Roy Cerqueti, Pierpaolo D’Urso, Livia De Giovanni, Raffaele Mattera, Vincenzina Vitale

{"title":"基于加权条件高矩的时间序列模糊聚类","authors":"Roy Cerqueti, Pierpaolo D’Urso, Livia De Giovanni, Raffaele Mattera, Vincenzina Vitale","doi":"10.1007/s00180-023-01425-6","DOIUrl":null,"url":null,"abstract":"Abstract This paper proposes a new approach to fuzzy clustering of time series based on the dissimilarity among conditional higher moments. A system of weights accounts for the relevance of each conditional moment in defining the clusters. Robustness against outliers is also considered by extending the above clustering method using a suitable exponential transformation of the distance measure defined on the conditional higher moments. To show the usefulness of the proposed approach, we provide a study with simulated data and an empirical application to the time series of stocks included in the FTSEMIB 30 Index.","PeriodicalId":55223,"journal":{"name":"Computational Statistics","volume":"77 6","pages":"0"},"PeriodicalIF":1.4000,"publicationDate":"2023-11-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Fuzzy clustering of time series based on weighted conditional higher moments\",\"authors\":\"Roy Cerqueti, Pierpaolo D’Urso, Livia De Giovanni, Raffaele Mattera, Vincenzina Vitale\",\"doi\":\"10.1007/s00180-023-01425-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract This paper proposes a new approach to fuzzy clustering of time series based on the dissimilarity among conditional higher moments. A system of weights accounts for the relevance of each conditional moment in defining the clusters. Robustness against outliers is also considered by extending the above clustering method using a suitable exponential transformation of the distance measure defined on the conditional higher moments. To show the usefulness of the proposed approach, we provide a study with simulated data and an empirical application to the time series of stocks included in the FTSEMIB 30 Index.\",\"PeriodicalId\":55223,\"journal\":{\"name\":\"Computational Statistics\",\"volume\":\"77 6\",\"pages\":\"0\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-11-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Computational Statistics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s00180-023-01425-6\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Statistics","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s00180-023-01425-6","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

Fuzzy clustering of time series based on weighted conditional higher moments

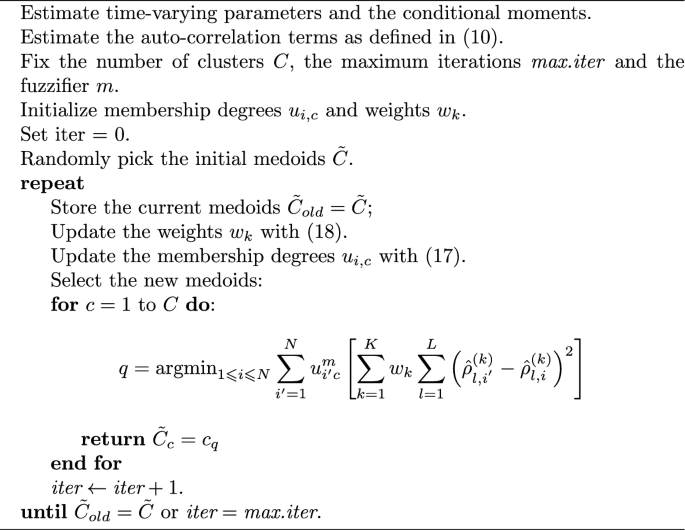

Abstract This paper proposes a new approach to fuzzy clustering of time series based on the dissimilarity among conditional higher moments. A system of weights accounts for the relevance of each conditional moment in defining the clusters. Robustness against outliers is also considered by extending the above clustering method using a suitable exponential transformation of the distance measure defined on the conditional higher moments. To show the usefulness of the proposed approach, we provide a study with simulated data and an empirical application to the time series of stocks included in the FTSEMIB 30 Index.

期刊介绍:

Computational Statistics (CompStat) is an international journal which promotes the publication of applications and methodological research in the field of Computational Statistics. The focus of papers in CompStat is on the contribution to and influence of computing on statistics and vice versa. The journal provides a forum for computer scientists, mathematicians, and statisticians in a variety of fields of statistics such as biometrics, econometrics, data analysis, graphics, simulation, algorithms, knowledge based systems, and Bayesian computing. CompStat publishes hardware, software plus package reports.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们