{"title":"一类具有方向切换代价的奇异随机控制问题","authors":"Łukasz Kruk","doi":"10.1007/s00186-023-00839-8","DOIUrl":null,"url":null,"abstract":"Abstract We introduce a new class of singular stochastic control problems in which the process controller not only chooses the push intensity, at a price proportional to the displacement caused by his action, but he can also change the allowable control direction, paying a fixed cost for each such switching. Singular control of the one-dimensional Brownian motion with quadratic instantaneous cost function and costly direction switching on the infinite time horizon is analyzed in detail, leading to a closed-form solution. This example is used as an illustration of qualitative differences between the class of problems considered here and classic singular stochastic control.","PeriodicalId":49862,"journal":{"name":"Mathematical Methods of Operations Research","volume":"11 1","pages":"0"},"PeriodicalIF":1.2000,"publicationDate":"2023-10-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A singular stochastic control problem with direction switching cost\",\"authors\":\"Łukasz Kruk\",\"doi\":\"10.1007/s00186-023-00839-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract We introduce a new class of singular stochastic control problems in which the process controller not only chooses the push intensity, at a price proportional to the displacement caused by his action, but he can also change the allowable control direction, paying a fixed cost for each such switching. Singular control of the one-dimensional Brownian motion with quadratic instantaneous cost function and costly direction switching on the infinite time horizon is analyzed in detail, leading to a closed-form solution. This example is used as an illustration of qualitative differences between the class of problems considered here and classic singular stochastic control.\",\"PeriodicalId\":49862,\"journal\":{\"name\":\"Mathematical Methods of Operations Research\",\"volume\":\"11 1\",\"pages\":\"0\"},\"PeriodicalIF\":1.2000,\"publicationDate\":\"2023-10-03\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Mathematical Methods of Operations Research\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s00186-023-00839-8\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, APPLIED\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematical Methods of Operations Research","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s00186-023-00839-8","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, APPLIED","Score":null,"Total":0}

A singular stochastic control problem with direction switching cost

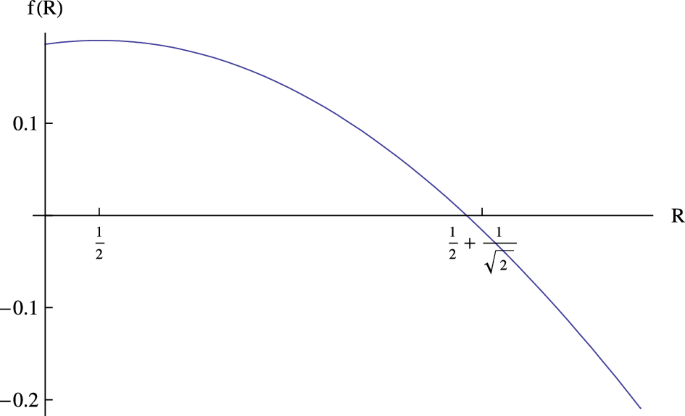

Abstract We introduce a new class of singular stochastic control problems in which the process controller not only chooses the push intensity, at a price proportional to the displacement caused by his action, but he can also change the allowable control direction, paying a fixed cost for each such switching. Singular control of the one-dimensional Brownian motion with quadratic instantaneous cost function and costly direction switching on the infinite time horizon is analyzed in detail, leading to a closed-form solution. This example is used as an illustration of qualitative differences between the class of problems considered here and classic singular stochastic control.

期刊介绍:

This peer reviewed journal publishes original and high-quality articles on important mathematical and computational aspects of operations research, in particular in the areas of continuous and discrete mathematical optimization, stochastics, and game theory. Theoretically oriented papers are supposed to include explicit motivations of assumptions and results, while application oriented papers need to contain substantial mathematical contributions. Suggestions for algorithms should be accompanied with numerical evidence for their superiority over state-of-the-art methods. Articles must be of interest for a large audience in operations research, written in clear and correct English, and typeset in LaTeX. A special section contains invited tutorial papers on advanced mathematical or computational aspects of operations research, aiming at making such methodologies accessible for a wider audience.

All papers are refereed. The emphasis is on originality, quality, and importance.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们