Ugur Korkut Pata, Ojonugwa Usman, Godwin Olasehinde-Williams, Oktay Ozkan

{"title":"土耳其的股票回报率、原油和黄金价格:基于滚动窗口的非参数量子因果检验的证据","authors":"Ugur Korkut Pata, Ojonugwa Usman, Godwin Olasehinde-Williams, Oktay Ozkan","doi":"10.1007/s10690-023-09430-x","DOIUrl":null,"url":null,"abstract":"<div><p>This study explores the time-varying effects of crude oil prices (OP) and gold prices (GP) on the Turkish stock market using a weekly data series from November 26, 1989 to July 10, 2022. For this purpose, we develop a new hybrid technique, the rolling window-based nonparametric quantile causality test, which allows the investigation of time-varying causality at various quantiles. The results reveal that (i) under all market conditions, there is time-varying causality from crude OP and GP to Turkish stock market returns (SMR) and volatility. (ii) The causal effects of both crude OP and GP on stock market volatility are larger than their causal effects on SMR. (iii) The crude OP have a greater impact on SMR than the GP, while the GP has a greater impact on stock market volatility than the crude OP. (iv) Both crude OP and GP have the strongest (least) causal impact on SMR and volatility under normal (bullish) market conditions. (v) Crude OP and GP have a greater impact on stock market volatility than on stock returns under all market conditions. Overall, our results highlight that OP and GP have a strong impact on the Turkish stock market, and this impact varies by returns and volatility. Therefore, financial investors should consider the volatility of crude OP and GP in the Turkish stock market.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"31 3","pages":"779 - 797"},"PeriodicalIF":2.6000,"publicationDate":"2023-10-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Stock Returns, Crude Oil and Gold Prices in Turkey: Evidence from Rolling Window-Based Nonparametric Quantile Causality Test\",\"authors\":\"Ugur Korkut Pata, Ojonugwa Usman, Godwin Olasehinde-Williams, Oktay Ozkan\",\"doi\":\"10.1007/s10690-023-09430-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study explores the time-varying effects of crude oil prices (OP) and gold prices (GP) on the Turkish stock market using a weekly data series from November 26, 1989 to July 10, 2022. For this purpose, we develop a new hybrid technique, the rolling window-based nonparametric quantile causality test, which allows the investigation of time-varying causality at various quantiles. The results reveal that (i) under all market conditions, there is time-varying causality from crude OP and GP to Turkish stock market returns (SMR) and volatility. (ii) The causal effects of both crude OP and GP on stock market volatility are larger than their causal effects on SMR. (iii) The crude OP have a greater impact on SMR than the GP, while the GP has a greater impact on stock market volatility than the crude OP. (iv) Both crude OP and GP have the strongest (least) causal impact on SMR and volatility under normal (bullish) market conditions. (v) Crude OP and GP have a greater impact on stock market volatility than on stock returns under all market conditions. Overall, our results highlight that OP and GP have a strong impact on the Turkish stock market, and this impact varies by returns and volatility. Therefore, financial investors should consider the volatility of crude OP and GP in the Turkish stock market.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"31 3\",\"pages\":\"779 - 797\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-10-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-023-09430-x\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09430-x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

摘要

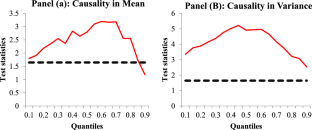

本研究利用 1989 年 11 月 26 日至 2022 年 7 月 10 日的每周数据序列,探讨了原油价格(OP)和黄金价格(GP)对土耳其股市的时变影响。为此,我们开发了一种新的混合技术,即基于滚动窗口的非参数量化因果检验,它允许在不同的量化水平上研究时变因果关系。结果显示:(i) 在所有市场条件下,原油 OP 和 GP 与土耳其股票市场收益率(SMR)和波动率之间存在时变因果关系。(ii) 原油 OP 和 GP 对股市波动性的因果效应大于其对 SMR 的因果效应。(iii) 原油 OP 对 SMR 的影响大于 GP,而 GP 对股市波动的影响大于原油 OP。(iv) 在正常(看涨)市场条件下,原油 OP 和 GP 对 SMR 和波动率的因果影响最大(最小)。(v) 在所有市场条件下,原油 OP 和 GP 对股市波动性的影响大于对股票收益率的影响。总之,我们的研究结果突出表明,OP 和 GP 对土耳其股市有很大的影响,而且这种影响因收益率和波动率的不同而不同。因此,金融投资者应考虑土耳其股市中原油 OP 和 GP 的波动性。

Stock Returns, Crude Oil and Gold Prices in Turkey: Evidence from Rolling Window-Based Nonparametric Quantile Causality Test

This study explores the time-varying effects of crude oil prices (OP) and gold prices (GP) on the Turkish stock market using a weekly data series from November 26, 1989 to July 10, 2022. For this purpose, we develop a new hybrid technique, the rolling window-based nonparametric quantile causality test, which allows the investigation of time-varying causality at various quantiles. The results reveal that (i) under all market conditions, there is time-varying causality from crude OP and GP to Turkish stock market returns (SMR) and volatility. (ii) The causal effects of both crude OP and GP on stock market volatility are larger than their causal effects on SMR. (iii) The crude OP have a greater impact on SMR than the GP, while the GP has a greater impact on stock market volatility than the crude OP. (iv) Both crude OP and GP have the strongest (least) causal impact on SMR and volatility under normal (bullish) market conditions. (v) Crude OP and GP have a greater impact on stock market volatility than on stock returns under all market conditions. Overall, our results highlight that OP and GP have a strong impact on the Turkish stock market, and this impact varies by returns and volatility. Therefore, financial investors should consider the volatility of crude OP and GP in the Turkish stock market.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们