Cheng Zhang, Nilam Nur Amir Sjarif, Roslina Ibrahim

{"title":"金融时间序列价格预测的深度学习模型:最新进展综述:2020-2022","authors":"Cheng Zhang, Nilam Nur Amir Sjarif, Roslina Ibrahim","doi":"10.1002/widm.1519","DOIUrl":null,"url":null,"abstract":"Abstract Accurately predicting the prices of financial time series is essential and challenging for the financial sector. Owing to recent advancements in deep learning techniques, deep learning models are gradually replacing traditional statistical and machine learning models as the first choice for price forecasting tasks. This shift in model selection has led to a notable rise in research related to applying deep learning models to price forecasting, resulting in a rapid accumulation of new knowledge. Therefore, we conducted a literature review of relevant studies over the past 3 years with a view to aiding researchers and practitioners in the field. This review delves deeply into deep learning‐based forecasting models, presenting information on model architectures, practical applications, and their respective advantages and disadvantages. In particular, detailed information is provided on advanced models for price forecasting, such as Transformers, generative adversarial networks (GANs), graph neural networks (GNNs), and deep quantum neural networks (DQNNs). The present contribution also includes potential directions for future research, such as examining the effectiveness of deep learning models with complex structures for price forecasting, extending from point prediction to interval prediction using deep learning models, scrutinizing the reliability and validity of decomposition ensembles, and exploring the influence of data volume on model performance. This article is categorized under: Technologies > Prediction Technologies > Artificial Intelligence","PeriodicalId":500599,"journal":{"name":"WIREs Data Mining and Knowledge Discovery","volume":"44 1","pages":"0"},"PeriodicalIF":0.0000,"publicationDate":"2023-09-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Deep learning models for price forecasting of financial time series: A review of recent advancements: 2020–2022\",\"authors\":\"Cheng Zhang, Nilam Nur Amir Sjarif, Roslina Ibrahim\",\"doi\":\"10.1002/widm.1519\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract Accurately predicting the prices of financial time series is essential and challenging for the financial sector. Owing to recent advancements in deep learning techniques, deep learning models are gradually replacing traditional statistical and machine learning models as the first choice for price forecasting tasks. This shift in model selection has led to a notable rise in research related to applying deep learning models to price forecasting, resulting in a rapid accumulation of new knowledge. Therefore, we conducted a literature review of relevant studies over the past 3 years with a view to aiding researchers and practitioners in the field. This review delves deeply into deep learning‐based forecasting models, presenting information on model architectures, practical applications, and their respective advantages and disadvantages. In particular, detailed information is provided on advanced models for price forecasting, such as Transformers, generative adversarial networks (GANs), graph neural networks (GNNs), and deep quantum neural networks (DQNNs). The present contribution also includes potential directions for future research, such as examining the effectiveness of deep learning models with complex structures for price forecasting, extending from point prediction to interval prediction using deep learning models, scrutinizing the reliability and validity of decomposition ensembles, and exploring the influence of data volume on model performance. This article is categorized under: Technologies > Prediction Technologies > Artificial Intelligence\",\"PeriodicalId\":500599,\"journal\":{\"name\":\"WIREs Data Mining and Knowledge Discovery\",\"volume\":\"44 1\",\"pages\":\"0\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-09-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"WIREs Data Mining and Knowledge Discovery\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1002/widm.1519\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"WIREs Data Mining and Knowledge Discovery","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1002/widm.1519","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

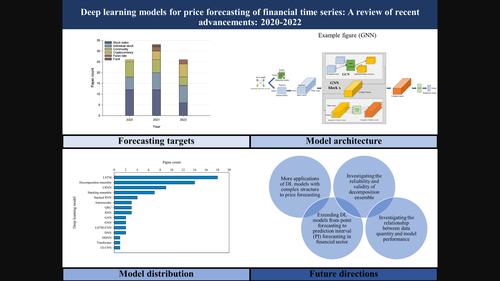

Deep learning models for price forecasting of financial time series: A review of recent advancements: 2020–2022

Abstract Accurately predicting the prices of financial time series is essential and challenging for the financial sector. Owing to recent advancements in deep learning techniques, deep learning models are gradually replacing traditional statistical and machine learning models as the first choice for price forecasting tasks. This shift in model selection has led to a notable rise in research related to applying deep learning models to price forecasting, resulting in a rapid accumulation of new knowledge. Therefore, we conducted a literature review of relevant studies over the past 3 years with a view to aiding researchers and practitioners in the field. This review delves deeply into deep learning‐based forecasting models, presenting information on model architectures, practical applications, and their respective advantages and disadvantages. In particular, detailed information is provided on advanced models for price forecasting, such as Transformers, generative adversarial networks (GANs), graph neural networks (GNNs), and deep quantum neural networks (DQNNs). The present contribution also includes potential directions for future research, such as examining the effectiveness of deep learning models with complex structures for price forecasting, extending from point prediction to interval prediction using deep learning models, scrutinizing the reliability and validity of decomposition ensembles, and exploring the influence of data volume on model performance. This article is categorized under: Technologies > Prediction Technologies > Artificial Intelligence

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们