{"title":"经济政策不确定性、地缘政治风险、市场情绪和地区股票:欧盟行业的不对称分析","authors":"Ahmed Bossman, Mariya Gubareva, Tamara Teplova","doi":"10.1007/s40822-023-00234-y","DOIUrl":null,"url":null,"abstract":"Abstract The purpose of this study is to investigate the asymmetric effects of economic policy uncertainty (EPU), geopolitical risk (GPR), and market sentiment (VIX) on European Union (EU) stocks by sectors of economic activity. The design and methodological approach of our research are rooted in parametric and nonparametric quantile-based techniques. We employ monthly data covering eleven sectors of economic activity in addition to GPR, Global EPU, European Union EPU, United States EPU, and VIX. Our dataset covers the period between February 2013 and September 2022. Our findings show a generally low predictive power of the considered EPU measures on the stock returns of the EU sectors. Notwithstanding, the analysis reveals that EPU from the EU has the highest predictive ability on the EU sectoral stock returns while EPU from the US has no significant predictive ability on the stock returns from the EU. Our findings also highlight the asymmetric effects of various EPUs on EU stocks. Moreover, certain sectoral exposure to EU stocks, found to serve just as diversifiers in normal market conditions, could become a hedge and safe-haven against GPR in extreme economic conditions. Our findings also highlight the role of the VIX as a good gauge to hedge against the downside risks of the EU stocks. The originality of our work is two-fold. First, we extend the study of how global factors influence the EU stock market to the most recent period including the Russia–Ukraine conflict. Second, we perform this study on a sectoral basis. Therefore, the value of our findings is that they provide notable implications for market regulation and portfolio management.","PeriodicalId":45064,"journal":{"name":"Eurasian Economic Review","volume":"4 1","pages":"0"},"PeriodicalIF":2.5000,"publicationDate":"2023-09-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"3","resultStr":"{\"title\":\"Economic policy uncertainty, geopolitical risk, market sentiment, and regional stocks: asymmetric analyses of the EU sectors\",\"authors\":\"Ahmed Bossman, Mariya Gubareva, Tamara Teplova\",\"doi\":\"10.1007/s40822-023-00234-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract The purpose of this study is to investigate the asymmetric effects of economic policy uncertainty (EPU), geopolitical risk (GPR), and market sentiment (VIX) on European Union (EU) stocks by sectors of economic activity. The design and methodological approach of our research are rooted in parametric and nonparametric quantile-based techniques. We employ monthly data covering eleven sectors of economic activity in addition to GPR, Global EPU, European Union EPU, United States EPU, and VIX. Our dataset covers the period between February 2013 and September 2022. Our findings show a generally low predictive power of the considered EPU measures on the stock returns of the EU sectors. Notwithstanding, the analysis reveals that EPU from the EU has the highest predictive ability on the EU sectoral stock returns while EPU from the US has no significant predictive ability on the stock returns from the EU. Our findings also highlight the asymmetric effects of various EPUs on EU stocks. Moreover, certain sectoral exposure to EU stocks, found to serve just as diversifiers in normal market conditions, could become a hedge and safe-haven against GPR in extreme economic conditions. Our findings also highlight the role of the VIX as a good gauge to hedge against the downside risks of the EU stocks. The originality of our work is two-fold. First, we extend the study of how global factors influence the EU stock market to the most recent period including the Russia–Ukraine conflict. Second, we perform this study on a sectoral basis. Therefore, the value of our findings is that they provide notable implications for market regulation and portfolio management.\",\"PeriodicalId\":45064,\"journal\":{\"name\":\"Eurasian Economic Review\",\"volume\":\"4 1\",\"pages\":\"0\"},\"PeriodicalIF\":2.5000,\"publicationDate\":\"2023-09-25\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"3\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Eurasian Economic Review\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s40822-023-00234-y\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Eurasian Economic Review","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s40822-023-00234-y","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Economic policy uncertainty, geopolitical risk, market sentiment, and regional stocks: asymmetric analyses of the EU sectors

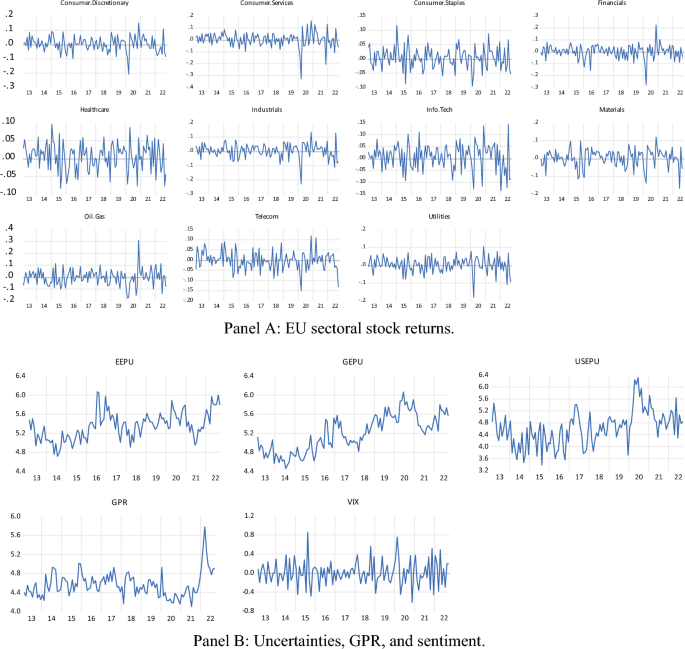

Abstract The purpose of this study is to investigate the asymmetric effects of economic policy uncertainty (EPU), geopolitical risk (GPR), and market sentiment (VIX) on European Union (EU) stocks by sectors of economic activity. The design and methodological approach of our research are rooted in parametric and nonparametric quantile-based techniques. We employ monthly data covering eleven sectors of economic activity in addition to GPR, Global EPU, European Union EPU, United States EPU, and VIX. Our dataset covers the period between February 2013 and September 2022. Our findings show a generally low predictive power of the considered EPU measures on the stock returns of the EU sectors. Notwithstanding, the analysis reveals that EPU from the EU has the highest predictive ability on the EU sectoral stock returns while EPU from the US has no significant predictive ability on the stock returns from the EU. Our findings also highlight the asymmetric effects of various EPUs on EU stocks. Moreover, certain sectoral exposure to EU stocks, found to serve just as diversifiers in normal market conditions, could become a hedge and safe-haven against GPR in extreme economic conditions. Our findings also highlight the role of the VIX as a good gauge to hedge against the downside risks of the EU stocks. The originality of our work is two-fold. First, we extend the study of how global factors influence the EU stock market to the most recent period including the Russia–Ukraine conflict. Second, we perform this study on a sectoral basis. Therefore, the value of our findings is that they provide notable implications for market regulation and portfolio management.

期刊介绍:

The mission of Eurasian Economic Review is to publish peer-reviewed empirical research papers that test, extend, or build theory and contribute to practice. All empirical methods - including, but not limited to, qualitative, quantitative, field, laboratory, and any combination of methods - are welcome. Empirical, theoretical and methodological articles from all fields of finance and applied macroeconomics are featured in the journal. Theoretical and/or review articles that integrate existing bodies of research and that provide new insights into the field are highly encouraged. The journal has a broad scope, addressing such issues as: financial systems and regulation, corporate and start-up finance, macro and sustainable finance, finance and innovation, consumer finance, public policies on financial markets within local, regional, national and international contexts, money and banking, and the interface of labor and financial economics. The macroeconomics coverage includes topics from monetary economics, labor economics, international economics and development economics.

Eurasian Economic Review is published quarterly. To be published in Eurasian Economic Review, a manuscript must make strong empirical and/or theoretical contributions and highlight the significance of those contributions to our field. Consequently, preference is given to submissions that test, extend, or build strong theoretical frameworks while empirically examining issues with high importance for theory and practice. Eurasian Economic Review is not tied to any national context. Although it focuses on Europe and Asia, all papers from related fields on any region or country are highly encouraged. Single country studies, cross-country or regional studies can be submitted.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们