{"title":"跨国公司和从避税天堂进口的服务:当政策阻碍税收筹划时","authors":"Joana Garcia","doi":"10.1057/s41308-023-00227-6","DOIUrl":null,"url":null,"abstract":"<p>We study services imports by multinational groups from tax havens and investigate to what extent those imports may have profit shifting motives. Drawing on rich data covering the universe of multinational groups with a presence in Portugal, we show that despite a high statutory rate of the corporate income tax, in the presence of strict anti-avoidance rules and a patent box regime, multinational groups do not have an excess propensity to import intra-group services from tax havens. For the havens directly targeted by anti-tax planning policies, there is even a negative excess propensity to do so. Moreover, the value of intra-group services imports from most tax havens is not found to be excessive.</p>","PeriodicalId":47177,"journal":{"name":"Imf Economic Review","volume":"91 ","pages":""},"PeriodicalIF":3.3000,"publicationDate":"2023-12-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Multinationals and Services Imports from Havens: When Policies Stand in the Way of Tax Planning\",\"authors\":\"Joana Garcia\",\"doi\":\"10.1057/s41308-023-00227-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study services imports by multinational groups from tax havens and investigate to what extent those imports may have profit shifting motives. Drawing on rich data covering the universe of multinational groups with a presence in Portugal, we show that despite a high statutory rate of the corporate income tax, in the presence of strict anti-avoidance rules and a patent box regime, multinational groups do not have an excess propensity to import intra-group services from tax havens. For the havens directly targeted by anti-tax planning policies, there is even a negative excess propensity to do so. Moreover, the value of intra-group services imports from most tax havens is not found to be excessive.</p>\",\"PeriodicalId\":47177,\"journal\":{\"name\":\"Imf Economic Review\",\"volume\":\"91 \",\"pages\":\"\"},\"PeriodicalIF\":3.3000,\"publicationDate\":\"2023-12-06\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Imf Economic Review\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1057/s41308-023-00227-6\",\"RegionNum\":2,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Imf Economic Review","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1057/s41308-023-00227-6","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Multinationals and Services Imports from Havens: When Policies Stand in the Way of Tax Planning

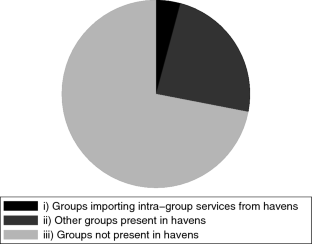

We study services imports by multinational groups from tax havens and investigate to what extent those imports may have profit shifting motives. Drawing on rich data covering the universe of multinational groups with a presence in Portugal, we show that despite a high statutory rate of the corporate income tax, in the presence of strict anti-avoidance rules and a patent box regime, multinational groups do not have an excess propensity to import intra-group services from tax havens. For the havens directly targeted by anti-tax planning policies, there is even a negative excess propensity to do so. Moreover, the value of intra-group services imports from most tax havens is not found to be excessive.

期刊介绍:

The IMF Economic Review is the official research journal of the International Monetary Fund (IMF). It is dedicated to publishing peer-reviewed, high-quality, context-related academic research on open-economy macroeconomics. It emphasizes rigorous analysis with an empirical orientation that is of interest to a broad audience, including academics and policymakers. Studies that borrow from, and interact with, other fields such as finance, international trade, political economy, labor, economic history or development are also welcome.

The views presented in published papers are those of the authors and should not be attributed to, or reported as, reflecting the position of the IMF, its Executive Board, or any other organization mentioned herein.

Comments

“The IMF Economic Review has been uniquely successful in publishing papers that rigorously analyze real international macroeconomic problems and in a manner that has immediate policy relevance. This success is owed to a great extent to the high quality of the editorial board, which is able to identify papers that are both relevant for policy and are executed using state-of-the-art tools so as to make the analysis compelling.” - Gita Gopinath, Economic Counsellor and Director of Research, IMF

“IMF Economic Review is devoted to state-of-the-art research on the global economy. Given the Fund''s unique position on the front lines of surveillance and crisis management, anyone interested in international economic policy or in macroeconomics more generally will find this journal to be essential reading.” - Maurice Obstfeld, Professor of Economics at University of California, Berkeley; and former Economic Counsellor and Director of Research, IMF

“There is great need for a rigorous academic publication that addresses the key global macro questions of our times. This is what the IMF Economic Review aims to be.” - Pierre-Olivier Gourinchas, Professor of Economics at University of California, Berkeley; and former Editor of the IMF Economic Review

“To navigate the global crisis, and to take the best policy decisions, will require mobilizing and extending the knowledge we have about open economy macro, from the implications of liquidity traps, to the dangers of large fiscal deficits, to macro-financial interactions, to the contours of a better international monetary and financial system. My hope and my expectation is that the IMF Economic Review will be central to the effort.” - Olivier J. Blanchard, Peterson Institute for International Economics; former Economic Counsellor and Director of Research Department, IMF

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们