10.1007/s40822-023-00237-9","DOIUrl":null,"url":null,"abstract":"Abstract The question underlying the research problem addressed by this study concerns various factors, including uncertainty, that could affect forecast errors. Previous works, focusing mainly on world-leading economies, are inconclusive on how economic agents form inflation forecasts or why forecast errors occur. There is a gap in the empirical literature that needs to be filled. The analysis covers the 2016–2020 period and seven economies: Albania, Czechia, Hungary, Poland, Romania, Serbia, and Turkey. We verify whether forecast errors are driven by production, inflation, exchange rates, interest rates, oil prices, changes in the tone of the central bank’s releases and their uncertainty. We assess whether economic agents can process available information to present accurate inflation forecasts. The results suggest that neither consumers nor professionals do—they present inaccurate forecasts regularly. The results suggest that exchange rate volatility is the most important variable that positively affects forecast errors, followed by inflation and its volatility. This confirms (in most cases) a theoretical assumption that a stable environment is better for long-term development as lower inflation forecast errors allow for the optimization of economic decisions. The study implies that mechanisms supporting forecasting during turbulent times must be strengthened. It presents the set of variables that should be analyzed more carefully by consumers and professionals. In addition, central banks could provide more precise communication regarding the evolution of error drivers. Our results build on existing literature by explicitly linking macroeconomic uncertainty with forecast errors including for small open economies from Eurasia.","PeriodicalId":45064,"journal":{"name":"Eurasian Economic Review","volume":"20 3","pages":"0"},"PeriodicalIF":2.5000,"publicationDate":"2023-11-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Impact of uncertainty on inflation forecast errors in Central and Eastern European countries\",\"authors\":\"Agata Kliber, Magdalena Szyszko, Mariusz Próchniak, Aleksandra Rutkowska\",\"doi\":\"10.1007/s40822-023-00237-9\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract The question underlying the research problem addressed by this study concerns various factors, including uncertainty, that could affect forecast errors. Previous works, focusing mainly on world-leading economies, are inconclusive on how economic agents form inflation forecasts or why forecast errors occur. There is a gap in the empirical literature that needs to be filled. The analysis covers the 2016–2020 period and seven economies: Albania, Czechia, Hungary, Poland, Romania, Serbia, and Turkey. We verify whether forecast errors are driven by production, inflation, exchange rates, interest rates, oil prices, changes in the tone of the central bank’s releases and their uncertainty. We assess whether economic agents can process available information to present accurate inflation forecasts. The results suggest that neither consumers nor professionals do—they present inaccurate forecasts regularly. The results suggest that exchange rate volatility is the most important variable that positively affects forecast errors, followed by inflation and its volatility. This confirms (in most cases) a theoretical assumption that a stable environment is better for long-term development as lower inflation forecast errors allow for the optimization of economic decisions. The study implies that mechanisms supporting forecasting during turbulent times must be strengthened. It presents the set of variables that should be analyzed more carefully by consumers and professionals. In addition, central banks could provide more precise communication regarding the evolution of error drivers. Our results build on existing literature by explicitly linking macroeconomic uncertainty with forecast errors including for small open economies from Eurasia.\",\"PeriodicalId\":45064,\"journal\":{\"name\":\"Eurasian Economic Review\",\"volume\":\"20 3\",\"pages\":\"0\"},\"PeriodicalIF\":2.5000,\"publicationDate\":\"2023-11-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Eurasian Economic Review\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s40822-023-00237-9\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Eurasian Economic Review","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s40822-023-00237-9","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Impact of uncertainty on inflation forecast errors in Central and Eastern European countries

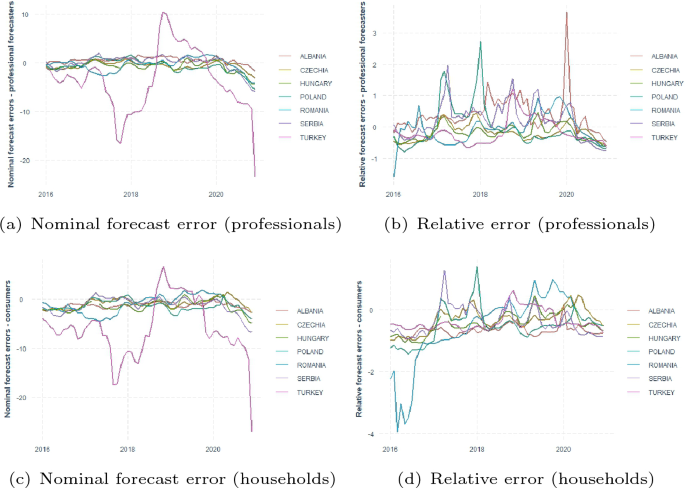

Abstract The question underlying the research problem addressed by this study concerns various factors, including uncertainty, that could affect forecast errors. Previous works, focusing mainly on world-leading economies, are inconclusive on how economic agents form inflation forecasts or why forecast errors occur. There is a gap in the empirical literature that needs to be filled. The analysis covers the 2016–2020 period and seven economies: Albania, Czechia, Hungary, Poland, Romania, Serbia, and Turkey. We verify whether forecast errors are driven by production, inflation, exchange rates, interest rates, oil prices, changes in the tone of the central bank’s releases and their uncertainty. We assess whether economic agents can process available information to present accurate inflation forecasts. The results suggest that neither consumers nor professionals do—they present inaccurate forecasts regularly. The results suggest that exchange rate volatility is the most important variable that positively affects forecast errors, followed by inflation and its volatility. This confirms (in most cases) a theoretical assumption that a stable environment is better for long-term development as lower inflation forecast errors allow for the optimization of economic decisions. The study implies that mechanisms supporting forecasting during turbulent times must be strengthened. It presents the set of variables that should be analyzed more carefully by consumers and professionals. In addition, central banks could provide more precise communication regarding the evolution of error drivers. Our results build on existing literature by explicitly linking macroeconomic uncertainty with forecast errors including for small open economies from Eurasia.

期刊介绍:

The mission of Eurasian Economic Review is to publish peer-reviewed empirical research papers that test, extend, or build theory and contribute to practice. All empirical methods - including, but not limited to, qualitative, quantitative, field, laboratory, and any combination of methods - are welcome. Empirical, theoretical and methodological articles from all fields of finance and applied macroeconomics are featured in the journal. Theoretical and/or review articles that integrate existing bodies of research and that provide new insights into the field are highly encouraged. The journal has a broad scope, addressing such issues as: financial systems and regulation, corporate and start-up finance, macro and sustainable finance, finance and innovation, consumer finance, public policies on financial markets within local, regional, national and international contexts, money and banking, and the interface of labor and financial economics. The macroeconomics coverage includes topics from monetary economics, labor economics, international economics and development economics.

Eurasian Economic Review is published quarterly. To be published in Eurasian Economic Review, a manuscript must make strong empirical and/or theoretical contributions and highlight the significance of those contributions to our field. Consequently, preference is given to submissions that test, extend, or build strong theoretical frameworks while empirically examining issues with high importance for theory and practice. Eurasian Economic Review is not tied to any national context. Although it focuses on Europe and Asia, all papers from related fields on any region or country are highly encouraged. Single country studies, cross-country or regional studies can be submitted.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们