{"title":"用于分析流式时间序列数据的非交叉量级双自回归","authors":"Rong Jiang, Siu Kai Choy, Keming Yu","doi":"10.1111/jtsa.12725","DOIUrl":null,"url":null,"abstract":"<p>Many financial time series not only have varying structures at different quantile levels and exhibit the phenomenon of conditional heteroscedasticity at the same time but also arrive in the stream. Quantile double-autoregression is very useful for time series analysis but faces challenges with model fitting of streaming data sets when estimating other quantiles in subsequent batches. This article proposes a renewable estimation method for quantile double-autoregression analysis of streaming time series data due to its ability to break with storage barrier and computational barrier. Moreover, the proposed flexible parametric structure of the quantile function enables us to predict any interested quantile value without quantile curve crossing problem or keeping the desirable monotone property of the conditional quantile function. The proposed methods are illustrated using current data and the summary statistics of historical data. Theoretically, the proposed statistic is shown to have the same asymptotic distribution as the standard version computed on an entire data stream with the data batches pooled into one data set, without additional condition. Simulation studies and an empirical example are presented to illustrate the finite sample performance of the proposed methods.</p>","PeriodicalId":49973,"journal":{"name":"Journal of Time Series Analysis","volume":"45 4","pages":"513-532"},"PeriodicalIF":1.0000,"publicationDate":"2023-10-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12725","citationCount":"0","resultStr":"{\"title\":\"Non-crossing quantile double-autoregression for the analysis of streaming time series data\",\"authors\":\"Rong Jiang, Siu Kai Choy, Keming Yu\",\"doi\":\"10.1111/jtsa.12725\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Many financial time series not only have varying structures at different quantile levels and exhibit the phenomenon of conditional heteroscedasticity at the same time but also arrive in the stream. Quantile double-autoregression is very useful for time series analysis but faces challenges with model fitting of streaming data sets when estimating other quantiles in subsequent batches. This article proposes a renewable estimation method for quantile double-autoregression analysis of streaming time series data due to its ability to break with storage barrier and computational barrier. Moreover, the proposed flexible parametric structure of the quantile function enables us to predict any interested quantile value without quantile curve crossing problem or keeping the desirable monotone property of the conditional quantile function. The proposed methods are illustrated using current data and the summary statistics of historical data. Theoretically, the proposed statistic is shown to have the same asymptotic distribution as the standard version computed on an entire data stream with the data batches pooled into one data set, without additional condition. Simulation studies and an empirical example are presented to illustrate the finite sample performance of the proposed methods.</p>\",\"PeriodicalId\":49973,\"journal\":{\"name\":\"Journal of Time Series Analysis\",\"volume\":\"45 4\",\"pages\":\"513-532\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-10-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12725\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Time Series Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12725\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Time Series Analysis","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12725","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Non-crossing quantile double-autoregression for the analysis of streaming time series data

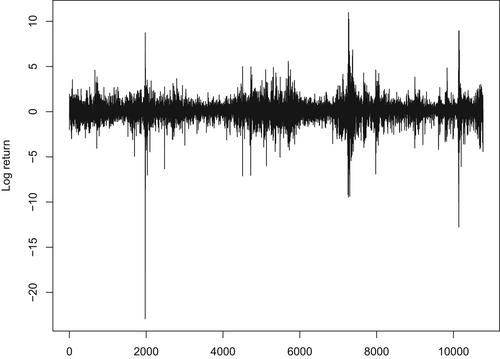

Many financial time series not only have varying structures at different quantile levels and exhibit the phenomenon of conditional heteroscedasticity at the same time but also arrive in the stream. Quantile double-autoregression is very useful for time series analysis but faces challenges with model fitting of streaming data sets when estimating other quantiles in subsequent batches. This article proposes a renewable estimation method for quantile double-autoregression analysis of streaming time series data due to its ability to break with storage barrier and computational barrier. Moreover, the proposed flexible parametric structure of the quantile function enables us to predict any interested quantile value without quantile curve crossing problem or keeping the desirable monotone property of the conditional quantile function. The proposed methods are illustrated using current data and the summary statistics of historical data. Theoretically, the proposed statistic is shown to have the same asymptotic distribution as the standard version computed on an entire data stream with the data batches pooled into one data set, without additional condition. Simulation studies and an empirical example are presented to illustrate the finite sample performance of the proposed methods.

期刊介绍:

During the last 30 years Time Series Analysis has become one of the most important and widely used branches of Mathematical Statistics. Its fields of application range from neurophysiology to astrophysics and it covers such well-known areas as economic forecasting, study of biological data, control systems, signal processing and communications and vibrations engineering.

The Journal of Time Series Analysis started in 1980, has since become the leading journal in its field, publishing papers on both fundamental theory and applications, as well as review papers dealing with recent advances in major areas of the subject and short communications on theoretical developments. The editorial board consists of many of the world''s leading experts in Time Series Analysis.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们